Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The Two Most Important Questions Every Commodity Investor Must AskBy

Tuesday, September 4, 2012

What about China?

The answer is important because China affects so much of the world economy, especially as it relates to commodity prices – and your commodity stocks...

A friend of mine forwarded me a story where a certain strategist said it was time to "start adding Chinese exposure." He said, "Where else can you buy an economy with 7%-8% growth prospects at less than 10 times estimated earnings?"

To believe his statement, you have to take two things at face value:

I don't buy either statement.

The 7%-8% growth rate assumption comes from China's own GDP statistics. GDP, which stands for "gross domestic product," is a widely accepted rough guess of economic growth. For an investor, it is almost useless, and I usually ignore it.

That's because as an investor, you're not buying "the economy." You're buying individual securities. The characteristics of those securities should be your focus. Stick to the basics and what's in front of you. Don't get lost in abstractions like "GDP."

But let's play ball for a bit. If you want to rely on Chinese GDP figures to frame some kind of investment thesis, then you should know there is a lot of room to doubt their veracity.

So officially, China's government says its economy is growing 8%. Lots of people don't believe it. Charles Dumas, of Lombard Street Research, is one. He says: "We don't believe official data. We think GDP slowed to a 1% rate in the first quarter." I don't believe official data either, and I certainly don't make investment decisions based on it.

Two other quick points about relying on GDP:

Who knows at what rate China's economy is really growing? Frankly, I think it is an unknowable. China's economy is a huge, complex thing. It has many parts going in all kinds of directions. To boil all that down to a single number always strikes me as silly.

The second point up top is on China's corporate earnings. There is a good case that such earnings deserve heavy discounting. Maybe 10 times earnings is the right number in today's environment. As Ivy Pan, an analyst with ABN AMRO, said recently, "Forecasts of company earnings have been continuously revised downward since the beginning of the year." Besides, there is the issue of earnings quality and trustworthiness. This is a matter of debate, too.

So there is a lot of guesswork. There are also things we do know.

The strategist up top cites healthy increases in imports of coal, iron ore, and copper as a plank to his bullish thesis on China. He says the increase is consistent with an economy growing 7%-8%.

Again, we have to question how the figures come about. I think it is safe to say that Chinese government-mandated investment drives these figures. And I tend to think of that as more of a bad thing, not a good thing. Will it prop up commodity markets to some extent? Of course. It's not a game I care to play, though.

Anyway, it seems an odd thing to cite these commodities. Despite decent Chinese import figures, iron ore prices recently hit 2.5-year lows. Iron ore prices are down 17% since mid-June. Coking coal is down 23% since the start of July. Copper prices are down more than 20% from a year ago.

Chinese steel mills are hurting. The China Iron and Steel Association said recently that the Chinese steel industry's profits fell 96% in the first half of the year compared with last year. That's not a typo: down 96%.

These anecdotes don't square with the image of a booming economy.

I don't know what will happen, but I find the whole thing fascinating. I've been bearish on China in the last year, but I think some of the air has already come out of China's boom. (Take a look at housing prices, for instance. Chinese housing prices registered nine months of decline, and they just had an uptick.)

And there are definitely China themes I'd own and/or will continue to own – those that play on China's need for water and food, for instance. These are very good long-term investment themes, regardless of what happens in China in the near term.

But what about commodities?

Now we turn to the other piece of the puzzle. Most people wouldn't care a whit about China's economy. They care because China is such a big user of commodities and has such an impact on world prices.

A growing China is a key to the commodity bull market. But the commodity bull market is long in the tooth. It started in roughly 2000. (Jim Rogers and others date it from 1998.) So the bull market is at least 12 years old. The average lasts about 17 years, according to Jim Rogers' book Hot Commodities. However, this one may already be beyond what's normal.

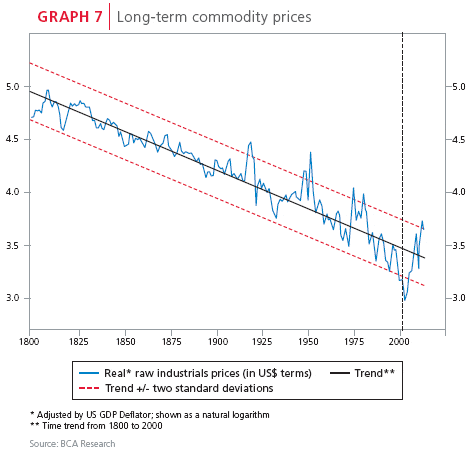

A reader sent me this chart on commodity prices from BCA Research and Allan Gray, which is the largest privately owned investment management firm in South Africa:

What this chart shows is that the long boom in commodity prices over the last dozen years has pushed commodity prices more than two standard deviations above their long-term trend line. In other words, we're in outlier territory. As you can see, not too many past bull markets have pushed much beyond where we are now.

There is another important point about that chart. Commodities, despite what you hear, are a poor way to preserve wealth over a long period of time. As Ian Liddle of Allan Gray notes:

I don't think this dynamic is somehow suspended in our own times. Commodities will continue to fall in real terms – that is, adjusted for inflation – over a long period of time. I think we've turned, or are turning, another corner. We should expect lower highs and lower lows on most commodities (in real terms) as the commodity bull market unwinds.

It will affect everything from iron ore to oil. (I exclude the precious metals, on which I remain bullish.)

If the bull market is, indeed, over, we have to change the way we look at investing in commodities. Commodity stocks have to clear different hurdles than in the last dozen years. We should not count on increases in commodity prices. Stocks should work at existing prices... and lower. I would favor picks-and-shovels plays over producers.

This is the way I plan to play it. It's the safe way to go. If I'm wrong, I'll be wrong for a year or two as the commodity bull takes its last breaths. But then, so what? There are plenty of other ideas to invest in.

The truth is that the end of the commodity bull market is coming. It seems too risky to try to and call the exact top. Start playing it safe now. Start preparing today.

Good investing,

Chris Mayer

Further Reading:

In February, Porter introduced readers to China's ongoing and enormous accumulation of gold... a plan that could allow it to replace the U.S. as the owner of the world's reserve currency...

"I know this will all sound crazy to most folks," he wrote. "But most folks don't understand gold... or why it represents real, timeless wealth. The Chinese do." Read his four-part series here...

Market NotesHOMEOWNERS: KEEP AN EYE ON THE 10-YEAR TREASURY YIELD It's decision time for interest rates.

One month ago, the yield on the 10-year Treasury note popped above resistance at 1.58%, signaling a possible trend change. It spiked sharply higher on the breakout. But over the past couple weeks, interest rates have come back down to retest the breakout level – which is now support.

The next move from here will tell us all we need to know about where rates are headed over the next few months. If support holds and interest rates bounce, look for higher rates by the end of the year.

On the other hand, if the 10-year yield drops through support at 1.58%, homeowners may get another chance to refinance their mortgages by Christmas.

– Jeff Clark  |

In The Daily Crux

Recent Articles

|