Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Great News for America... and America's BanksBy

Friday, February 1, 2013

The recovery is getting louder...

Nearly a year ago, I wrote: "The U.S. banking sector hasn't been this healthy in 25 years..."

I explained that the banks, chastened by the near-apocalypse of the 2008-2009 financial meltdown, had renewed their commitment to conservative lending practices. That, combined with a resurgent housing market, was pointing to bigger bank profits...

I called it a "quiet recovery." Since then, things have only gotten better.

Banks today are nearly as strong as they've ever been.

All the positive trends I cited last year have only gained momentum... The housing recovery continues to raise asset values and decrease liabilities for both small and large banks.

Many banks have settled class-action lawsuits that resulted from the credit/mortgage crisis of 2008-2009, too. This resolves some of the undefined, potential liabilities that the banks had to prepare for... and frees up even more capital for lending.

Commercial and industrial lending is growing at nearly 12%, and it shows no sign of slowing down. The chart below shows how banks' commercial and industrial lending is just $100 billion (about 6% away) from all-time highs...

Remember, this is how banks make money – by lending. The more they lend, the more money they make.

With interest rates low, they can borrow money from depositors for next to nothing (as anyone with a savings account knows quite well). Then, they loan it out at higher rates (around 4%-5% for commercial loans). This "interest spread" allows banks to mint money.

Not only are bank profits rolling in, but almost all the banks are as healthy as they've been in almost a century.

A bank's health is measured by how much capital it has relative to its assets. For most major banks, this ratio is higher than it's been since the Great Depression. Part of the reason is regulation. The government raised the requirements after the 2008-2009 crisis... But much of it reflects the industry's return to less leveraged and more careful banking practices.

Another measure of health is the institution's "liquidity" – how much of its assets are shorter-term in nature. Liquidity helps banks react to emergencies and opportunities... You can't deploy cash unless you have it on hand. Right now, liquidity is at 30-year highs.

There are many other banking metrics that show signs of improvement. The loan-loss reserves are dropping as the economy grows and borrowers are better able to meet the commitments.

Most banks have been forced to be extra cautious over the past few years and hold back earnings for possible defaults and losses. But fewer delinquent loans means more income and fewer losses. Many of the assets on the books don't need the same super-conservative loan-loss provisions. Reallocating that set-aside money would increase book value.

This is good news for banking in general. And it's one more reason I like the banking sector.

My top recommendation in the banking sector, Wells Fargo (NYSE: WFC), is still a "strong buy." And I'm finding more great opportunities in the sector.

The crisis has passed. And the recovery is gaining strength. Now is a good time to own bank stocks.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Last year, Porter explained how the government is offering investors "a nearly risk-free way to make huge gains in bank stocks."

"Now believe me," he writes, "I know what the reaction to this idea will be... Most of my readers will never buy these banks – or any others. Some of you will even stop reading because I've suggested what is, in your eyes, heresy."

Read his full argument here: One of the Best Trades of the Next Two Years.

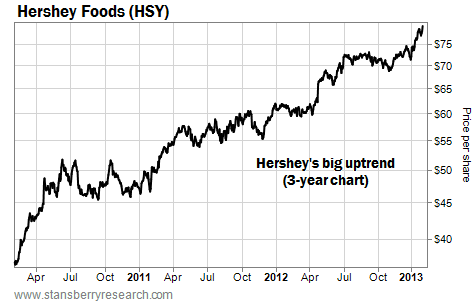

Market NotesPORTER WAS RIGHT! Porter Stansberry was right. You can make a lot of money selling chocolate...

Longtime DailyWealth readers know our colleague Porter Stansberry is a proponent of owning "capital efficient" companies like chocolate-maker Hershey Foods (NYSE: HSY). As he has written in these pages many times, Hershey is a company with big profit margins that treats its shareholders well. Buy elite companies like Hershey at bargain prices, and you can't help but get rich in common stocks.

Hershey also fits into our big theme of "owning the basics" for emerging-market investment. As we often say, investing in elite makers of basic products like chocolate, beer, and cigarettes isn't exciting. It just works.

As evidence, we point to the past three years' trading in Hershey. Today's chart shows how Hershey has marched from $35 per share to $79. Just yesterday, shares reached a new multi-year high. Porter's readers have more than doubled their money... by simply selling brand-name chocolate.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|