Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's Note: Last year, we ran a special series in DailyWealth: Our colleague Dr. David Eifrig covered simple ways to protect yourself, your family, and your money from dangerous government and criminal intrusion. It was a little different from our usual investment-focused content... but the response was tremendous. So today, we're featuring more commentary from "Doc" on how to keep your wealth and your identity safe. A Big Privacy Risk That Could Cost You Your JobBy

Thursday, March 7, 2013

Major Zane Purdy's life imploded in just three months...

Purdy, a defense contractor and Air National Guard officer, used to earn a six-figure salary. Then, according to the Montgomery Advertiser, thieves stole his identity. They decimated his credit rating.

Bad credit or excessive debts flag someone as a national security risk. Purdy had his top-secret security clearance revoked. His company was forced to fire him. Even the Air National Guard couldn't bring the 18-year veteran back onto active duty.

Now, the father of two is waiting tables for $7.25 an hour... he has tax liens levied against his property... and the IRS is claiming he owes them more than $10,000 in back taxes.

He's not the only one whose life was turned upside down...

The person who stole Purdy's identity was a data-entry clerk at a nearby hospital. She stole more than 800 patients' personal information. She had access to names, Social Security numbers, birth dates, and addresses. She sold this data to a unique brand of scammers – experts in manufacturing "synthetic identities" – for $8,000 in 2010.

By 2012, they had turned this personal-information stash into $1.6 million.

A typical fraudster racks up charges as soon as he gets access to the victim's account. This restricts the size of his take to the account's preset limit. The "synthetic" process takes longer than conventional credit fraud... but the returns are higher.

Over time, the crooks use these conjured persons to open bank accounts, start fake businesses, get personal and corporate credit cards, take out home and auto loans, and file tax returns. In the beginning, they pay bills and establish superior credit ratings. Once the credit nozzles open up, look out...

NBC News reports a handful of these synthetic identity thieves in New Jersey stole at least $200 million over the last six years. The group gathered small snippets of personal data – stolen utility bills here, pilfered Social Security cards there, hacked online logins elsewhere – and used them to stitch together fake credit identities.

The FBI determined the criminals manufactured at least 7,000 synthetic identities. Banks issued them 25,000 fake credit cards. They established at least 169 fake bank accounts... through which $60 million in cash flowed out.

Current law allows everyone a free peek at his or her credit reports once per year. Conventional wisdom says that's enough to protect you from identity theft. But with this new threat, it's not. Your information may already be part of a synthetic identity... and your credit score could still look amazing. What you need to know is whether new accounts are being opened in your name.

A few services charge by the month to monitor your credit report. The services start at around $10. They'll alert you to any newly opened accounts or other suspicious activity. One of them, LifeLock, offers a $1 million guarantee if your identity gets stolen on its watch.

There are other ways to take even more control over your credit profile. For example, the law allows you to force credit-ratings agencies to notify you of new activity. You can even make them freeze your credit outright. These actions may also be free, depending on your age and home state. Search for "freeze" on any of the three credit bureaus' websites – TransUnion, Experian, and Equifax – and follow their instructions.

These identity thieves succeed because most folks don't have the right protections in place. But these protections are cheap... and easy to set up. There's no reason not to take action right now.

Take just a few minutes and just a few dollars, and you can reduce the chances of a synthetic identity thief turning you into the next Major Purdy.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Last year, in a special four-part holiday series, Doc showed DailyWealth readers several ways to protect your money, your family, your health, and your privacy. Learn how to avoid the worst kind of government intrusion... how to take control of your retirement money... one of his favorite ways to "dodge" taxes... and the most dangerous "everyday" threat to your privacy.

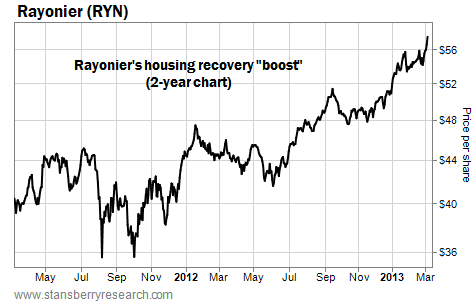

Market NotesTHIS IS WHY TIMBERLAND IS SOARING IN VALUE Yesterday, we highlighted the bull market in lumber. And if it's a bull market in lumber, it's a bull market in timberland company Rayonier (NYSE: RYN)...

Longtime readers know we consider timberland – bought at a good price – to be one of the world's greatest investments. Trees grow relentlessly. Harvesting them produces cash flow. And if lumber prices are low, you can opt to leave the trees in the ground until better prices arrive. (Read this educational interview for the full story.)

As we detailed yesterday, the U.S. housing recovery has caused lumber prices to skyrocket. This has produced a big rally in timberland stocks like Rayonier. This company is one of the few "pure play" timberland stocks available to investors. Surging lumber prices provide a big boost to its earnings and land values.

You can see this boost in the two-year chart below. Rayonier has returned investors more than 50% in capital gains and dividends. Shares are near an all-time high. Life is good for timberland investors.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|