Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

How to Get Rich in Five Years or Less, Part IIIBy

Friday, March 7, 2014

My friend Dean wants financial freedom...

He wants to be able to afford to live where he wants, to spend his days doing something he enjoys, and to not worry about money. That's his definition of being "rich."

The other day, Dean and I were talking about how he could get there...

I shared with him the three greatest wealth-building ideas I know. The first was to join or start an ideal business (click here to read more)... The second was to compound his income by achieving a 10% raise every year (click here to read more).

Today, I'll share the final piece of advice I gave Dean...

For peace of mind – to really be free – Dean is going to need plenty of "go to hell" money.

This is a pot of savings that will allow him to walk away from a job or situation that doesn't work for him. It's the amount of money it will take for Dean to know he has the freedom to do whatever he wants.

And to get that, he's going to have to save like a squirrel in October.

My publisher Porter Stansberry wrote the best essay on the impact of being a good saver I've ever read. He wrote it for kids in their 20s... but it applies to anyone who wants to accumulate a big bankroll. You can read it right here.

Porter started with a 15-year-old and assumed a low salary ($9.50 an hour)... a very high savings rate (50% of gross pay)... a low investment return (5% after taxes)... and a long history of good raises (a 10% rate every year). He showed that this kid could have a nest egg worth $976,000 by age 40.

Dean is starting out ahead of our 15-year-old. So if he practices the same discipline, he'll have a quarter-million dollars by year five. That'll cover a lot of "go to hell" situations. If he sticks with it, he'll have a million-dollar savings account in less than 15 years. The key is to save a lot... and to continue to save a lot even as his compensation increases.

The temptation, of course, is to increase spending as income goes higher. As Porter writes, many people "tie their feelings about their self-worth to their spending, instead of to their net worth (their saving). They've badly confused the near-term experiences of living rich with the long-term goals of being rich."

Dean has modest tastes and good saving habits now. Like I told you on Monday, he drives an old motorcycle and wears old Converse shoes. If he can maintain these habits even as he grows his income, he'll have plenty of cash on hand to help him sleep at night.

In short, Dean might not realize it, but he's already closer to being richer than 99% of his peers.

He found a great job, he's doing what he enjoys and living where he wants. He's in a position to learn valuable skills and be well rewarded for them. He has so far avoided the trap of spending money he doesn't have.

He's taking the necessary step to get rich... to be free.

Are you?

Regards,

Further Reading:

Find more classic essays on wealth-building here:

How to Be Dramatically More Productive, Successful, and Wealthy

"It's so simple. But most people don't do it." The "Three-Bucket System" for Managing Money

Mark Ford used this system to generate more than $50 million in wealth. Two Simple Rules All 20-Somethings Should Know About Money

"By the time you're 40, you can be a millionaire, easily." Market NotesAN 'AMERICAN DREAM' BULL MARKET One of our top "real-world indicators" is telling us things are a heck of a lot better than the pessimists would have you believe.

Owning and maintaining a home is the American dream... And as long as folks are making that dream a reality, things can't be all that bad with the U.S. economy. Last week, we showed you Steve Sjuggerud's bullish call on housing has been dead-on... The U.S. home construction fund (ITB) had just broken out to a six-year high. Today, we're looking at one of the holdings in that fund...

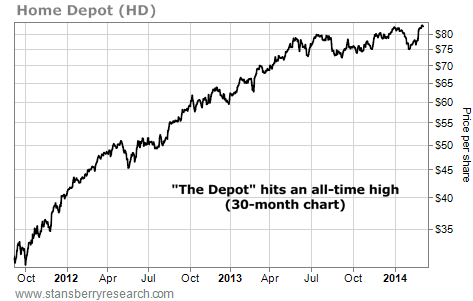

Home Depot is America's largest home-improvement chain. It sells the things we need to install new kitchens, remodel bathrooms, and build home additions. This makes its share price an excellent gauge of what's happening in America.

"The Depot" reported annual earnings last Tuesday. The company saw revenues just shy of $79 billion and earnings around $5.4 billion... Those are the best results in seven years and are near record levels. Shares responded by hitting a fresh all-time high. They're up 158% in the last two-and-a-half years.

The message in today's chart is clear. Things can't be all that bad... People are still spending money on the American dream.

|

Recent Articles

|