Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

A Three-Step Solution to the Hardest Problem Investors FaceBy

Wednesday, October 17, 2012

Without a plan... you're simply gambling...

To keep your investment returns high, you need to go into any investment knowing when to sell. Without a plan and strategy for selling, it's easy to get into trouble.

And knowing when to sell is only half the battle... you must also have the discipline to follow through with your plan. Sometimes, greed can slip in at the last minute. Sticking with a plan to sell is critical to protecting your profits.

Listening to my readers, I know this is one of the most difficult problems many individual investors face.

That's why, today, I want to share a few secrets to selling...

There are three keys to selling investments...

First, whenever you invest in something, it's important to write down why you bought it.

This means literally getting out paper or an index card (or opening a spreadsheet) and writing down your reasons for owning it – for dividend or interest income or potential growth-driven capital gains. You should note any data or metrics that support your investment decision. (For example, a low price relative to its earnings or cash flow.)

The second thing you need to do is write out when you'll sell the investment.

Do it on the same piece of paper and at the same time you're buying the investment. This includes writing out your expected percent return and over what time frame.

This is important as it expresses your plans before you become emotionally attached to the act of purchasing it. Once you own something, "confirmation bias" – the tendency to favor information that confirms your beliefs – tends to cloud your judgment. So it's better to outline your goals ahead of time.

The simplest way to know when to sell an investment is to set a simple stop loss or trailing stop loss. Both kinds of stop losses take the emotion out of the decision when an investment works against you.

With a simple stop loss, you set a fixed point at which you'd sell... essentially setting the maximum amount you're willing to lose if you're wrong on an investment.

With a trailing stop loss, you raise your selling price every time the stock hits a new high... Say you buy a stock at $50 a share and set the trailing stop at 20%. If the stock price falls straight down, you'd sell at $40 a share. But if it rises to $80 a share, you would sell on a decline back to $64. ($80 x 20% = $16. You subtract that $16 from the $80 high to determine the $64 stop price.) That way, you've protected yourself and pocketed a 28% gain.

You can also use fundamental analysis to determine when you might sell a stock – selling when the shares become overvalued relative to the company's earnings or cash flow and compared with other potential investments.

Or you can do what I like to do... and create a sell level on a chart by marking an expected return one-year out and then using that as the technical trigger. For example, I'll take a stock bought at $100. If my plan is to make 12% a year, I'll mark $112 and $124 on the chart. If in one or two years the stock hasn't traded above those levels, I'll sell. This sort of technical analysis can also incorporate moving averages or price support and resistance levels to guide you. (I don't use this much for selling, but I do when buying.)

However you determine your selling prices, it's important to write things down. This teaches you discipline. And it helps illustrate when investments are working out, and when they aren't. That way when it's clear they aren't working the way you envisioned... you can change things.

Finally, you must review your investments. You should do this at least once a year – preferably every six months. Make sure the reasons you bought remain valid.

One trick I use to make sure I stay disciplined is to ask myself whether I'd buy more right now or recommend it to friends or family members. If the answer is no, it's probably time to sell.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Get more priceless investing tips from Doc here...

"I've seen ignorance of this topic ruin more retirements than any other financial factor."

"It is the greatest trap there is in investing..."

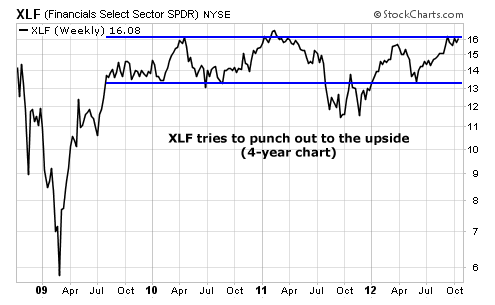

Market NotesA "MUST WATCH" LEVEL FOR AMERICA'S BANKS Regular DailyWealth readers know we monitor XLF, the big U.S. financial stock fund, to gauge the action in the banking sector. With large weightings in JPMorgan, Bank of America, Goldman Sachs, and Citigroup, XLF rises and falls according to America's ability to earn money, save money, service debts, start businesses, and generally just "get along."

In 2009, XLF enjoyed a big rebound off its credit-panic lows. But in August that year, the uptrend stalled out and turned into a long period of sideways trading action. Three years later, XLF is still drifting sideways...

In the past two months, though, the bulls have managed to push XLF past $16 per share. It's now in the upper reaches of this big sideways pattern. XLF's holdings are the backbone of our banking and credit system... If the fund can finally blast out of its trading range, we'll know America's financial backbone is strong.

|

In The Daily Crux

Recent Articles

|