Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today's issue is unusual. Rather than our typical essay format, today's issue comes in the form of an interview. It's with our friend Rick Rule. Rick is one of the best investors on the planet, and he has a legendary eye for value. When he tells us he is interested in buying an asset, we take notice. He recently told The Daily Crux about a big opportunity he sees right now... The Most Dramatic Speculative Opportunity in Energy TodayBy

Tuesday, November 6, 2012

The Daily Crux: When we last spoke, you mentioned you were bullish on several areas of the resource market. One that you're especially bullish on today is uranium. Can you explain why that is?

Rick Rule: Well, the "big picture" reasons to be bullish on uranium – and energy more generally – are probably quite familiar to most of your readers.

There are 3.5 billion people in the world who are becoming gradually more free... and as a consequence, are becoming rapidly more wealthy. These people aspire to the same lifestyle you and I enjoy. And that lifestyle is energy intensive.

However, I'm particularly bullish on uranium, as it is my belief that the uranium market is irrationally depressed – depressed, of course, as a continuing consequence of the Fukushima disaster.

Crux: Why was the Japanese nuclear disaster so bearish for prices?

Rule: When the tidal wave hit the Fukushima plant in Japan, a couple things happened.

First, the Japanese shut down their entire nuclear power industry. This took about 20 million pounds of annual uranium demand off the market.

But what most people don't realize is it also brought 15 million pounds of surplus inventory onto the market. The Japanese reactors weren't going to burn uranium for any foreseeable time frame, and they had to sell it to generate revenues because they weren't getting revenues from electric generation.

So 20 million pounds of demand evaporated, and 15 million pounds of supply was dumped on the market in a very, very short period of time.

In addition, the Japanese, as well as the Germans, have since issued policy statements which suggest that nuclear is not going to be part of their power mix on a going-forward basis... which only served to further depress the price.

Crux: Under these circumstances, what upside catalysts do you see?

Rule: Frankly, we believe those policy statements are disingenuous.

We don't believe the Japanese have the ability to sustain their current economy without nuclear power. Their power-generation costs are up threefold as a consequence of burning liquefied natural gas. This, of course, has had a wonderful impact on the liquefied natural gas markets, but is a serious problem for Japan.

The Japanese have a stated goal of energy security, and the most secure form of energy available in the world today is uranium because of its energy density.

The Japanese can – and I think ultimately will – purchase enough physical uranium to have three or four or five years of energy security and avoid the geopolitical contests that have become so prevalent in the oil market.

It is interesting to note that the Japanese government – through JOGMEC, which is its international exploration arm – recently announced a strategic new venture with the government of Uzbekistan to explore for uranium for export to Japan.

The fact that they're spending a bunch of money on grassroots exploration flies in the face of their stated goal of eliminating nuclear energy.

The German question is also of interest. The Germans have stated that they have a similar policy goal with regards to eliminating nuclear power from their mix.

What they're doing – because they're in a somewhat better financial condition – is rather than generating electricity on German soil, they plan to phase out the German reactors and import more electricity from places like Holland or France.

The interesting thing about that is most of the electricity they will be able to import is in fact nuclear energy – energy generated from uranium.

So even if Germany dramatically reduces its nuclear power production – and hence uranium consumption – that demand will not disappear, but rather only move to a different location.

So we believe the demand fears are greatly exaggerated. But we also believe supply could become a problem as well.

Our data – found through the course of our analyses on individual uranium producers – suggest the industry requires a price of about $85 per pound of uranium in order to bring new mines into production. Currently, uranium is trading for under $50 per pound.

So for the uranium industry to continue supplying power around the world, the uranium price has to go up.

And the uranium price can go up because the price of uranium is as little as 3% of the total cost of delivering electricity from a nuclear power plant. Even if the uranium price were to double, it would make an almost imperceptible difference in the final cost of producing electricity from a nuclear power plant.

So we see a situation where the spot price is under $50 and the term price – the prices paid in the long-term market between uranium producers and uranium consumers – is about $65 or $70. So the spot price is $20 depressed of the term price... and more importantly, even the term price has to go up for current uranium demand to be supplied on an ongoing basis.

