Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Warren Buffett's Biggest Mistake...By

Wednesday, February 12, 2014

Today and tomorrow, I'd like to share with you part of a larger research project I've been working on for the last six months or so.

It involves an unusual investment lesson from the greatest investor of our time, Warren Buffett.

So, if you feel like learning something valuable, please continue reading...

One of the best educations that you can give yourself in investing is simply reading the annual letters Warren Buffett writes to the shareholders of his holding company, Berkshire Hathaway. (You can read them for free at www.berkshirehathaway.com. Also, a new book compiling all of his letters can be read on e-readers like Amazon's Kindle. It's well-worth the price, as it makes his writing searchable.)

To better understand Buffett's methods, I've been studying his mistakes. You always learn more by studying when something doesn't work.

It's like Buffett's business partner, Berkshire Hathaway vice chairman Charlie Munger, says: "Just tell me where I'm going to die, so that I won't go there." What he's really saying is, tell me how and why an investment approach fails, and I will learn how to improve upon it.

Improving upon Buffett? You might think that sounds like hubris or idiocy.

But the truth is... since the late 1990s, Buffett's performance (as a stock picker) hasn't been special. After averaging annual gains in the mid-20% range for most of his career, Buffett's portfolio of publicly traded equities has only averaged about 6% a year since 2000.

And for the first time in his entire career, Buffett will announce sometime later this year that Berkshire's book value did not increase faster than the S&P 500 over the last five years.

Buffett has beaten the S&P 500 over every other five-year period since the mid-1950s. The reason Buffett did not beat the S&P 500 over the last five years was because of poor stock picking. Berkshire's wholly owned businesses have performed well.

Buffett (and many others) will likely attribute this declining performance in stocks to Berkshire's portfolio size. Don't believe it. The two other managers who work with Buffett on Berkshire's portfolio both beat the market easily. But Buffett still manages the lion's share of capital. And he made one big, uncharacteristic mistake in the last five years... He chased a commodity boom.

During 2007 and 2008 – as oil prices soared to $150 per barrel on talk of "Peak Oil" – Buffett invested $7 billion in major oil firm ConocoPhillips. It was the single largest investment Buffett had ever made at the time. Within 12 months, he would sell most of the stock at a huge loss to free up capital for other investments. By then, the damage was done: ConocoPhillips cost Buffett several billion dollars. It was, by far, the worst investment he has ever made and probably his only genuine "blow up."

Buffett, who has always been completely honest with his shareholders about his mistakes, explained what happened in his 2009 letter:

Buffett started buying ConocoPhillips in 2007. He bought a little more than $1 billion worth of the stock and paid an average of $59.34 per share. It was a peculiar investment for Buffett to make. First... the stock wasn't cheap. Over the previous five years, ConocoPhillips' share price had risen from a split-adjusted $13 to $60. Even more uncharacteristically, Buffett kept buying even as the stock went much, much higher. By the end of 2008, Berkshire documents show the company held a little less than 85 million shares of ConocoPhillips, purchased at an average price of $85.35. As I mentioned earlier, the size of Buffett's investment made ConocoPhillips the largest publicly traded investment of Buffett's entire career at that time. The stock represented almost 19% of the total cost of Berkshire's existing portfolio and almost 15% of the portfolio's total value.

The same year that Buffett began buying ConocoPhillips shares, he described his overall strategy as an investor this way:

You don't have to be a cynic or a Buffett critic (and we're neither) to wonder about how a massive investment in ConocoPhillips could qualify as an investment for him. ConocoPhillips is a vertically integrated energy company, meaning it controls every step in the process from exploring and producing oil to selling refined gasoline. It produces and refines gasoline and other commoditized fuels and competes in global markets with virtually no barriers to competition. And why, we wondered, would Buffett make such a business his largest-ever commitment to a publicly traded stock? And why... why... would he ignore the inevitable commodity price cycle and continue to buy an oil company even as petroleum prices soared?

I think I know... And in tomorrow's essay, I'll explain why I believe that, for the first and only time in his career, Buffett got caught up in an investment "mania."

I'll also share two of the most fundamental lessons in resource investing... Lessons that could have saved Buffett and his shareholders billions of dollars...

Regards,

Further Reading:

"Most people think Warren Buffett became the richest investor in history – and one of the richest men in the world – because he bought the right 'cheap' stocks," Porter writes. "The truth of the matter is entirely different." The secret to Buffett's approach is buying capital-efficient companies. And Porter calls it the only sure way to get rich in stocks. Read more here.

Porter says the problem with buying high-quality, capital-efficient companies – and reinvesting the dividends – is that most investors don't have enough patience or common sense to pursue this approach... Get "the best investment advice you'll never take" here.

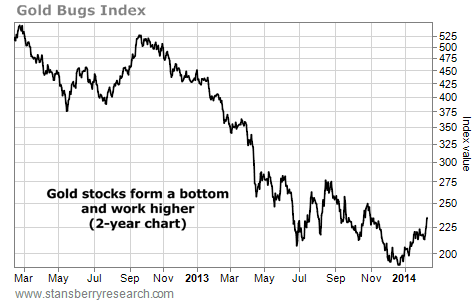

Market NotesOUR EXPECTED GOLD-STOCK RALLY IS HERE Another day, another sign that gold stocks have "put in a bottom."

Last month, we wrote bullish commentaries on both gold and gold stocks. We noted that after being out of favor and near "blown out" levels, gold and gold stocks looked good for a rally.

Over the past few weeks, gold and gold-stock prices have moved in the direction we expected. You can see this action in the chart below...

Our chart displays the past two years' trading in the benchmark gold stock index (the "HUI"). As you can see, this index suffered a huge fall in 2013. But check out the lower-right-hand side of the chart. You'll see that over the past few weeks, the HUI has climbed higher and higher. Just yesterday, shares broke out to their highest level since November.

Our expected gold rally is on...

|

In The Daily Crux

Recent Articles

|