Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Five Simple Ways to Increase Your Wealth in 2015By

Wednesday, February 25, 2015

If you don't do this, you will likely never, ever be wealthy.

You will work until your health collapses, and be dependent on the whims of Washington bureaucrats. Quite possibly, you'll die broke.

It's a disturbing fate... but many Americans will experience it firsthand.

So for a moment, forget about valuing stocks, picking the fund with the lowest fees, or finding the ideal asset allocation.

All those are important. But your retirement... and wealth that you accumulate across your lifetime... depends almost entirely on just one factor: your savings rate.

Below, I'll share five easy ways to help you start saving more. But first, let me share some shocking statistics…

A recent survey from Bankrate, the online aggregator of banking industry news and information, found that a third of American adults haven't saved for retirement. More than a quarter of people between 50 and 64 years old have no retirement savings. And 36% of Americans have less than $1,000 in savings.

Now you may be one of these folks or you might not... either way, I want to make sure you're aware of your own situation. That's because the U.S. nanny state won't be there to protect you. And if you're wealthy, the U.S. government is going to try and take it away from you.

Most Americans say they'll depend on the government to provide in their old age... Of course, here's what the Social Security Administration had to say in its 2014 Annual Report:

It means these government promises will not stay around forever. That means... The only person left is you.

You must take personal control of your wealth... and you can start today.

Remember, saving is just spending a little less than you take in. Start small at first. But if you can save a higher-than-average amount... say, 20%, 30%, even 50%... I guarantee you will be wealthy in a modest number of years.

Let me repeat this... I guarantee it.

The best part is that it doesn't really matter how much you make. It only matters how much you save. That's the part most people don't appreciate.

Assuming modest, after-inflation investment returns of 5%... The average American has to work for more than 65 years with a 5% savings rate before accumulating enough wealth to replace their income without touching the principal. And saving 10% of your income, you should expect to work for more than 50 years before accumulating enough wealth to never have to work again.

But if you can bump that savings rate up...

Take a look at the table below:

If you can save 20%, you will be wealthy enough to retire in less than 40 years of work. If you save 30%, you can retire in less than 30 years. And at 50%, you can stop in less than 20 years. The numbers are shocking, but clear.

No matter how skilled you are as an investor, upping your savings rate is more powerful to your wealth than either increasing your income or increasing your investment returns. That's because it's a one-two punch... you increase what you have to invest, while decreasing what you spend. You also learn how to live longer on less money.

Think of savings as a gift from your present self to your future self. Think of savings as "paying in once, getting paid out forever."

Here are five simple tricks to get you started saving more...

Set up direct deposit for your paychecks. A recent study shows that those who have a portion of their earnings directly deposited into a savings account automatically save about $450 a month, much more than usual. Try it. Start with $50, then go to $75 in a couple of months, then to $100 and so on.

Boost your 401(k) contribution. Often, your employer may match contributions that you make to your 401(k) up to a certain level. If there's one financial decision that absolutely every single person needs to make, it's this... Always contribute to your 401(k) to earn the maximum employer contribution. Skipping out on that free money is the most senseless mistake in personal finance. And if you ever receive a raise, put the extra money into your 401(k) up to the maximum amount ($17,500 in 2014, $18,000 in 2015). At my company, I make an instant 50% on the first 6% I save because the company matches. It's the best investment I make every year.

Open an IRA. It's just as easy as opening any other brokerage account. When registering, you simply select IRA as the account type. When you file your taxes at the end of the year, the forms include a line to enter any IRA contributions. It's as simple as that. And it will save you tens of thousands of dollars over just a decade or two of retirement savings.

There's also another type of IRA called a "Roth IRA." These accounts let you make after-tax contributions. Then when you withdraw the income in retirement, you don't pay any taxes on them. This account makes sense for people who believe that their tax rate is lower now than it will be when they retire. I recommend people split the difference and put half into your Roth and half into a deductible so-called Traditional IRA. We'll be sharing some other secrets about IRA strategies in 2015, like ways to insure your tax-free retirement.

Pry some cash back from the tax man. If your income is under certain limits, you can get an even greater boost to your IRA. For 2014, a married couple earning less than $60,000 earns a tax credit equal to 10% of their IRA contribution. So if a couple puts $1,000 away, they not only lower their taxable income by $1,000, they also get another $100 of hard cash back from the IRS as a tax credit.

The tax credit gets bigger for lower income levels. If you make less than $36,000, your credit is 50% of your contribution. Saving is difficult for low-income folks, but this helps. It's also a great boost to the savings of young people. This is one heck of a deal. Put $2,000 into your IRA and the government will give you $1,000 (the maximum) in cash back.

If you've got a college student or other low-earner in your family, consider helping them make a contribution.

Switch to a credit union. Credit unions often pay the best rates on savings accounts – like money-market accounts and certificates of deposit. And they keep your money away from Wall Street. Credit unions are nonprofit companies that act as local community banks. If you're tired of being abused by your big bank, move to a credit union. You can find a credit union near you with www.findacreditunion.com.

Remember that ultimately, how much you save will be the difference between a lifetime of poverty... or one of wealth.

With two 401(k)s and two IRAs, a married couple interested in saving aggressively can save $46,000 a year without paying income taxes. That's a savings of tens of thousands of dollars of money that you earned and you get to keep, and that you can spend later in life. And by investing that money, you can compound your earnings quickly. Before you know it, you'll have wealth and riches to enjoy in your retirement days.

If you have someone that you care about, please forward this letter to them immediately. Encourage them to start saving today. The math is undeniable.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig Jr.

Further Reading:

Editor in Chief Brian Hunt recently showed readers what he calls "the butterfly effect of spent money." It's a "powerful, hidden force that is released when you save money instead of spending it." Get all the details here.

Last month, Doc explained what is possibly the most important question in personal finance... How much cash should you hold? "Most people don't spend too much time thinking about their cash..." Doc writes. "That's to your detriment."

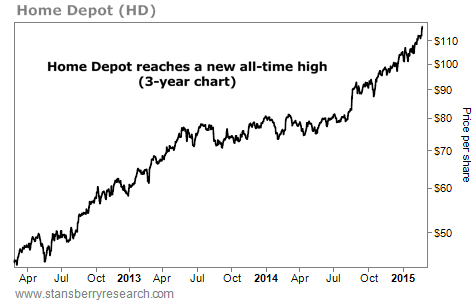

Market NotesANOTHER GOOD SIGN FOR THE U.S. ECONOMY Yesterday, "The Depot" once again showed us things are a heck of a lot better than the pessimists would have you believe.

Over the past few years, we've highlighted many charts that reveal an important idea: While the U.S. economy isn't booming, it can't be doing all that bad. For example, we've noted the tremendous share-price strength in super-bank Wells Fargo and American entertainment giant Disney.

But let's not forget about Home Depot (HD). Owning and maintaining a home is the American dream. "The Depot" is America's largest home-improvement chain. It sells the things we need to install new kitchens, remodel bathrooms, and build home additions. This makes Home Depot's share price an excellent gauge of what's happening in America.

As you can see from today's chart, things are "happening." Shares of Home Depot are up more than 150% over the past three years. And just yesterday, the company announced earnings that beat Wall Street estimates. Things are going so well that the company just boosted its annual dividend by 26%... and authorized an $18 billion share buyback program. If "The Depot" is doing this well, things can't be all that bad.

|

Recent Articles

|