Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Your Boss Wants to Give You a Raise… Don't Turn Him DownBy

Thursday, June 19, 2014

Are you skipping out on free money?

Yesterday, I shared some of the benefits of tax-deferred investing... and how simply opening up an IRA account can provide you with an instant 33% return because of its tax benefits.

Today, I'll cover another type of tax-deferred account that you likely have access to – a 401(k).

Most importantly, I'll show you how this type of account can help you earn "free" money, even before considering the tax benefits. It's much like getting a raise from your boss… yet many people turn down the offer.

Let me explain…

A 401(k) account is similar to an IRA. You make contributions before taxes, and the gains add up tax-free.

The key difference with 401(k)s: Your employer sponsors and manages it. And the employer often matches contributions up to a certain limit.

If there's one financial decision that absolutely every single person needs to make, it's this...

Always contribute to your 401(k) to earn the maximum employer contribution.

Skipping out on that free money is the most senseless mistake in personal finance. I cannot stress this enough: Employer 401(k) contributions are free money... Make sure you invest enough to claim the full benefit.

Take an employer that will match half of an employee's contributions up to 6%. That means if the employee sets aside 6%, the employer adds 3% for a total of 9%. That's an instant 50% return on your money... even more when you consider the tax effect.

The most you can put into your 401(k) in 2014 is $17,500. If you're older than 50, you can contribute $23,000.

The potential downside of 401(k)s is that they sometimes come with limited investment options. Your employer chooses a plan manager and works out the investment options that will be included. Most plans have a decent range of funds to choose from, but it can be hard to find good, low-cost funds for every one of your asset classes.

Talk to your benefits administrator and see if your company offers a self-directed 401(k). This type of account has all of the benefits of a 401(k) with none of the restrictions. It works just like a regular brokerage account and allows you to buy single stocks, options, exchange-traded funds (ETFs), or mutual funds.

For those who know nothing about investing – and who don't want to learn – the restricted 401(k) probably works just fine. But if you want to take more control of your financial future, convert to a self-directed 401(k).

Even armed with that knowledge, most investors still feel overwhelmed. But by skipping taxes (and possibly getting an employer's contribution), you've already made a huge investment gain. That 33% to 50% boost on your initial capital alone is worth it.

Don't leave that free money on the table...

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig Jr.

Further Reading:

Doc has been telling readers about one of his favorite long-term, low-risk investments – a group of stocks he calls "Digital Utilities." He says many investors would call these businesses "boring"... But "the mountains of cash they produce and return to shareholders are anything but..." Get all the details here.

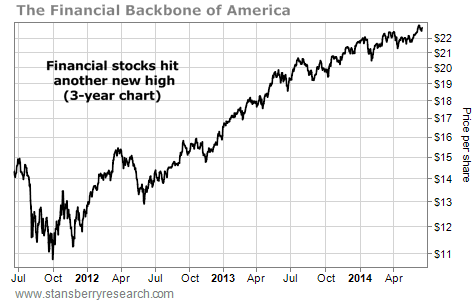

Market NotesAMERICA'S FINANCIAL BACKBONE IS STILL GETTING STRONGER The uptrend in America's financial backbone is still in place. And that's good for America.

Regular DailyWealth readers know we monitor the U.S. financial stock fund (XLF) to gauge the action in the banking sector. With large weightings in JPMorgan, Bank of America, Goldman Sachs, and Citigroup, XLF represents America's financial backbone. It rises and falls according to America's ability to earn money, save money, service debts, start businesses, and generally just "get along."

After suffering a selloff in 2011, XLF rallied in 2012 and 2013. As you can see from the chart below, this rally is still going.

In just the past month, XLF has rallied above $22.50 per share. This represents its highest level in five years. It's still a bull market in America's financial backbone.

|

Recent Articles

|