Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: In yesterday's edition, we shared one of our all-time most popular essays. It was written by our friend and wealth expert Mark Ford. In today's edition, we pass along another extremely popular idea from Mark. It's one of the most insightful ideas on retirement we've ever read...

The Biggest Mistake You'll Make When You RetireBy

Thursday, March 20, 2014

I consider myself to be an expert of sorts on retirement. Not because I've studied the subject, but because I've retired three times.

Yes, I'm a three-time failure at retiring. But I've learned from my mistakes. Today, I'd like to tell you about the worst mistake retirees make.

It's a common mistake... Yet, I've never heard it mentioned by retirement experts. Nor have I read a word about it in retirement books...

The biggest mistake retired people make is giving up all their active income.

When I say active income, I mean the money you make through your labor or through a business you own. Passive income refers to the income you get from Social Security, a pension, or from a retirement account. You can increase your active income by working more. But the only way you can increase your passive income is by getting higher rates of return on your investment.

When you give up your active income, two bad things happen:

First, your connection to your active income is cut off. With every month that passes, it becomes more difficult to get it back.

Second, your ability to make smart investment decisions drops because of your dependence on passive income.

Retirement is a wonderful idea: put a portion of your income into an investment account for 40 years and then withdraw from it for the rest of your life. Once you retire, you won't have to work anymore. Instead, you will fill your days with fun activities: traveling, golfing, going to the movies, and visiting the kids and grandkids.

But consider this: A retirement lifestyle for two, like the one I described above, would cost about $75,000 a year, or $100,000 before taxes.

How big of a retirement account do you need to fund that?

Let's assume that you and your spouse could count on $25,000 a year from Social Security and another $25,000 from a pension plan (two big "ifs"). To earn the $50,000 balance in the safest way possible (from a savings account), you'd need about $5 million, because savings accounts only pay 1% right now.

If you were willing to take a bit more risk and invest in tax-free municipal bonds (this is the safety level I like), you'd need about $1.25 million, assuming you could get 4% interest.

But middle-class American couples my age are trying to retire with an account in the $250,000 to $300,000 range. And that's where the trouble begins. To achieve an annual return of $50,000 on $300,000, you'd need to make 17% a year.

Getting 17% consistently over, say, 20 years may not be impossible, but it's very risky – too risky for my tastes.

I retired for the first time when I was 39. I put my money into ultra-safe municipal bonds. I soon realized, however, that to maintain the lifestyle I wanted, I would have to get a greater return on my investments – I would have to take greater risks with my money by investing in stocks. But when I studied the history of yearly stock market performance, I came to the conclusion that I couldn't confidently expect to get the return I needed, year after year.

So what did I do? I went back to work.

I went back to earning an active income because I didn't want to spend my days studying the market and my evenings worrying about my investments. And do you know what happened? The moment I started earning money again, I started to feel better.

Retirement isn't supposed to be filled with money worries. And yet, that is exactly what you will get if you try to get above-par returns on your investments.

As I write this, millions of Americans my age are quitting their jobs and selling their businesses. They are reading financial magazines and subscribing to newsletters. They are hoping to find a stock-selection system that will give them the 30% and 40% returns they need. But they will soon find out that such systems don't exist. They will have good months and bad years, and they will compensate for those bad years by taking on more risk. The situation will go from bad to worse.

It doesn't have to be this way. Let's go back to the example of the couple with the $300,000 retirement fund and the $100,000-a-year retirement dream. To generate the $50,000 they need, they would have to earn about 17% a year in stocks. As I said, that is highly improbable. But if they each earned only $15,000 in active income, they would need a return of only about 7% on their retirement account, which is doable.

There are many ways for a retired person to earn a part-time, active income. You could do some consulting, start your own Web business, or earn money doing any sort of purposeful work.

I am not saying that you should give up on the idea of retirement. On the contrary, I'm saying that retirement might be more possible than you think.

But you must replace the old, defective idea that retirement means living off passive income only. Paint a new mental picture of what retirement can be: a life free from financial worry that includes lots of travel, fun, and leisure, funded in part by active income from doing some sort of meaningful work.

The first benefit of including an active income in your retirement planning is that you will be able to generate more money when you need to. But the other benefit – the one that no one talks about – is that it will allow you to make wiser investment decisions because you won't be a slave to your investments.

Regards,

Mark Ford

Further Reading:

Contrary to popular modern belief, Mark says "the door to 'America's Millionaire Club' is not locked." If you have ambitions of being truly rich one day, read this.

And while Mark explains that "it's simply not possible to quickly turn, say, $25,000 into $1 million by investing in stocks," he says, "breaking the chains of 'financial slavery' can be done relatively quickly." If you're feeling financially shackled, here's what you must do...

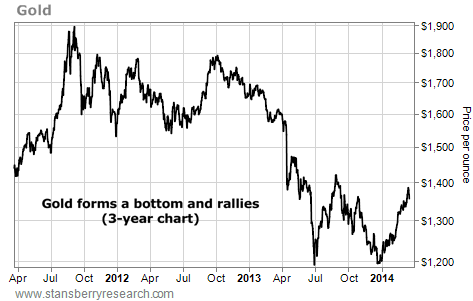

Market NotesGOLD HOLDS THE $1,200 LEVEL Gold held the $1,200 level... and the rally is on.

Longtime readers know that since we started publishing DailyWealth in 2005, we've been outspoken bulls on gold. We were gold owners and gold bulls years before that. Over the years, we've published hundreds of essays on the right ways to own it. We even published a book on the stuff. It's fair to say we're experienced with gold.

In 2011, worries about the global banking system sent gold skyrocketing to $1,900 per ounce. Then, it corrected to the $1,800 level... then to the $1,500 level... and then to the $1,200 level. The $1,200 level is where we guessed gold would bottom back in January.

As you can see from the chart below, our guess was well-timed. Gold has climbed from $1,200 to its recent high of $1,390. Even though gold has pulled back from its recent high, Asia is still buying lots of gold... and governments are trying to devalue their paper currencies (which is bullish for the currency they can't devalue, gold). The new gold rally should continue.

|

Recent Articles

|