Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today, we're continuing our holiday series from Dr. David Eifrig... For the past three months, Doc has been looking into "common sense" solutions for Americans who are worried about privacy, security, and wealth protection. Below, you'll find one of his top recommendations for legally keeping a portion of your income away from the taxman...

One of My Favorite Ways to "Dodge" TaxesBy

Wednesday, December 26, 2012

Are you earning the market's safest, highest tax-free yields?

Or are you still buying into the hype?

For the past three years, I've been one of the few investment advisors to continually "pound the table" on municipal bonds. They've been – and will continue to be – a great deal for income-seeking investors.

As you probably know, municipal bonds are loans made to state and municipal governments. To encourage folks to invest in the government, interest received from "munis" is exempt from federal income tax and, in many cases, state and local income taxes.

This makes them a great way to earn investment income... and keep it from the taxman.

During the time I've been urging investors to own munis, there's been an enormous amount of "fear hype" surrounding them. On the December 19, 2010 broadcast of 60 Minutes, Wall Street analyst Meredith Whitney – best known for her bearish call in the fall of 2007 on Citigroup – foretold 50-100 "significant" municipal bond defaults that would add up to "hundreds of billions of dollars."

Whitney's media appearance caused a panic. About $30 billion exited the muni bond market. Some of the strongest, best bond funds fell 15% in just a few months. This is an enormous move for "boring" bonds.

The panic was way overdone. In 2011, defaults totaled just $2.6 billion. That's a hair less than the $2.8 billion defaults in 2010 and hardly the disaster industry "experts" were expecting. My Retirement Millionaire readers kept holding their muni bonds and making great tax-free money.

And then Stockton, California stoked the fear hype again. Back in June, Stockton became the largest U.S. city to declare bankruptcy. The crisis triggered the same warnings investors had heard for years.

But remember... the municipal bond market is huge... It's over $3 trillion. So while Stockton is the largest city to declare bankruptcy – with over $500 million in debt – it can't do much, if any, harm to the whole muni market.

This year, the numbers of municipal defaults will still be minuscule – perhaps 0.5%-1% of the total municipal bond market. But many of the muni bonds are priced as if they're expecting 10%-14% default rates. Remember... in 2011, defaults totaled $2.8 billion... less than 1% of the total market. Even if defaults doubled (to $5.6 billion), that is still less than 1% of the market... and a long way away from the 10%-14% the talking heads are yelling about.

Plus, when there is a default, new terms are usually quickly worked out. Sometimes investors still get new deals that provide $0.80-$0.90 on the original dollars. In short, default isn't the huge risk you're hearing about.

Many investors have sold municipal bonds in the past month. They're afraid politicians will try to tax folks on muni bond interest income. This is another overblown fear. It's not happening.

One of my favorite municipal bond picks is the Invesco Value Municipal Income Trust (NYSE: IIM). IIM invests in tax-free, fixed-income securities. It holds a diversified portfolio of mostly A-rated (or higher) municipal securities. The interest and principal payments are also covered by insurance. Owning a fund that holds insured, investment-grade paper means we can sleep well at night.

IIM's current distribution rate is 5.6%. For people in the 35% tax bracket, this works out to an incredible 8.6% taxable equivalent yield.

Bottom line... Don't let the scary headlines and gloomy predictions spook you out of a great investment and a great tax "dodge." Ignore the hype and earn safe, tax-free income.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

"In the modern age, your personal information is more valuable than exquisite jewelry," Dr. Eifrig wrote on Monday. But there "are a few easy strategies you can use to keep it safe. You should put them into practice immediately." Read more here: The Most Dangerous "Everyday" Threat to Your Privacy.

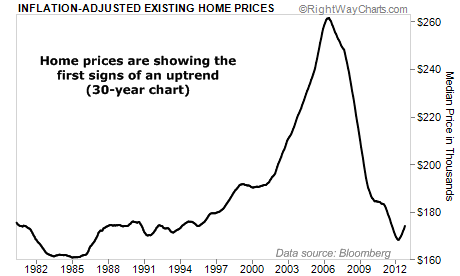

Market NotesTHE UPTREND YOU'VE BEEN WAITING FOR One of Steve Sjuggerud's favorite assets is cheap… it's still hated… and now, the uptrend is in place.

It's "housing week" in Market Notes. On Monday, we showed you that U.S. residential real estate is still near record levels of "affordability." Today's chart shows that this incredible situation finally passes all three of Steve's True Wealth "tests."

Below, you'll find the past 30 years of inflation-adjusted home prices. You can see the incredible 40% run higher into the bubble years of 2003-2005… and you can see the incredible crash back to 20-year lows beginning in 2006.

At the far, right end of the chart, though, you'll see a little "hook" higher. This shows the first "year over year" increase since 2006. We're hardly back in boom times again. But the uptrend has begun.

– Amber Lee Mason

|

Daily Crux Best of '12Top consumer tips

Tuesday, February 21, 2012

"Forget about authoritarian governments, democratically elected ones are tracking your every move online..."

Thursday, March 15, 2012

"A number of non-monetary goods will be more valuable than a fistful of dollar bills..."

Monday, January 30, 2012

If you want to make the most of your money, avoid these places...

Tuesday, January 17, 2012

"We've been scammed..."

Recent Articles

|