Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Five Reasons Why This World Dominator Is Still a 'Buy' TodayBy

Wednesday, November 12, 2014

I recently received an interesting note from one of our customer service representatives...

What should a customer do with IBM? IBM is dropping... so should he still buy? Have you taken the drop into account? What do you recommend as the next action? The customer feels like you have been misleading with reports... Have you taken this into account? – Regarding paid-up subscriber B.H.

I've heard similar (and similarly vague) complaints many times over the years.

At various times in the last nine to 10 years, people have loved to hate "World Dominators" like Wal-Mart, Microsoft, Intel, Cisco, Johnson & Johnson, Procter & Gamble, and Apple... It must be impossible for a business to become large and successful without attracting mountains of criticism.

And so it is with IBM today...

People who try to explain small drops in company share prices are wasting their time. They're either TV talking heads – who are paid to look good and read clearly from a teleprompter – or they're individual and professional investors who aren't focused on the numbers that tell you if a company is doing well or poorly.

IBM's share price is down roughly 11% since we recommended it two years ago (including dividends) in August 2012. An 11% drop isn't much to worry about. All the factors that made IBM a great business in 2012 still hold true today...

IBM is the biggest provider of IT services in the world. It's the second-largest software company in the world (after Microsoft). In 2011, IBM was awarded more U.S. patents than any company in the world for the 19th year in a row. Since 2000, it has generated more than 47,000 patents.

Those are facts. I don't know how much clearer or less misleading I can possibly be.

In the initial recommendation, I also discussed the five financial clues that identified IBM as an excellent business...

Despite the clamor of disgruntled ex-employees, short sellers, political writers, and the financial press... all five of those important financial clues are still intact. My research partner, the intrepid Mike Barrett, recently did some more work that sheds a flattering light on IBM's use of two of those clues: free cash flow and share repurchases.

IBM is the most efficient share repurchaser we've studied yet. It has, on average, spent just 3% of its annual free cash flow on each 1% reduction in its share count since 2008. The company's total share-count reduction from December 31, 2008 to today is an incredible 21%.

The company has continued to raise its dividend annually, at about 14% per year. If IBM keeps that up, you'll make about 16% per year holding shares. Since our recommendation, it has continued to generate high returns on equity... higher than most of the companies in existence today.

We don't sell based on share-price movements like this...

We sell based on our return expectations from current prices, among other variables. If we think a stock that's down will generate good returns going forward, we'll continue recommending it. Likewise for a stock that's up.

Whether a stock is up or down is far less important to us than if we believe it'll generate good returns from current prices.

IBM should generate good returns from current prices, so our advice hasn't changed.

Good investing,

Dan Ferris

Further Reading:

Find more of Dan's latest advice for investors here:

How to Make a Fortune in Resource Stocks... Starting Today

"Today, resource stocks are some of the best bargains in the world..." Why I'm Recommending "Value Destroyers" Today

These will be some of the best-performing stocks of the next three years... The 'World Dominator' Triumph: More Return Without More Risk

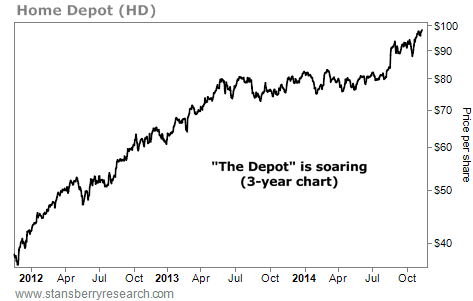

"Owning these businesses allows you to do something you're not supposed to be able to do..." Market NotesAN UPDATE ON ONE OF OUR FAVORITE "REAL-WORLD" INDICATORS Shares of Home Depot continue to soar... and that's good news for America.

Over the past three years, we've run dozens of charts that prove "things can't be all that bad" in the U.S. economy. We've featured charts of "real-world" indicators like soaring transportation stocks, soaring hotel stocks, and soaring financial stocks. The price action in shares of Home Depot is another great example...

"The Depot" is America's largest home-improvement chain. It sells the things we need to remodel kitchens, build backyard patios, and make home additions. This makes Home Depot's share price an excellent gauge of what's happening in America.

As you can see from the chart below, shares are up more than 150% over the past three years. And since our last note on "The Depot" in late August, shares are up another 6.5%... setting a new all-time high this week. It's yet another sign "things can't be all that bad" in America.

|

Recent Articles

|