Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The Facts About One of the Biggest Energy Trades of the DecadeBy

Friday, December 14, 2012

If you accept the bunk you read in the mainstream media about nuclear energy, you're going to miss out on a big opportunity...

Earlier this week, I showed you how countries will be forced to use a growing amount of nuclear power... no matter what the politicians say. Basic economics will override speechmaking. It's inevitable. And Japan, for example, is already pursuing new sources of uranium, which powers nuclear plants.

That's a smart move. Uranium supplies are looking tight, especially in the face of potentially explosive new demand. Let me show you what I mean...

The growth in nuclear power centers on China, India, and Russia. These huge populations remain among the lowest consumers of electric power in the world. And in those countries, nuclear power should flourish. According to British Petroleum's "Energy Outlook 2030" study, the countries will increase their use of nuclear power 7.8% per year through 2030.

That means the nuclear power demand from those countries will more than double by 2020 and will quadruple by 2030.

To put that into a more global perspective, the world has 436 active nuclear reactors today with a total capacity of 374 gigawatts (GW). Another 62 reactors are under construction and will add 63 GW of capacity.

Each gigawatt of increased capacity requires about 200 metric tons of uranium per year. And the first fueling for new reactors requires between 400 to 600 metric tons of uranium, according to the World Nuclear Organization. So the 62 new plants will need a minimum of 25,000 metric tons of uranium in their first year of production and 12,400 metric tons per year after that.

According to the World Nuclear Organization, total demand for uranium will hit 67,990 metric tons in 2012. The 62 plants under construction will jack up that number by 18%.

And think about this... another 484 reactors are either on order, planned, or proposed. China alone accounts for 171 of those planned reactors. India accounts for 57 and Russia the other 44. These potential reactors represent 542 GW of electric power. If those reactors are built, they will more than double the existing nuclear fleet.

At the same time... the supply side of the equation isn't keeping up, thanks to the economic turmoil, huge capital costs, and negative public sentiment toward nuclear power.

The highest-profile supply problem was BHP Billiton's decision to delay its Olympic Dam mine expansion. That took 14,545 metric tons of uranium per year off the table. In addition, the Kazakhstan government shelved about 4,500 metric tons of new projects.

Here are other notable delayed or shelved projects...

As you can see, about 29,550 metric tons of uranium per year of expected supply has been waylaid. This could create a substantial supply pinch over the next few years.

Again, it's basic economics. When supplies are low and demand is high, prices will rise. In my next essay, I'll show you how enormous the gains can be when uranium prices enter a "boom" phase. Until then...

Good investing,

Matt Badiali

Further Reading:

"There's just no way the world can work without nuclear energy playing a prominent role... no matter what the politicians say," Matt writes. Read his argument – and learn one of the most important questions facing natural resource investors – here: The Big Nuclear Energy Lie.

"Uranium may finally be ready to stage a big 'bad to less bad' rally," Brian Hunt writes. He shared a low-downside, high-upside bet in uranium. Read more here.

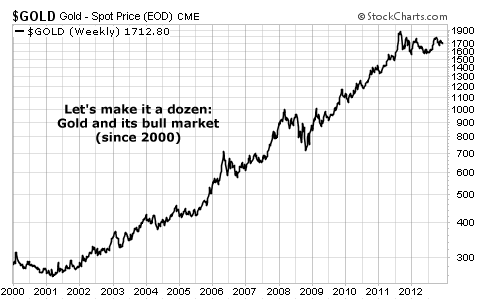

Market NotesGOLD IS GOING TO MAKE IT 12 CONSECUTIVE YEARS As we near the end of 2012, gold looks likely to register the incredible: 12 consecutive years of price gains.

Longtime readers know that ever since we started publishing DailyWealth in 2005, we've been outspoken bulls on gold. (We were gold owners and gold bulls years before that even.) Since then, we've published hundreds of essays on the right ways to own it. We even published a book on the stuff. We've helped thousands and thousands of people make big gains in gold.

At the end of 2011, gold registered its 11th consecutive year of gains. This is an extreme anomaly in the financial markets. No other widely traded asset has registered this many consecutive years of gains in over a hundred years. So it was only natural to think gold might be due for a "break."

That break didn't come in 2012. Western governments are still trying to spend and borrow their way to prosperity, which devalues their currencies. Asia is still emerging as a sizable accumulator of gold. This is all driving gold to close 2012 higher than where it started. The "Currency Trade of the Millennium" will tack another year onto its string of success.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|