Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's Note: Regular readers may recognize today's essay from last Friday's S&A Digest. It covers such an important concept that we wanted to make sure all of our readers had a chance to read it. This idea comes from Stansberry Research Editor in Chief Brian Hunt... and it's one of the most important steps you can take to protect your wealth today. Read on to learn...

The Easiest Way to Protect Yourself From the Next Financial DisasterBy

Friday, October 24, 2014

You wake up in the morning, turn on the news, and get a sick feeling in your stomach...

The stock market is crashing again. Another big Wall Street bank has failed. Your 401(k) has lost another 25%. It's bleeding value every week.

Your dream of early retirement is history. You've lost so much money in stocks that even a "regular" retirement is in jeopardy. If you live a long life, there's no way you'll have enough money.

This is the financial disaster scenario that terrifies a lot of investors. It's what kept people up at night during the 2008 credit crisis.

Could it happen again? Could another crisis cause the value of the U.S. dollar to collapse? Could the stock market suffer another epic decline?

Many people say the answer to these questions is "yes."

Fortunately, I don't need to know the answer to these questions... and neither do you.

The good news is that it's very easy to buy insurance against financial disasters like these. I personally own this insurance. Many of the smartest, wealthiest people I know own it, too. It could mean the difference between a comfortable, early retirement... and just barely getting by.

First, it's important to agree on what "insurance" is. In my book, buying insurance comes down to spending a little bit of money to hedge yourself against a disaster.

Throughout our lives, we spend a little bit of money on insurance and hope we never have to use it. For example, home insurance costs a small fraction of your home's value. Buy it and hope you never have to use it. Same goes for car insurance. It costs a fraction of your car's value, so you buy it and hope you never have to use it.

It's the same with investment insurance. You can buy "investment insurance" and hope to never have to use it.

There are hundreds of wealth and investment insurance policies out there. They involve intricate details, lots of forms to sign, and payment of big fees to advisors and salesmen (which are often the same thing).

I'd rather keep things simple and keep money in my pocket instead of a salesman's pocket. Here's how you can do it...

Put a small portion of your wealth in gold bullion.

That's it.

That's all it takes to insure yourself against a financial disaster.

No complicated insurance products. No big fees to pay. Just pay a small commission to a gold seller, store the gold in a safe place, and you're done.

Here's why this "insurance" is important...

Some popular market gurus are predicting a global depression, a collapse in the dollar, and a huge increase in the price of gold. The chances of them being right are relatively slim. People have been predicting the "next depression" for 30 years. The world just has a way of not ending.

However, the "doom and gloom" gurus bring up some good points. They aren't crazy. There are some big risks to our financial system. The U.S. government is spending way too much money on wars, Obamacare, welfare, and other programs. Europe and China's economies could decline and trigger a global recession. These are all real risks to your retirement account.

I'm no doom-and-gloomer. I think the economy will deal with these risks and keep growing. Again, the world just has a way of not ending like so many people believe it will. That's why I want to own stocks, bonds, and real estate. These assets will do well if the crap doesn't hit the fan.

However, I also want insurance in case I'm wrong and the potential disaster that some are predicting takes place. People would likely flock to gold in a global financial disaster... and cause its price to soar.

That's why it makes sense to buy gold as a form of insurance.

The good news is that you don't have to buy a huge amount of gold to have a good insurance policy. You can place just 5% of your portfolio into gold.

Let's say you have a $100,000 portfolio with 95% of it in blue-chip stocks and income-paying bonds. You place the remaining 5% of your portfolio into gold. This gives you $95,000 in stocks and bonds and $5,000 in gold.

If the predicted financial disaster doesn't strike, your stocks and bonds will increase in value. Your gold will probably hold steady in price or decline a little. Since the bulk of your portfolio is in stocks and bonds, you'll do just fine.

But what if the financial disaster strikes? I've heard some top financial analysts say gold could climb to $7,000 an ounce in the financial-disaster scenario.

Let's say a financial disaster sends the value of your stocks and bonds down 50%. That would be a massive decline. Throughout history, only the worst, most severe bear markets sent stocks down this much.

