Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Why I'd Buy Intel Over AppleBy

Wednesday, February 20, 2013

There aren't very many genuine technology companies.

Instead, almost all of the companies people call "tech stocks" are really companies that use technologies to make or to sell their products. They have no real technological advantage whatsoever. As a result, it is difficult for them to achieve the kind of scalability (expanding profit margins) that is the hallmark of great tech companies.

To me, the definition of a tech stock is based on the nature of the moat that surrounds its business and protects it from competition.

In short, is the company's competitive advantage based mainly on the technological superiority of its products? Are these technologies proprietary? And most important, are these products tremendously scalable? Will the gross profit margins of the business grow as volume ramps up?

Consider semiconductor giant Intel (NASDAQ: INTC), for example. Intel takes sand (silicon) and applies decades of research and engineering to turn it into the heart of the modern world – computer chips. The moat around its business is both high-tech expertise and intellectual property. It is difficult (impossible, really) to compete against Intel in the microprocessor market, where it has tremendous scale.

That's because most of Intel's costs are fixed. It takes a lot of capital to build fabs (the plants where Intel's chips are made). It takes a lot of capital spent on research and development (R&D) to produce faster and faster chips. And it takes a lot of money to hire and retain the brilliant engineers to design the chips and the patent attorneys to protect the chips. But it doesn't cost much at all to make each additional chip. This lack of marginal costs (and the large size of the fixed costs) is what makes tech stocks so interesting for investors.

From 2010 to 2012, Intel's business grew – a lot. The company sold $10 billion more in chips last year than it did in 2010. But the company's costs to make these extra chips only increased by $5 billion. Thus, the more chips Intel sells, the bigger its margins get.

This fact makes the microprocessor market a natural monopoly. As Intel gets bigger, it can afford to spend more and more on R&D... which makes its chips bigger, faster, and better than its competitors'. The R&D makes its products better in a tangible, objective way. That, in turn, allows Intel to sell more and more chips at higher and higher prices... and earn wider and wider margins.

I realize the stock market hasn't been impressed with Intel's earnings lately. I think investors are making a huge mistake.

Wall Street puts far too much emphasis on sales growth. It ignores the quality of a company's earnings and the moat around its business. Yes, on a percentage basis, Intel's growth is slowing because it is already such a big business. But consider the quality of those earnings...

Last year, Intel earned more than $20 billion in cash. With this huge profit, Intel spent more than $16 billion returning capital to its owners via cash dividends ($4 billion) and share buybacks ($12 billion). In short, shareholders at Intel kept 80% of the profits.

Please make sure you understand what this means... Intel is a $100 billion business. The current shareholder yield (cash and share buyback) is now over 16%.

Let's compare that to Wall Street's current darling, Apple (NASDAQ: AAPL).

Apple designs consumer products that use mostly other people's technology. The big difference is that Apple is also a software company. Its software is truly excellent, so we'd qualify Apple as a legitimate technology company. The question is, does it truly compete on the basis of technology... or on the basis of design and brand? I believe it mostly competes on brand and design. Thus, it will be harder (and more expensive) than most people think for Apple to remain as dominant as it is today. It will be harder for it to maintain its profit margins because it's not competing on the basis of pure technology.

Apple is a $450 billion company. It earned $50 billion in cash last year. How much of that vast richness did its shareholders get? Almost nothing – $4.5 billion in total dividends (cash and net share buybacks). The company kept more than 90% of its earnings.

I know the market (and most of you) will not agree with me, but trust me on this... Intel is a much better investment than Apple.

Intel is a real technology company. Its products are objectively better than its competitors' and that advantage is maintained via R&D spending and patents. It will be incredibly difficult for anyone to compete with Intel effectively in microprocessors. Apple, meanwhile, depends far more on design and consumer preference for its competitive advantage.

While I love Apple products today, I never used them until about 2006. The public taste is fickle. It is not hard to imagine that someone... a new Steve Jobs... could come along and put together phones and computers in a new and better way.

Apple realizes that too, which is why it wants to keep such a huge cash hoard (now more than $150 billion). Intel doesn't need a stockpile like that... so it can return more of its profits to its shareholders. I'll let you decide which company is the "real" tech stock.

Today, by the way, investors value Apple at $400 billion (enterprise value, which doesn't include the company's cash hoard). Intel is only worth about 25% of that amount ($100 billion enterprise value).

It's a safe bet that Intel's stock will outperform Apple's over the next decade.

Good investing,

Porter Stansberry

Further Reading:

In September, Steve warned DailyWealth readers of a potential peak in Apple's share price. Four months later, shares are down 33%. "Many investors are left wondering if now is the time to buy," he wrote last month. "My answer is simple... While it might seem like a great time to buy Apple, I wouldn't put a dollar into the company today." Get the full story here: Down 33% in Four Months... Is it Time to Buy Apple?

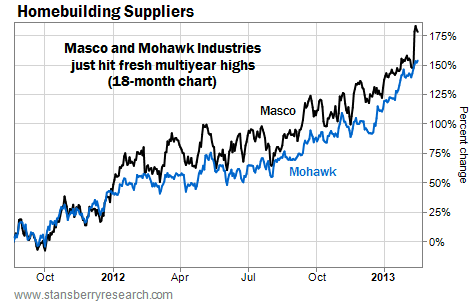

Market NotesTHE LATEST SIGN OF A BOOM IN HOUSING Today's chart offers further evidence that there's a massive recovery happening in the housing market.

Regular DailyWealth readers have heard a lot about the housing market over the past couple years. Steve Sjuggerud has called it the "most awesome opportunity in American history." To make his case, he's cited record-low mortgage rates, improving home sales data, and a renewed uptrend in housing prices.

The latest positive sign for the housing market comes from companies that supply "fixtures" to the homebuilders. Masco (NYSE: MAS), for example, sells billions of dollars of faucets and cabinets each year. And Mohawk Industries (NYSE: MHK) is the world's largest flooring manufacturer. It sells everything from carpet to tiles to hardwood. These companies are "bellwethers" for the homebuilding sector – after all, you can't build a house without the supplies they manufacture.

As you can see in the chart, shares of Masco (black line) and Mohawk (blue line) just hit fresh multiyear highs. While both companies' latest financial results showed sales barely grew last year, the market is expecting business to pick up in 2013. That means a major jump in homebuilding activity… It's also another sign the housing uptrend is just getting started.

– Larsen Kusick

|

In The Daily Crux

Recent Articles

|