Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: We're continuing our weeklong series on the elite class of stocks we truly believe every individual investor should own. Yesterday, we showed you how steady, high rates of dividend growth from these businesses can lead to double-digit annual returns. Today, we explain what makes these companies the best investments in times of crisis...

An Income Investment Secret Wall Street Doesn't Want You to LearnBy

Thursday, August 22, 2013

The 2008 credit crisis offers a tremendous lesson for folks interested in generating income from their investments.

You're not going to hear this from your broker. He doesn't want you to know.

But if you learn this lesson, you'll find it indispensable in the years to come...

The lesson is that chasing income through stock in highly leveraged companies – like most finance and real estate vehicles – can be a killer.

Many finance companies and real estate firms take on lots of debt to conduct business. They are such low-profit-margin businesses, they have to "lever up" in order to achieve good returns on capital. They can only exist with continuous debt financing. If this debt financing seizes up, as it did in 2008, it's like the oxygen leaving a room for these guys. If they don't have that constant financing, their share prices collapse. No amount of income will allow your portfolio to recover from a near-total loss.

There is an income investment where you never have to worry about that. Ever. These investments sailed through the crisis, paying... and raising... their dividends the whole way. If you're tired of getting killed by every ludicrous, leveraged sham Wall Street thinks up, this investment is where you want to be.

Before I get to that, though, let me back up and show you how poorly traditional income investments are set up to withstand trouble...

Thornburg Mortgage was a real estate investment trust (REIT). It was a great company. It never lost a penny investing in mortgages since the day it started up in 1993. Thornburg returned an average of about 14% a year to investors, most of it in dividends, from 2000 to 2007.

Thornburg's stock carried a double-digit yield. But in 2008, Thornburg was hit with $600 million in "margin calls." Its mortgage assets were falling in value due to the ongoing mortgage crisis. Thornburg's lenders needed $600 million in additional cash – which it didn't have. It had to sell its high-quality mortgages for less than it paid so it could stay in business. Thornburg's problems worsened, and it eventually declared bankruptcy and ceased all operations.

Thornburg knew what it was doing. The business performed well for over a decade. Its only problem was that it carried $13 billion in debt. Shareholders saw the stock drop from $140 a share to less than $1.40.

I hope you see what I'm getting at here. Investors eager for high current yields often buy leveraged junk – junk dreamed up by Wall Street. When trouble hits, junk gets outed and the investors suffer.

But there was one group of stocks that raised its dividends in 2008 and 2009: World Dominating Dividend Growers.

As DailyWealth readers know, World Dominating Dividend Growers are big companies that are No. 1 in their industries. They dominate their markets, obliterate competition, gush cash, pay rising dividends year after year, and – since they don't yield double digits right this second – are generally underappreciated by the average income investor.

But in a crisis, your income investment couldn't be safer. Remember, these are the biggest, strongest companies in the world... and their fortress-like balance sheets allow them to march through tough times.

Take dominant payroll processor Automatic Data Processing (ADP), for example. It carries very little debt, less than $15 million versus a $34 billion market cap.

More important for income investors, on November 18, 2008 – with global financial markets in a panic – ADP raised its quarterly dividend 14%.

The same thing is true of other World Dominating Dividend Growers...

Wal-Mart – the world's biggest retailer – issued $1 billion of new debt in January 2009, at rates as low as 3%. And in March 2009, when the world looked like it was coming to an end, the company raised its dividend almost 15%.

Now... you might argue, World Dominating Dividend Growers' share prices fell along with others in 2008 and 2009. But unlike most other stocks, the World Dominators were never in any financial danger.

They just became better investments during the crisis. Investors were able to buy them more cheaply.

By far the best, safest stocks to buy are World Dominating Dividend Growers at a great price. Yes, their share prices can drop, just like any other stock. You don't have control over that. But even if their share prices suffer, they'll still be safe, financially strong companies that raise their dividends year after year. They'll still be great businesses that will prosper for years to come.

Wall Street would rather you not invest in these companies. It wants you to buy the leveraged stuff so it can collect banking fees...

That leveraged stuff usually sounds new and exciting. But great investors avoid "new" and "exciting." They prefer "been around a long time, through everything" and "safe and steady cash flow." They prefer "sleep at night" income investing.

They prefer World Dominating Dividend Growers.

Good investing,

Dan

Further Reading:

"Exciting stocks" – companies that often have a hot new product... or a fantastic "story" – are what most investors like to buy, Brian Hunt writes. But "the average 'spectacular' company is almost sure to destroy most investors." Brian says if you're interested in making a meaningful, long-term stock investment, elite "stable" companies are the Holy Grail. Learn more here.

"In simple terms, a share of stock represents a share of an actual business," Dan says. And the majority of investors would make a lot more money if they learned to approach stocks the way they'd approach ownership in a business. Find out how to start "valuing a stock as a private business owner would" here.

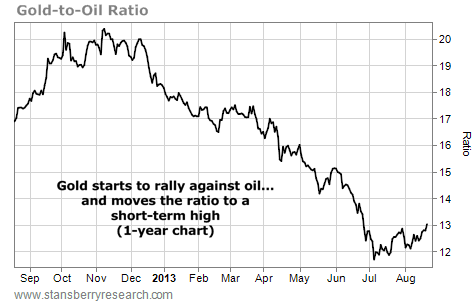

Market NotesGOLD BEGINS TO RALLY AGAINST OIL As we expected, the "gold-to-oil" ratio is working in gold's favor...

Back on July 26, we noted how the "gold-to-oil" ratio was ready to snap back in gold's favor. At the time, we reminded readers how this kind of "ratio trade" isn't a conventional "buy a stock and hope it goes up" trade. "Ratio trades" involve trading one asset against another asset. For example, one of the most important ratios in this group is the "gold-to-oil" ratio.

Since they are both commodities that have intrinsic value, gold and oil can be affected by the same buying and selling pressure in the market. But their values can get "out of whack." When this happens, traders can step in to sell gold and buy oil... or buy gold and sell oil. The profit on these trades depends on how the two assets move against each other. We used this analysis to time – almost to the day – the epic 2008 bottom in crude oil.

From late 2012 through last month, the gold-to-oil ratio fell from 20 to 12. This means gold collapsed in value relative to oil. In our July note, we pointed out that this decline left gold and oil in an extreme position. Hedge funds held extreme bearish bets on gold... and extreme bullish bets on oil. As you can see from the chart below, our note was well-timed. The gold-to-oil ratio has bottomed... and just staged a short-term breakout in gold's favor. This rally will continue.

|

In The Daily Crux

Recent Articles

|