Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The Next Stage of America's Rise to Energy DominanceBy

Wednesday, November 28, 2012

An incredible shift in the global energy markets is going on right now... and it's about to make the United States the world's most important producer of oil and natural gas.

Most people don't realize it, of course. Americans are used to thinking of our country as dependent on shaky, hostile nations for our energy needs.

That's changing... fast.

Advanced technologies, notably hydraulic fracturing and horizontal drilling, have opened vast domestic resources. Longtime DailyWealth readers should be familiar with this trend... we've been covering it for years. (You can read more here and here.)

But it's safe to say that despite the huge new supplies... I'm bullish on natural gas.

In April, just as natural gas was hitting its most recent lows, I told my Investment Advisory readers ...

To understand my argument, you need to understand why and how natural gas will become a global fuel, with a consistent global price – just like oil.

The prices for liquefied natural gas (LNG) are determined by long-term supply contracts. Little gas is available on the spot market (the market for immediately available gas). And currently, the prices on these long-term contracts are highly variable. In the U.S., natural gas sells for around $3 per thousand cubic feet (mcf). In Europe, it goes for around $11 per mcf. And in Asia, it sells for approximately $17.

These price discrepancies present a huge opportunity for investors ...

In the U.S., gas production has jumped 20% in the past five years. The International Energy Agency (IEA) reports that last year, the U.S. was the world's second-largest producer behind Russia. The difference in production volumes between the two was a minuscule 3.8%.

Last year, Russia produced 677 billion cubic meters (bcm) of natural gas, 20% of the world's total supply. The U.S. produced 651 bcm, 19.2% of world production. Russia exported about 29% of its production, which made it the No. 1 exporter.

You might expect that, as the world's No. 2 producer, only a fraction behind top dog Russia, the U.S. would also be among the world's largest exporters.

But we're not. The tiny Arab nation of Qatar – with 2 million people, its population is roughly the size of Houston – claims the title of No. 2 global exporter, behind Russia.

It produces about 151 bcm a year. That's about 4.5% of the world's annual total... but it ships out nearly all of it – 119 bcm. And resource-rich Australia is ramping up natural gas production for export. Experts say Australia will surpass Qatar in exports by 2017.

Even though the U.S. is producing a huge surplus of natural gas, we export essentially none of it. U.S. producers want to export their product to higher-paying markets... But right now, the U.S. has no operating export facility.

Cheniere Energy, a company I recommended last July in my Investment Advisory, will be the first. It's constructing a huge LNG export terminal in Louisiana. It expects to start operating in 2015.

The company has already signed a 20-year supply agreement with the Spanish natural gas infrastructure and utility company Gas Natural. The Spanish company agreed to buy 3.5 million metric tons of LNG annually... beginning in 2017. Chenier also struck a 20-year deal with the United Kingdom's oil and gas company BG Group. And other customers that are lined up include the Indian gas transmission and marketing company GAIL India Ltd and the Korea Gas Corp.

But Cheniere is not the only opportunity out there. This abundance of natural gas is one of the biggest economic trends of my lifetime. And the world needs a lot more LNG infrastructure. Things like LNG export terminals, LNG tankers, and storage-and-distribution facilities.

According to an estimate by trade group Interstate Natural Gas Association, North American industries need to invest $6 billion-$10 billion per year to maintain the storage network capable of handling the growth in production.

I've pointed out this opportunity to you before. In April, I wrote:

While the surplus of natural gas in the U.S. has most people bearish on the sector, I'm bullish. I know it's impossible for a surplus of energy to exist for long. I know billions will be spent making natural gas a global fuel... with a global price. And I know it will be a boon to companies that transport or are preparing to transport LNG.

Good investing,

Porter Stansberry

Further Reading:

In August, Porter put together a two-part series detailing the potential of this long-term energy boom. In Part I, he explained how America is on its way to being the world's largest energy producer and one of the largest energy exporters. And in Part II, he showed the two numbers that are proving this prediction is coming true. Read the series here and here.

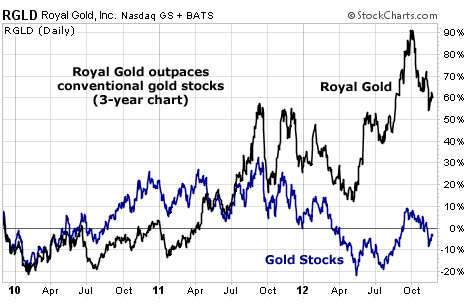

Market NotesTHIS IS WHY WE LIKE ROYALTY COMPANIES Today's chart shows you why we like royalties.

Regular DailyWealth readers are familiar with the idea of precious metal royalty companies. We've written about them dozens of times. Royalty companies don't mine any gold or silver of their own. Instead, they finance lots of early-stage mining projects, then earn royalties on mine production if things work out. This is a safer, more diversified way to invest in the gold-mining business, rather than owning a company focused on one big strike... or a conventional miner with escalating production costs.

One such royalty firm is Royal Gold. Royal Gold owns a portfolio of more than two dozen royalties located in mining-friendly countries. It's one of the "go to" royalty firms knowledgeable investors buy for exposure to precious metals.

Today's chart shows you how our idea is working. It plots the performance of Royal Gold (the black line on the chart) versus the large gold stock fund GDX (the blue line) over the past three years. As you can see, Royal Gold is up more than 60%, while conventional gold stocks have declined a bit. Life is good as a royalty owner.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|