Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Steve's note: Peter Churchouse is one of my investing "heroes"... He's one of the true pioneers of emerging-markets investing. For the last 30-plus years, he's been based in Hong Kong, pursuing investment opportunities in Asia. Today, Peter writes The Asia Hard Assets Report (www.AsiaHardAssets.com). In my opinion, nobody is more knowledgeable about Hong Kong and China investments than Peter. The Monaco of China: 100% Upside If Left UncheckedBy

Friday, October 19, 2012

Back in the days leading up to the handover of Hong Kong to China in June 1997, I said Hong Kong could become "The Monaco of China."

That has happened...

The city is now a target for wealthy property buyers from the big elephant market to its north, China. Hong Kong's low tax base, ease of doing business, open capital system, and free-and-easy lifestyle has attracted people and money from China to Hong Kong.

Thanks to the "Monaco of China" effect, people from mainland China are now buying about 30% of the properties in Hong Kong above US$1.5 million in price. Locals here in Hong Kong are now rightfully worried that the Chinese are pushing prices up.

There is more to come. Courtesy of Mr. Bernanke in the U.S. (and Mr. Draghi in Europe), Hong Kong asset prices are likely to continue to face upward pressure for years to come.

Left to its own devices, it is entirely possible that Hong Kong residential prices could rise 100% from here over the course of the next three years.

We have a number of reasons why this could happen now...

The thought of a 100% rise in Hong Kong residential prices over the next three years might sound outrageous at first. But it has happened before...

In the two years from late 1995 to late 1997, prices rose by around 100%. However, the Asian Crisis and years of deflation since the beginning of this century have meant that prices in real terms now are about the same as 1997.

There have been other episodes of very sharp escalation of property prices in Hong Kong. For example, in the three years leading up to the end of 1980, residential prices moved up by between 100% and 120% PER ANNUM. Now that is a bubble!

The key caveat here in this 100% upside idea is the phrase, "left to its own devices."

You see, the Hong Kong property market is unlikely to be left to its own devices...

The Hong Kong government and its central bank worry about property bubble conditions emerging. Evasive action has been and is continuing to be taken. Further policy measures could well be introduced if prices continue the pace of growth seen in recent months.

Still, the balance of risk for residential property prices is more to the upside than the downside.

So how should you trade this?

The shares of the major property developers in Hong Kong should be big beneficiaries from the conditions we see prevailing in the Hong Kong property markets over the coming couple of years.

Property developers have the potential for decent earnings increases, from both increases in construction as well as potentially rising prices. The main overhang for these stocks is the risk of further policy actions aimed at curbing demand and price pressures.

The Hong Kong housing market is dominated by approximately six major developers who routinely produce at least 70% of the city's new private housing. Current easy money policies will play very well to rising earnings prospects in the coming three to four years for these major developers.

This list includes Sun Hung Kai Properties (0016:HK), Cheung Kong (0001:HK), Henderson Land (0012:HK), Sino Land (0083:HK), and New World Development (0017:HK).

These stocks are all trading at deep 30%-50% discounts to underlying net asset values with average 2012 price-to-earnings ratio of around 15 times. They also pay very respectable dividends with an average expected yield of a little over 3% for the current year.

These are the big blue chips, and they are attractive today for investors who can easily trade Hong Kong shares.

For U.S. individual investors, the simplest, most-liquid way to buy a basket of the major Hong Kong blue chips (that includes these names) is to buy the iShares MSCI Hong Kong Index Fund (NYSE: EWH).

With a pile of positive indicators that should remain in place for years, combined with reasonable valuations, Hong Kong property developers are a buy in my book.

Sincerely,

Peter Churchouse

Founder, Asia Hard Assets Report

For more on Peter's Asia Hard Assets Report, visit www.AsiaHardAssets.com.

Further Reading:

In March, Brett Eversole introduced DailyWealth readers to a simple system for trading Hong Kong stocks. Over the past 40 years, this system has triggered six trades... returning an average of 234% in less than three years. Get the full details here: This Easy Rule Almost Guarantees Triple-Digit Returns.

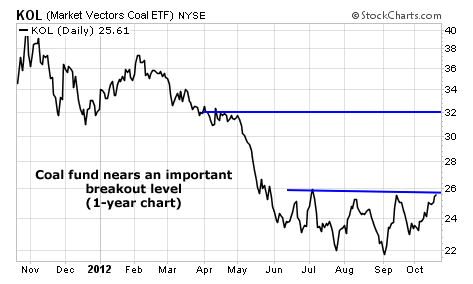

Market NotesA NEW TREND FOR COAL STOCKS Coal stocks have been miserable performers this year.

The price of coal has fallen nearly 30% since last October. Low prices are cutting into the profit margins of many coal producers. Most of these companies are loaded with debt. And they're bleeding red ink...

That's why investors hate coal stocks these days. KOL, a fund that holds a basket of coal producers and related stocks, dropped more than 50% from July 2011 to July 2012. But the sector may be ready to turn higher...

Ever since Mitt Romney mentioned coal companies favorably during the first presidential debate, coal stocks have been trending higher. And as today's chart shows, KOL is now approaching an important resistance level. If it manages to break out to the upside, there's a lot of room for coal stocks to run.

– Jeff Clark

|

In The Daily Crux

Recent Articles

|