Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

These Energy Loopholes Are Creating HUGE ReturnsBy

Friday, February 28, 2014

I'm sure – by now – you've read about the U.S. energy boom in publications like Forbes, Barron's, and the Wall Street Journal... You've surely seen analysts gushing about it on cable channels like CNBC or Fox Business... And I'm certain you've seen countless newsletter editors tout the opportunity.

But even with all the hype, most people still don't realize just how massive this trend really is...

It's producing incredible gains all over the place... in areas you might not consider...

We've been tracking all aspects of this boom for nearly four years in our Investment Advisory. (The word "fracking" didn't even exist when we started writing about it in May 2010... We spelled it "fraccing.")

In that time, we've scoured the markets looking for companies pursuing export strategies, because we believe the businesses that gather, refine, and export North America's excess energy will generate fantastic returns for their owners.

And so far, they have. Here's why...

Many people don't realize it, but it's actually illegal to export crude oil out of the U.S. And because it will likely take a long time for our politicians to get their heads out of the sand, we don't think this will change any time soon.

But the energy export market has two major loopholes... and we've been able to take advantage of both for excellent returns...

Export Loophole No. 1: Liquefied natural gas

Longtime readers know that we believe this theme is a slam dunk. The U.S. is now producing record amounts of natural gas. The spread between U.S. and Asian natural gas prices is unsustainable. For instance, natural gas in Japan sells for about three times as much as it does in the U.S. And we know several companies are racing forward – with access to nearly unlimited capital – to meet this demand.

One of our early recommendations on this trend was Cheniere Energy (LNG).

For years, it was the only company with approval from the U.S. government to export natural gas... We last recommended buying LNG stock in July 2012, when shares cost less than $15. The "mainstream" eventually caught on to this story... and we closed out the position last June for an 88.3% gain. Today, LNG is trading for nearly $50 a share.

More recently, our favorite way to invest in the trend has been Chicago Bridge & Iron (CBI). It's one of the world's foremost liquefied natural gas infrastructure construction firms. The company is building natural gas export terminals and pipelines all over the world.

And business is booming...

CBI's stock has returned 131% since we recommended it in June 2012... And on Wednesday, it smashed analyst earnings expectations again.

It also reported an increased "backlog"... which is the projects that the company has won but hasn't started working on yet (and therefore, have not yet been recognized as revenue). If a company's backlog is consistently growing, it's a sure sign that earnings and revenues will also grow. And that's exactly what has been happening with CBI.

Although the company is currently a "hold" in our portfolio, we expect the business to continue to thrive in the months ahead.

Export Loophole No. 2: Natural gas liquids (NGLs)

Propane and butane are two common NGLs (which are byproducts of oil and gas drilling). And propane has become extremely valuable in the global market. In the U.S., propane mostly grills burgers. But in much of the rest of the world, it's far more important. It fuels cars and heats homes.

Because they're naturally liquid (unlike liquefied natural gas, which has to be super-cooled to liquefy), they're easier to transport.

To export the NGLs, you need ports and ships, but not the immense cooling systems that liquefied natural gas projects require. Exporting NGLs is a fantastic business. And the next several years represent a "sweet spot" for NGL exporters. Until the natural gas export terminals are ready, NGLs will be one of the only major energy export opportunities.

We're so confident about this idea, we've dedicated a relatively large portion of our portfolio to the NGL export strategy. And it's working...

Although we've only been covering the strategy since December 2012, the average gain from this group of stocks is more than 38%.

We currently have at least one stock covering each step in the process of delivering NGLs to global markets (eight total)... from extracting it from the ground to shipping it in tankers around the world.

Many of these companies, such as Dominion Resources (D), are engaged in other aspects of the energy business besides NGLs. But that's kind of the point...

Most investors have typically looked at NGLs as an ancillary profit center... an offshoot of a company's "real" business. We believe it has become much more than that. And judging by the returns we're seeing – such as a 106% gain in Targa Resources (TRGP) – the market is beginning to catch on...

The bottom line is that we've been writing about the U.S. energy boom since 2010 – long before any other major publisher. Now, everyone is talking about it...

But it's still generating HUGE returns... in areas you probably haven't considered. And it's going to do so for a long, long time.

Good investing,

Bryan Beach

Further Reading:

Last year, Porter Stansberry put together a two-part series on America's rise to energy dominance. Porter calls it "the most important economic event of our lifetimes." In short, America is on its way to becoming the world's largest energy producer and exporter. Learn more here and here.

"After being held up for years, the giant natural gas boom is ready to happen," Frank Curzio writes. Last year, the government approved three natural gas export facilities. But Frank says nearly two dozen are awaiting approval: "I expect at least half of them to get it in the coming months." That's why it's time to buy in to this megatrend before it's too late. Get all the details here and here.

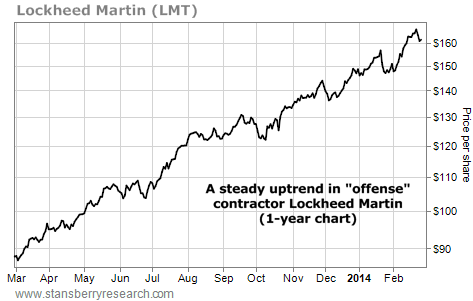

Market NotesTHE BULL MARKET IN GOVERNMENT SPENDING IS ON The U.S. government is still spending... and "offense" contractors are still raking in billions.

Last June, we noted how the U.S. is involved in so many foreign wars that defense contractors should be called "offense" contractors. We also noted that many analysts have warned against investing in this industry... due to an expected reduction in government spending.

That reduction hasn't come... And today's chart of "offense" contractor Lockheed Martin (LMT) is proof. The company produces things like jet fighters, missiles, radar systems, and unmanned aerial drones. Last year, Lockheed got 82% of its business from the U.S. government... And 2013 marked the third consecutive year of increased profits. Revenues were just 4% below all-time highs... which it reached in 2012.

As you can see below, Lockheed's shareholders have benefited from steady U.S. spending... Shares have risen 81% in the last year with almost no volatility. The dips have been minor and short-lived. The advances have lasted months. For better or worse, the bull market in government spending is on... and "offense" contractors are profiting.

|

Recent Articles

|