Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The First Chinks in Housing's ArmorBy

Tuesday, July 2, 2013

My favorite idea for the last couple years has been U.S. housing...

The idea is simple. It's based on the fact that TWO once-in-a-lifetime things have come together. We're dealing with...

This has made U.S. houses more affordable than ever. It's been the perfect recipe for rising house prices. But all of a sudden, those two things are changing... We're seeing the first chinks in housing's armor.

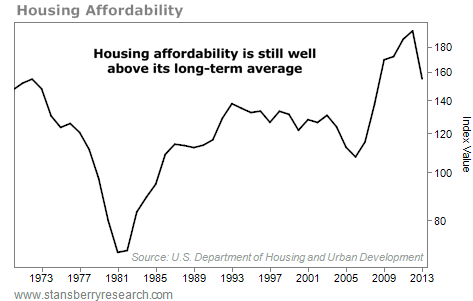

House prices are up a lot. And mortgage rates are up a lot. This means housing affordability ain't what it used to be...

House prices have soared this year... up to a nationwide median of $208,000 (for existing homes). That's up from $173,000 in February. (To be fair, home prices are typically weaker in the winter.)

Also – and possibly more importantly – mortgage rates have soared. They've climbed over a full percentage point – from below 3.4% in May to around 4.4% today.

These are two serious chinks in the great housing story.

Fortunately, I have some good news for you...

It is true that houses aren't nearly as affordable as they were even just a few months ago. However, you need to understand that house prices can still soar dramatically from here...

Outside of the bubble of 2006, the greatest boom in house prices was in the 1970s. House prices soared from roughly $20,000 to roughly $60,000 in that decade. Importantly, that boom started from the last great period of housing affordability.

So the good news today is, even with the recent dramatic fall in housing affordability, we have only fallen to the starting point in affordability in the 1970s.

The chart below shows what I mean:

This chart is yearly housing affordability. Since 2013 hasn't ended yet, it is based on today's house price and mortgage rate.

I hope you took me up on my advice to buy property in the last few years. It was a once-in-a-lifetime opportunity.

Fortunately, the opportunity today is still great – even with higher home prices and higher mortgage rates.

Today, we are at the same level of affordability that we were when house prices soared roughly threefold in a decade (in the 1970s).

I'm not saying that we'll see a repeat of the 1970s... What I'm saying is this: Yes, house prices and mortgage rates are up. But even with those dramatic moves, housing is still affordable... And there's still plenty of upside potential left.

Take advantage of it... soon!

Good investing,

Steve

Further Reading:

"The U.S. Federal Reserve has tricked people into spending money again," Steve writes. He's seeing evidence all over his small Florida hometown. He describes one unique economic indicator here: Running Out of Cousins... The U.S. Boom Is Back.

How high can home prices in in the U.S. go? To answer that, Steve says, you just need three simple numbers. Find out what they are right here.

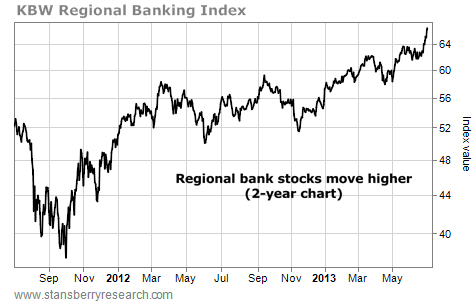

Market NotesA BIG MOVE IN REGIONAL BANKS Yesterday's price action confirmed it: It's a bull market in regional bank stocks.

Last Friday, we published a chart of regional bank stocks. We noted how banks "partied hard" during the 2003-2008 bull market in stocks, real estate, and commodities. Banks crashed in 2008... and then spent years in a "hangover" period.

Regional bank stocks aren't your typical "too big to fail" megabanks. They tend to practice a more traditional model of banking, rather than run big trading operations. They benefit when their regions enjoy good economic conditions and rising asset values.

A handy way to track this sector is with the KBW Regional Banking Index. It's a widely followed gauge of regional banks. Last week, we noted the bullish price action in this index. Just yesterday, it jumped nearly 3% to reach a new multiyear high... It's a bull market in regional banks.

|

In The Daily Crux

Recent Articles

|