Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

What My 'Perfect Indicator' Is Saying About Muni BondsBy

Wednesday, August 7, 2013

Almost every finance guru I know has one person he uses as the "perfect indicator"...

This is the one person who always seems to be running with the herd... and is always doing the wrong thing with his or her investments. When that person gets incredibly bullish or incredibly bearish on an investment idea, taking the other side is a sure bet. (My colleague Jeff Clark uses the "Mother Indicator.")

My "perfect indicator," an old friend from my days in New York City, sent me a note last week. It's a huge bullish sign for one of my favorite investments. And by using this "perfect indicator," you can set yourself up for 6% tax-free yields. Let me explain...

My friend is in a panic right now. The prices of her municipal bonds have fallen. Plus, she sees all kinds of scary stories on TV and the Internet. Detroit's bankruptcy – combined with the ever-present worry about the strength and safety of the U.S. dollar – has lots of people worried about where markets and the economy in general are headed. Newspapers and television talking heads feed this worry with sensational claims.

But the broad message I give to worried investors is very simple...

Municipal bonds are one of the safest income-paying securities I know... and you should still own them.

As I've written before, muni bonds are loans to local governments. By buying a muni bond, investors give a locality cash to build roads, schools, or other public buildings. In exchange, the government promises to send investors regular interest payments and return the initial "principal" investment at the end of a set period of time.

With many "muni bonds," the local government uses its taxing authority as a promise to pay back investors. Essentially, investors don't have to worry about where the municipality is getting its money... If things get tight, it'll raise taxes.

And if the locality does get in trouble... these bonds are among the first things it has to repay in any default case. So the interest and principal repayment on these securities is nearly certain.

The numbers provide proof. The historic default rate on municipal bonds is minuscule. Investment-grade municipal bonds (those ranging in grade from A to triple-A) have a default rate of only 0.017% over the past 40 years, according to Forbes magazine.

But in the wake of Detroit's bankruptcy, some people have speculated that it could rewrite the laws governing bankruptcies and the assumptions that support the muni-bond market. For example, I've heard conjecture that the hopes and wishes of other unsecured creditors may be equally relevant in a bankruptcy court.

While the process of righting Detroit's finances will be political – and some investors are going to lose money – I disagree that Detroit will upend centuries of law and precedent in handling debt defaults.

First, remember Detroit's high-profile bankruptcy is unfortunate. But its $20 billion in debts are just one blip in the immense $3.7 trillion muni-bond market.

Also... no creditor's claims can take precedence over the senior debt. This will remain a fundamental tenet of both capitalism and the rule of law. You cannot make promises to me and sign documents that agree to the terms, then come crying later that you don't want to pay... or that you want to pay someone else what you pledged to me.

Almost all municipal debt is safe. So muni bonds (and funds that hold muni bonds) should be a part of nearly everyone's portfolios. But investor fear and slightly higher interest rates (which send bond prices lower) have caused a decline in the muni market.

Now, the bonds are trading at very cheap levels compared with other debt. And today, their yields are at all-time "rich" levels compared with other benchmark securities, like U.S. Treasury bonds. Also, they pay tax-free interest income.

The muni-bond funds in my Retirement Millionaire portfolio, like Invesco Value Municipal Income Trust (IIM), currently yield between 4.8% and 6.8%. For those in higher tax brackets, the income you receive is equivalent to getting 9%-10% on your taxable investments. Even people in lower brackets benefit from getting tax-free income (6.5%-8% equivalent).

Those yields are similar to what you can get from high-yield corporate "junk" bonds, which yield a little more than 6% according to the Merrill Lynch High Yield Index. But junk bonds are much riskier, with default rates in the high single digits of percent.

Plus, my favorite funds, like IIM, are trading at a discount to their underlying assets, which makes them an even better buy.

In summary, I'm not worried about what Detroit's bankruptcy will do to the overall municipal-bond market. The filing isn't a surprise to investors... Detroit suffered under its debt burden for decades. But that isn't stopping people like my "perfect indicator" from dumping – or worrying about – the safe muni market.

With the recent downturn in prices of muni bonds, now is the time to make sure you're fully loaded with interest-earning securities in your portfolio.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Like Doc said, 'munis' pay tax-free interest income. "This makes them a great way to earn investment income... and keep it from the taxman." Learn more here.

And Doc says there's another way to grow your money tax-free. He calls it "one of the biggest financial opportunities in America," but the numbers show it's likely you're not taking advantage of it. Get the details here: Retire 119.8% Richer Without Putting Aside a Single Extra Penny.

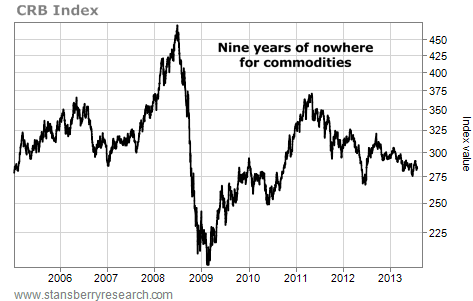

Market NotesA SURPRISING LOOK AT THE COMMODITY "SUPERCYCLE" Is the commodity "supercycle" over? Today's chart holds the answer to this question... and it might surprise you.

Many people in the investment business like to talk about the commodity "supercycle." The general idea is that we are running out of commodities like crude oil, iron ore, grains, and copper. And that means you should invest in these commodities, because shortages will produce an enormous "supercycle" bull move.

Today's chart shows this idea hasn't produced much in the way of gains for a while. Below is a nine-year chart of the benchmark CRB Index. The CRB is one of the most widely used gauges of commodity prices. It tracks the price of basic raw materials, like copper, oil, corn, natural gas, gold, sugar, cotton, and nickel.

In late 2004, the CRB sat around 283. Since then, the index has boomed and busted several times. All this volatility has left the CRB hugging the 283 level again. The commodity "supercycle" idea has been a heartbreaker for the true believers.

|

In The Daily Crux

Recent Articles

|