Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Your Financial Security Depends on This QuestionBy

Friday, January 23, 2015

It's possibly the most important question in personal finance...

"How much cash should I hold?"

By cash, we don't mean actual dollar bills stacked up in your sock drawer. We mean money you can access quickly, with no loss of capital and little transaction fees.

This includes checking accounts, savings accounts, and a few short-term investment accounts. Basically, cash is the money you can use to pay for things with no worry or hassle.

With that in mind, when we talk about how much cash you need to hold, we're really talking about two different things...

These are:

Your emergency cash fund is there to provide a safety cushion in the event of unforeseen emergencies, especially the loss of your source of income. In many ways, this is a personal question. It depends on how safe you want to be. You can find experts saying that you should have between three and 36 months of living expenses in your emergency fund. I'd narrow that range to between six and 12 months.

To measure where you fall in that range, think about the risks that affect your life...

If your job is in a cyclical industry, you need more savings than someone whose job is recession-proof. If you only have one income-earner in the family, you need more than if you have two. If you have a large mortgage payment, you should keep more on hand than if you rent an apartment, since missing mortgage payments is more painful than skipping out on rent.

It also depends on how nervous a person you are. You should keep enough to sleep well at night. That's the central tenet to all of my investment advice.

Another thing to remember, six to 12 months of expenses is a lot of money for nearly anyone. For those just starting to save, it seems like an insurmountable number. Don't be discouraged. Three months of expenses saved is better than two months. And two months is better than no months.

A small cushion is better than none at all.

After you've got your cushion, you have to look at the longer-term cash allocation in your portfolio.

For a young person with 30 years to retirement, there is little reason to have any cash holdings in your portfolio, after you set aside your emergency fund.

As you get closer to retirement, you should start moving some of your investments over to cash. You should start this phase five or 10 years before retirement. And you could gradually grow your cash allocation from, say, 5% to as high as 20%, depending on your goals.

Keep in mind, over a 30-year sample, cash provided a lower return than stocks 73% of the time. If you've got a long time and want to generate returns, cash is a drag on your portfolio returns.

However, cash is king in times of volatility... outperforming stocks 27% of the time, typically when stocks are down big. When you are most concerned with safety and liquidity, cash is exactly what you need.

Most people don't spend too much time thinking about their cash.

In the case of deciding how much to hold, that's to your detriment. Because of our emotions, people tend to skew either too cautious – and hold too much cash – or too aggressive – and hold too little.

Sitting down and taking a rational look at your cash needs can provide for emergencies and immediate needs without sacrificing long-term returns.

Here's the good thing about getting your cash investments in order: Once you do, it takes little time to keep things in order.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig Jr.

Further Reading:

Allocating your assets wisely builds safe, long-term, "sleep at night" wealth. "If you haven't looked at your asset mix recently," Amber Lee Mason warns, "do it this week. It could save you from catastrophe down the road." Learn more here.

"Right now is likely the best, safest time in the history of the world..." Doc writes. Earlier this week, he showed readers the proof... And why you shouldn't let misplaced fear keep you from taking advantage of great investment opportunities. Find his must-read essay here.

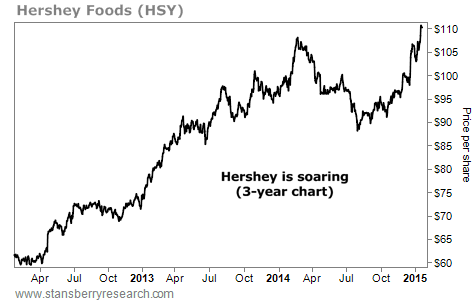

Market NotesONE OF OUR FAVORITE BUSINESSES IS SOARING Last week, we discussed the concept of capital efficiency... Today's chart is a perfect example of this idea in action.

Over the years, Porter Stansberry has written many times about investing in capital-efficient businesses (a few examples are here, here, and here). These companies generate high returns on capital with little additional ongoing investment. They enjoy strong customer loyalty. They can gradually raise prices when they need to. This translates into more money returned to shareholders.

Porter's favorite example of this idea is Hershey Foods (HSY). When people think about chocolate bars, they think "Hershey's." It's a simple, cash-gushing business that most anyone can understand (most capital-efficient companies are).

As you can see below, capital efficiency is working well for Hershey's shareholders. Shares have nearly doubled over the past three years... and just soared to a new all-time high.

|

Recent Articles

|