Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The Secret to Making 10,000% in the MarketBy

Wednesday, January 6, 2016

Today, I'm going to share some highlights with you from an excellent presentation I heard at Grant's Fall Investment Conference in Manhattan.

These are essential for making 100 times your investment.

The speaker was Markel Chief Investment Officer Tom Gayner. Markel, which has an outstanding long-term record, is a corporation that is often compared to Warren Buffett's Berkshire Hathaway.

Gayner's approach is simple and much like my own. He looks for profitable businesses with good returns on capital that do not have a lot of debt... businesses that have ample opportunities to reinvest profits and earn high returns again and again. He wants to acquire the stocks at favorable prices. And he wants an honest and talented management team.

The most important of these is the ability to reinvest at high returns. Gayner called it the "most nuanced aspect of investing." He said: "A fair price might be a lot more than you think it is if profitable reinvestment can really take place."

He had three striking examples. All of them prove that a fair price for an investment might be a lot more than most people think...

The Mistake in New England: The first is Berkshire Hathaway. In 1965, when Buffett took control, it was a struggling New England textile manufacturer. The share price was $19. It was a high-cost producer in a commodity business. Nothing indicated that buying it would be a good move. Buffett himself called it a mistake.

"The only thing that made it better is that he realized his error and set about investing whatever funds Berkshire produced into more economically productive assets," Gayner said. "He did that relentlessly and continuously."

So while $19 was not justified at the time, Berkshire became an astounding investment. Shares today go for around$200,000. "Even if you paid 10 times as much [as $19]," Gayner pointed out, "you would still have had something special."

The point is that people spend most of their time thinking about what something is worth right now and over short time frames. They ask things like: Can it trade for more over the next 12 months? What's the Fed going to do with interest rates? What about the refugee crisis in Europe? What's going to happen with U.S. budget issues? Who's going to be the next president? What about China? And so on and so on...

"All of those are important questions," Gayner admitted, "but they are all fundamentally unknowable."

He continued: "What is somewhat knowable, or at least worth working on, is the task of finding a manager who can successfully produce earnings growth and reinvest those earnings properly over long periods of time. The example of Berkshire shows there is no more important task."

He related a good anecdote from the financial writer John Train. (Read his books!) Assume you had been on the committee of the Sistine Chapel and had the task of getting the ceiling painted. You wouldn't focus on the training of various painters, what kinds of paints to use, how many people you should hire, etc. "Instead, you go out into the world and look for a Michelangelo," Gayner said.

"We spend all of our time trying to find the Michelangelos of today," he said. "Sometimes they are specific individuals. Sometimes they are teams or systems that produce great results over time."

Markel's portfolio represents "a congealed pudding of our vision of companies and leaders that fit this ideal." The portfolio includes companies like Berkshire-Hathaway, Walgreens Boots Alliance, Walt Disney, Brookfield Asset Management, Marriott International, Home Depot, and Deere. "If we get just one or two ideas right, we will continue to produce outstanding results," Gayner said.

Fair prices often scare investors. What if something bad happens, they ask? Gayner continued with his second example: American Express.

The Salad Oil Scandal: The year was 1963. American Express had already been a successful business for more than a century. In 1963, though, it did something stupid. "It lent a large amount of money based on warehouse receipts of salad oil to a man named Tino De Angelis," Gayner said.

De Angelis was 47 years old at the time. And he was already a shady character with a documented history. American Express should have suspected something. But the company did not. Turns out, the receipts were bogus. When his scheme collapsed, AMEX collapsed, too.

Buffett bought 5% of the stock, about $20 million. It would become one of the building blocks of his great subsequent track record. "Bold, daring, and brilliant," Gayner said of the move.

But what if you bought AMEX the day before the scandal came to light? You would've thought you were a dummy. But your investment returns over time would've been close to Buffett's. So close, "it's not worth arguing about," Gayner said. "You would've compounded your capital at high-double-digit rates."

