Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

These Inflation Numbers Might Shock YouBy

Wednesday, October 22, 2014

It's a terrifying thought for investors...

In its efforts to stimulate the economy, the Federal Reserve goes too far... creates too much credit... and a big inflation crushes stock and bond prices. Retirement is ruined.

Over the past five years, this worry has caused many people to miss out on terrific returns in stocks and bonds. During this time, I've reminded readers of Retirement Millionaire about the facts on inflation... and why it hasn't been a concern.

We've made huge returns as a result.

As I'll show you below, the gains aren't close to being over... and inflation still shouldn't be a concern for investors right now...

While it's a good idea to monitor the latest inflation statistics each month (like we do in my Income Intelligence newsletter), it pays to check in on a timeline of inflation stats to see where we are in the cycle.

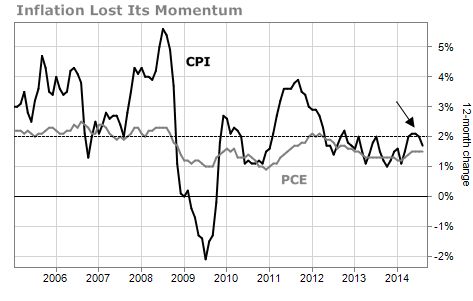

Remember, a long-term comfortable level of inflation is about 2%. But there are a few ways to measure it.

The most popular measure is the core Consumer Price Index (CPI), which excludes energy and food prices. That's important, since the prices of those commodities are so volatile right now that including them can cause some wild readings. The CPI rose above 2% for a touch in 2011, then fell again. For the past year, it looked like it was rising, but recently lost its momentum.

The Personal Consumption Expenditure Index (PCE) is the Fed's preferred measure of inflation and it does a better job of tracking an actual consumer's exposure to prices. That's signaling an even lower level of inflation. It, too, was starting to rise earlier this year, before leveling off in recent months. Take a look:

As you can see, inflation is no concern right now. That means we'll continue to see very favorable credit conditions. Businesses will be able to borrow cheap money. Consumers won't be rocked by high interest rates. That's why I'm still urging my readers to take advantage of extraordinary deals in municipal bonds... and I'm still urging readers to own dividend-paying blue-chip stocks like Chevron (CVX) and Medtronic (MDT).

The boogeyman of inflation is nowhere to be seen... so don't get scared out of solid investments.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Doc knows investors are also worried about rising interest rates. But "don't fall for the hype," he says. "Rising rates won't stall the stock market." Find out why right here.

Interest rates are complex and unpredictable. "That's why the best approach is to build a diversified portfolio that's prepared for any interest-rate environment," Doc writes. Learn how here: My No. 1 Way to Reduce Interest-Rate Risk.

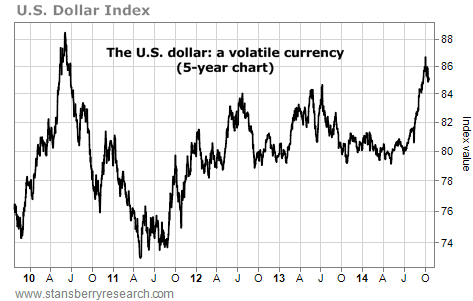

Market NotesYOUR BANK ACCOUNT IS MORE VOLATILE THAN YOU THINK Today's note is a reminder... the value of your bank account fluctuates a lot more than you realize.

Currencies like the U.S. dollar, Europe's euro, and Japan's yen trade on big financial exchanges just like stocks and commodities do. Most folks don't realize just how volatile currencies can be... and how their global purchasing power is affected.

The chart below displays this volatility. It's a five-year chart of the U.S. dollar index. This index measures the dollar's value against a basket of foreign currencies, like the Japanese yen and the euro. It's the generally agreed-upon measure of the dollar's global trade value. It displays the value of our bank accounts.

You can see how the U.S. dollar is bouncing up and down with tremendous volatility. Double-digit percentage changes in value (12%... 15%... 20%) are taking place in the span of months... not years. Think holding U.S. dollars in a bank account is a boring, conservative idea? Think again!

|

Recent Articles

|