Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today, we bring you the next installment of our week-long series on how to safeguard your wealth from inflation. So far, we've shown you ways to get out of paper dollars and into "real" assets like timber and precious metals. It's also worth considering Porter's take on... The World's Greatest Business in Inflationary TimesBy

Wednesday, October 24, 2012

There's one asset class that appears tailor-made to thrive in inflationary times...

Make no mistake. I know how horrible the inflation I expect will be for most Americans. But all I can do about it is try to position my readers to keep pace with the inflation that's coming.

And these stocks are one of the best ways I know to do that...

There's a reason many professional investors, including myself, believe insurance is the best business in the world.

Few individual investors understand why this is so...

One of my overriding goals is to give you the knowledge I'd want to have if our roles were reversed. When it comes to insurance and insurance stocks, I can only beg you to pay close attention. I believe if individuals would limit themselves to only investing in insurance companies – and no other sector – they would greatly increase their average annual returns. There's no other sector of the market where I believe that's true.

There's a simple reason for this, which everyone can understand, immediately. It's completely intuitive. But I'm pretty sure your broker has never explained it to you...

Insurance is the only business in the world that routinely enjoys a positive cost of capital. In every other business, companies must pay for capital. They borrow through loans. They raise equity (and most pay dividends). They pay depositors. Everywhere else you look, in every other sector, in every other type of business, the cost of capital is one of the primary business considerations.

But a well-run insurance company will routinely not only get all the capital it needs for free, it will actually be paid to accept it.

The best insurance companies make sure the fees they charge for capital are in excess of the risks they accept by extending insurance. These companies actually make a profit on their underwriting. They earn money by taking the capital of their customers. It's incredible. These firms compound their equity by simply opening their doors every morning. They don't have to do anything else. Nothing else in business is like it.

As legendary investor Warren Buffett explained in his 2011 letter to Berkshire Hathaway shareholders...

The beauty of insurance is that you can get paid to use capital. That's a fantastic way to become very wealthy. And it's precisely how (along with several great stock picks) Buffett became the world's most successful investor.

The nature of this business gives Berkshire – and other insurance firms who can earn a profit with their underwriting and their investments – a truly mind-boggling advantage. And that's not the only one.

Their other huge advantage – and it's a doozy – is that they don't have to pay taxes on those underwriting gains for many, many years because on paper, they haven't technically earned any of the float until all of the possible claims on the capital have expired. So unlike most companies that have to pay taxes on revenue and profits before investing capital, Berkshire and other insurance companies get to invest all the float, without paying any taxes for years and years and years.

These companies, then, are sensitive to increased economic activity (which leads to more insurance being sold), interest rates (thanks to their float, they are extremely leveraged to the capital markets), and inflation.

Let's assume I'm right, and the value of the U.S. dollar is going to collapse. If that happens, the dollars these insurance companies are collecting in premiums today will be invested with the full purchasing power the dollar has now. But they will only pay out claims over the next 10 or 20 years... when the value of that dollar will have fallen by 50% or more.

This inflation/time arbitrage almost guarantees big profits for the entire industry.

The biggest gains will go to the companies that earn a profit on their underwriting – that is, they collect more in premiums than they pay out in claims. Inflation will make future claims more expensive. (Prices will rise and damages will rise with them.) But inflation will also push up the value of the investments the insurance companies make – especially those firms that make equity investments.

I'm telling my readers to buy insurance stocks because I believe inflation will increase the size of policies sold... increase the return on float... and enable these companies to profit from the time arbitrage of inflation. (The dollars paid today in premiums will be worth substantially more than those same dollars paid back later.)

I also believe we have an investment opportunity in the insurance sector that only comes up every 20 years or so.

Financial stocks of all stripes have taken a beating since the financial crisis of 2008/2009. That will discourage many readers from buying these stocks, as lots of my more inexperienced readers still prefer to chase this year's hot stock or trendy sector. I can only shake my head.

As the financial stocks and the insurance sector recover, I expect top-shelf insurance firms to perform well. That means... you might not have an opportunity this good in insurance stocks again for another 20 years... maybe ever.

Good investing,

Porter

Further Reading:

"There's nothing sexy about insurance," Steve Sjuggerud says. "There's nothing to get investors excited... But that's a mistake." To see why Steve agrees insurance is a great investment... take a look at his must-see price-to-book chart – and a table that shows you recent valuations for some of the top names in the sector – here: A Triple-Digit Opportunity Exists in This Hated Sector.

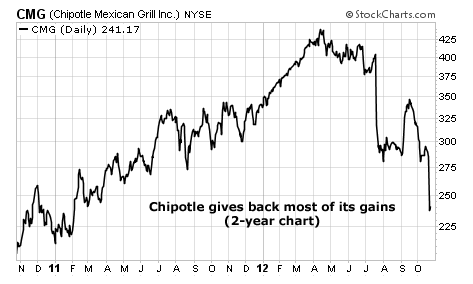

Market NotesTHIS WALL STREET DARLING HAS LOST ITS EDGE Trading stocks on momentum cuts both ways…

On the basis of "strong momentum," stocks can rally to dizzying heights. The problem is, these stocks tend to fall even quicker.

Today's chart of Chipotle Mexican Grill (NYSE: CMG) is an excellent example of this. As longtime readers know, the popular food chain has been the darling of Wall Street for most of the past two years. It only took 13 months for CMG to double in value… from $220 per share in February 2011 to its peak of $440 per share this past April.

It only took half as long for CMG to give up nearly all those gains. Today, the stock has completed the round trip. Shares are sitting back at $240 per share… proving the old axiom, what goes up must come down.

– Jeff Clark

|

In The Daily Crux

Recent Articles

|