Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Two Dangerous Mistakes Smart Long-Term Investors Often MakeBy

Wednesday, January 9, 2013

Capitalism is about capital – how much you earn and how much you keep.

I told you that last week... and reminded you that the single greatest investment secret ever discovered is to compound your money with extremely capital-efficient companies. These companies can generate massive returns for patient, long-term investors.

But as you're looking for these companies, you must keep two incredibly important risks in mind...

As I showed you, it's easy to spot capital-efficient companies: You compare a company's cash earnings to the amount of capital that's returned to shareholders through cash dividends or net share buybacks. The more capital a company can distribute, the better. Even if the company doesn't grow much, its shareholders will still become extremely wealthy.

Here's the thing: Not all of the companies that pass this "test" are worth owning.

Obviously, you can't ignore the basics of valuation. If you pay way too much for these businesses, your returns will disappoint. Beyond the basic value determination, the capital-efficiency approach has two significant problems.

First, a lot of companies – especially resource companies, like gold miners or oil producers – convert assets on their balance sheets (reserves) into cash earnings. These firms can sometimes look far more capital-efficient than they really are because they delay the purchase of additional reserves for a long time.

You have to be careful to accurately measure the real costs of the company's production – including the costs to replace reserves. You can do this by measuring capital efficiency across a long period of time, typically 10 years. This allows you to measure a company's capital-investment expenses even when they're infrequent.

Second, this kind of analysis tends to highlight one type of company... the so-called "value trap." These companies appear to be great values because they throw off nearly all the cash they generate... but they're doing so only because their products and services are rapidly growing obsolete. These companies are essentially in "runoff" mode.

"Runoff" refers to an insurance company that's gone bust because the expected claims it faces are more than the capital it can raise. It exists only to pay out cash until it's all gone. The same thing happens to companies whose products have grown obsolete. Imagine a pay-phone manufacturing and servicing business. Or a CD case maker. Or Kodak. The iconic filmmaker didn't need to build new chemical plants or develop new kinds of chemical-film products because demand for chemical film was disappearing.

Investors frequently believe they can manage these kinds of permanently declining businesses in a way that extracts all the cash each year... because there's really no ongoing business to invest in.

Avoid these situations at all costs. If there's even a hint that a business is involved in a product or service that faces long-term obsolescence, don't get involved. Ever.

I've seen many great investors – folks far smarter and wealthier than me – fall flat on their faces trying to beat a sales-decline curve with larger dividends. In my experience, it never works. Expenses and problems mount faster than cash can be paid out, almost every time.

Again... If you decide to focus on capital-efficient companies, your biggest risk is that you'll end up buying companies that can't grow at all. These companies often "look" good on the basis of capital efficiency. But they're not.

Fortunately, this risk is pretty easy to mitigate. Just ask yourself this question: Is it likely that my children or grandchildren will desire this brand and this product in 20 or 30 years?

Obviously, you can't answer this question with any real certainty. However, I can say without hesitation that my kids and grandkids are likely to enjoy simple, branded consumer products known for consistent quality and consumer loyalty... such as Hershey's chocolate... Heinz ketchup... Coca-Cola's soft drinks... and McDonald's hamburgers.

Like I said last week, these are "high class" companies. They don't have to spend much money investing in their businesses because their primary asset is their well-established, good reputation. They won't grow rapidly. But they will likely make shareholders who buy at the right price rich for decades to come.

Good investing,

Porter Stansberry

Further Reading:

"Most people think Warren Buffett became the richest investor in history – and one of the richest men in the world – because he bought the right 'cheap' stocks," Porter writes. "The truth of the matter is entirely different." The secret to Buffett's approach is buying capital-efficient companies. And Porter calls it the only sure way to get rich in stocks. Read more here.

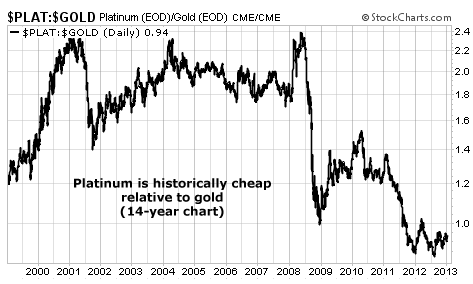

Market NotesONE OF THE FEW CHEAP ASSETS LEFT Now that stocks have hit a five-year high, it's getting harder and harder to find investment bargains. One asset that might qualify is platinum...

Platinum is technically a precious metal, which means many people see it as jewelry and a "store of wealth," like gold. But platinum also serves as an industrial metal. It's used heavily in automobile production.

Since platinum is heavily used in industry, global economic worries have depressed its price. The metal is down 17% from its 2011 high. It's also become very cheap relative to its precious metal cousin, gold.

You can see platinum's level of cheapness in the chart below. The chart tracks the ratio of platinum to gold. For many years, an ounce of platinum was twice as expensive as an ounce of gold, and this ratio stood around 2. But since the credit crash, this ratio has fallen below 1. Platinum is cheap relative to gold. If the global economy keeps ticking higher, it won't stay that way for long.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|