Finally, investors need to understand that for the past 10 years, the uranium price has been moderated as a consequence of a program where Russian and American weapons-grade uranium stock has been blended down to fuel grade stock for use in power plants. That supply is rapidly running out.

Mercifully, we have taken away a whole bunch of latent warheads, and it's done a wonderful thing to moderate energy prices for 10 years. But that party's largely over.

So we see a situation with greatly constrained supply on a going-forward basis, coinciding with rapidly increasing demand in places like Taiwan, Korea, and China.

When those supply and demand lines intersect, the only thing that can happen is prices go up. If the prices don't go up, the lights will go out. Even in anti-nuclear markets like the United States, 19% of the total electrical mix comes from uranium.

Will natural gas help? Certainly. Will solar help? Will geothermal help? Will wind help? Absolutely. But is there any way to substitute for uranium in today's energy mix? Absolutely not.

Crux: That's quite a case for higher prices. Are there any serious risks to this forecast?

Rule: As you know, there are risks with any investment thesis, and this is no exception.

The principal risk is another serious accident. Another accident of the magnitude of the Fukushima or Chernobyl disasters would certainly delay a recovery in the uranium price.

The countries that are building nuclear plants now – primarily Taiwan, Korea, and China – are well enough financed that we don't see financing risk in terms of building out additional nuclear capacity.

We only see political risk, and political risk would manifest itself in the event of another catastrophic failure of a power system.

Crux: Any parting thoughts?

Rule: While we believe this is an incredible opportunity, it's important to remember that these things always take longer to play out than we think they will.

I would suspect that an investor who's looking for immediate gratification – immediate, in this case, meaning one year or less – should be cautious about this. But I think investors taking a two- to four-year time frame will be richly rewarded.

Crux: Thanks again for talking with us, Rick.

Rule: My pleasure.

Editor's note: Rick and his team have extended their offer of a complimentary portfolio review for any interested readers. You can reach them at Sprott Global Resource Investments, by e-mail at [email protected], or by phone at 800-477-7853 (or 760-943-3939 outside of the U.S.).

Further Reading:

A while back, the Daily Crux team sat down with Rick to learn about one of the most powerful strategies for profiting in natural resources. Of all the ways to invest in the sector, this may be the simplest. And when used correctly, it can lead to huge, safe gains...

If you're looking to make life-changing profits from commodities and resource stocks, you can't miss this interview. It's completely free for Crux subscribers. Learn more here.

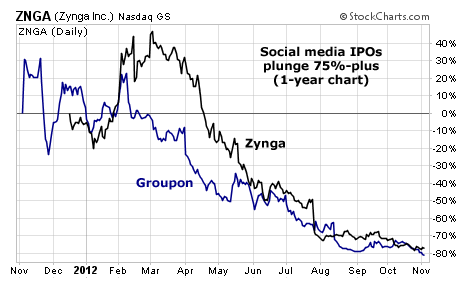

Market NotesA STUNNING COLLAPSE FOR SOCIAL MEDIA IPOS Today's chart is a reminder about the dangers of buying into the hype of initial public offerings (IPOs).

Amateur investors often mistakenly think they need to invest in risky, unproven companies to make big gains. Take social media companies, for example… Their IPOs within the last year generated massive hype. And frenzied investors – who paid ridiculous prices for shares of companies with lackluster financial results – were left "holding the bag"…

Some of the biggest IPOs included daily-deals website Groupon and online game-maker Zynga. As you can see in the chart below, both stocks are down more than 75% since their shares went public.

Today, the outlook for both companies looks much different than the rosy picture Wall Street painted for investors last year. At Groupon, high employee turnover and the departure of several key venture capital backers over the summer have weighed on the stock. Shares fell to their lowest level ever last week. Zynga also hit a fresh low after the company announced it would lay off 5% of its employees.

The lesson: It rarely pays to buy what Wall Street is hyping.

– Larsen Kusick

|

In The Daily Crux

Recent Articles

|