This epic financial disaster would cut your $95,000 stock and bond position by 50%, leaving you with $47,500. But let's say this disaster also causes gold to rise to $7,000 an ounce. Right now, gold is $1,230 per ounce. A rise to $7,000 would produce a more-than-fivefold increase in the value of your gold. It would cause the value of your $5,000 gold stake to rise to about $28,455.

Post-financial disaster, you're left with $75,955 ($47,500 from stocks and bonds + $28,455 from gold). The disaster still hits you, but not nearly as hard. Your insurance played a big role in limiting the damage.

But what if you think the chances of financial disaster are higher than "unlikely"? What if you're more worried than the average Joe?

If you are, simply increase the "insurance" portion of your portfolio. Instead of a 5% position in gold, you could increase it to 20%.

If the previously mentioned financial disaster were to strike your $100,000 portfolio weighted 80% in stocks/bonds and 20% in gold, the math works out like this:

The 50% decline in your $80,000 stocks/bond position leaves you with $40,000. Gold's increase to $7,000 an ounce makes your $20,000 gold position increase to $113,821.

Your large gold insurance position actually produces a net gain in this scenario. You're left with $153,821... an increase of more than 50%.

As you can see, the larger your gold-insurance policy, the better you do in the financial-disaster scenario. But if the financial disaster doesn't strike, you won't benefit as much because you hold less money in stocks and bonds, which do well if the economy carries on. And keep in mind... it would take a serious financial disaster to send stocks down by 50% and gold to $7,000.

Depending on what you think the chances of financial disaster are, you can adjust your gold-insurance policy. It all depends on your goals and beliefs.

Think the chances of disaster are slim? Consider a gold-insurance policy equivalent to 1%-5% of your portfolio. Think the chances of disaster are high? Consider a gold-insurance policy equivalent to 20% of your portfolio.

Are the "gloom and doom" gurus right? Is financial disaster around the corner? I don't know the answer. Nobody does. But if you buy some "investment insurance" in the form of gold, you don't need to know the answer. It's simple. It's easy. It's low-cost.

You buy gold and hope to never have to use it. You'll do fine if things carry on. You'll do fine if the crap hits the fan.

And the peace of mind you get from owning gold "insurance" is worth even more than the money it could save you.

Regards,

Brian Hunt

Further Reading:

If paper currencies like the U.S. dollar collapse, gold will still hold value. That's why Doug Casey, one of the world's top experts on gold and resource investing, views gold as "cash in its most basic form." Read our full interview with Doug to learn why you should hold gold.

Dan Ferris says you should always own gold… "Gold is the asset that can't be inflated, yields nothing, and is no one's liability," he writes. "It's real wealth… pure wealth… the most enduring form of wealth in history." Get all the details here.

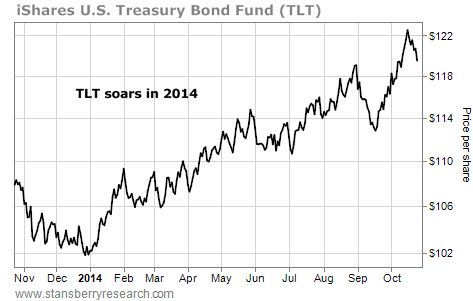

Market NotesIT PAYS TO BE CONTRARIAN Almost nobody expected it... but one of the best-performing assets this year has been U.S. Treasury bonds.

As you'll remember, there was no "surer" bet in all of finance: Interest rates had to go up in 2014. And since interest rates and bond prices have an inverse relationship (when rates go up, bond prices go down – and vice versa), that meant bond prices were "sure" to slump in 2014.

But as regular readers know, when the crowd all agrees on something, it's likely that the opposite will happen. And that's exactly what we've seen with U.S. Treasurys this year. As Brett Eversole pointed out last October in Growth Stock Wire, sentiment on U.S. Treasurys had reached a negative extreme – a bullish sign for Treasurys. As Brett explained, it was a great time to place a contrarian bet.

You can see how this idea has played out in the chart below. It shows the price action for the iShares U.S. Treasury Bond Fund (TLT). TLT is the easiest way to gain exposure to long-term U.S. Treasurys. And as you can see, Brett's call was spot on... interest rates have fallen and TLT shares have soared close to 20% since the start of the year. It's one more example of why it pays to go against the crowd.

|

Recent Articles

|