Time is the key. The mind-blowing 100 times returns often come after 10 or 20 years. Looking at his own portfolio over the years, Gayner says the one-year return for any one of his holdings was random at best. In one year, any particular stock could be way ahead or way behind the market. "I have no way of knowing which one will do what," he said.

As time goes by, however, the underlying returns earned by the businesses themselves start to dominate. "As [Charlie] Munger says, investors are doomed to earn the same returns in their shares that their businesses earn on their equity over time."

This brings us to his final example.

The Nifty Fifty: The Nifty Fifty was a group of large-cap stocks that dominated the market of the 1960s and early 1970s. They were popular. They were also expensive, trading for price-earnings ratios more than double the market's average. McDonald's went for 86 times earnings; Disney, 82; Polaroid, 91. These stocks collapsed in the ensuing bear market and sunk to gut-wrenching lows by 1982.

"It's trotted out as a cautionary tale," Gayner said, "about the danger of growth stocks and being price insensitive. But a closer look reveals those lessons are not so cut and dried."

A $50 investment in the S&P 500 in 1972 would've grown to just more than $2,900 by the end of 2014. How did the Nifty Fifty do? There is no definitive listing, but Wal-Mart is included in almost every one.

In 1972, Wal-Mart had 50 stores in five states, sales of $78 million, and net income of $3 million. Today, it has 11,000 stores in 27 countries, sales of $480 billion, and $16 billion in net income.

In the early 1970s, Wal-Mart's return on capital was in the low 20% range. Today, it's in the teens. One dollar invested in Wal-Mart in 1972 would've grown to just more than $1,800. While that's not enough to top the market, you had 49 other stocks to go.

"They did not all go to zero," Gayner said. You would have had $1 in Philip Morris (now Altria) and $1 in Anheuser-Busch. "Your $3 handily outperforms the market by double digits," Gayner said, "even without including any of the returns from the remaining 47 stocks."

These 47 did include some giant losers, such as Polaroid and Kodak. But you also would have had Disney, Johnson & Johnson, and Procter & Gamble.

So Gayner finished where he began: Why is this investing stuff so hard to do? It's hard because we don't give our investments time. And we need to recognize something else: "You only need to get one right." This is something I like to repeat as well. It's true.

The greatest investors are often great investors because of one, two, or three really great moves. And even if your timing seems awful at first – as with Berkshire in 1965, American Express in 1963, and the Nifty Fifty in 1972 – time and patience will do the work for you to succeed.

In the quest to make 100 times your money, these lessons from Gayner are indispensable.

Regards,

Chris Mayer

Further Reading:

Find more of Chris' insights in DailyWealth right here:

If you have a high conviction on the gold price, these royalty stocks belong in your portfolio...

As bad a run as oil stocks have had, it could get worse...

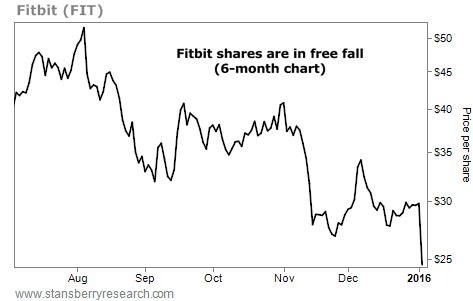

Market NotesA LESSON IN BUYING WHAT'S HOT Today, an important reminder on the dangers of owning newly listed companies (or "IPOs")...

2015 was a terrible year for IPOs. According to an article in Bloomberg, nearly half of the companies that went public last year with a valuation in excess of $1 billion were already trading below their IPO prices. As you can see, brand-new companies may be exciting, but that does not necessarily make them good investments.

One perfect example is fitness stock Fitbit (FIT). The company makes wearable trackers that people use to monitor their daily steps and various other health goals. As you can see from the chart below, the market fell in love with this new technology... but now the fad is cooling off in a big way.

After soaring 60%-plus from its first day of trading in mid-June to August, share prices have fallen fast. The stock has plummeted more than 50% in the past five months alone and just hit a new low. If you want consistent profits, turn to the "boring," proven companies instead...

|

Recent Articles

|