Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

My No. 1 Way to Reduce Interest-Rate RiskBy

Thursday, April 24, 2014

Yesterday, I exposed two popular misconceptions about rising interest rates...

First, that rates MUST rise from here... And second, that rising rates will spell doom for all income-paying investments.

In short, interest rates are much more complex and unpredictable than most investors realize. That's why the best approach is to build a diversified portfolio that's prepared for any interest-rate environment.

And today, I'm going to share a little-known investment that will reduce (or eliminate) your interest-rate risk while generating a steady stream of income. It's part of a trillion-dollar market with a 20-year history. And most investors don't have any exposure to this asset class at all.

But it can help protect your income. Let me explain...

Fixed-income investments, such as bonds, typically struggle with rising interest rates because their interest payments are fixed.

Let's look at an example...

Say you buy a bond for $100 that pays $3 in interest payments per year. That's a yield of 3%. But if the market changes and decides that these bonds should pay 4% a year, the price of your bond will fall. The bond still pays that fixed $3 interest per year... but because it now must yield 4%, the bond's price drops to $75 ($3/$75 = 4%).

The fixed nature of the interest payments means that the value of the bond must rise or fall to match the market.

So if you were concerned about rising interest rates, I'd try to find an investment with interest payments that rise with interest rates. That way, their value would be protected no matter what happens with rates. Ideally, you could get an investment that still pays a healthy yield... Then you get paid even if interest rates go nowhere.

Fortunately, this type of investment exists...

Remember that a bond is a loan from the investor (you) to the borrower (a company). In most cases, the interest payments are fixed and don't change through the life of the loan. But there's another way for investors to lend money: You can also get a variable, or floating-rate, loan.

A floating-rate loan is one where the interest payments rise or fall with interest rates.

Individuals see floating-rate loans all the time. Your credit card, mortgage, or car loans can demand interest payments that change over time.

Companies can take out floating-rate loans as well. Floating-rate loans will earn larger interest payments if rates rise, which offers investors protection from rising interest rates. And right now, they pay healthy yields, which is great even if interest rates go nowhere.

Plus, you can invest in these types of loans with a click of your mouse. Let me explain how these loans work... and how they fit in an income investor's portfolio...

To the average investor, senior floating-rate loans look a lot like bonds. They are both ways for a company to borrow money. Just like a bond, the company pays regular interest payments and the initial principal at the end.

Of course, there are some differences.

First, because we're talking about floating-rate loans, periodically (typically every quarter) the company checks a benchmark interest rate and adjusts its interest payments.

For example, tire maker Goodyear Tire took out a senior floating-rate loan in 2012. The company borrowed about $1.2 billion to refinance some existing debt.

The way that the loan is structured, Goodyear has to pay the London Interbank Offered Rate (or "LIBOR"), plus 375 basis points (3.75%). LIBOR is the benchmark rate for banks to lend money to each other.

Right now, LIBOR is about 0.23%. Based on that measure, Goodyear would pay 3.98% on its loan (0.23% plus 3.75%). If LIBOR were to rise, so would Goodyear's interest payments. But with LIBOR at just 0.23%, it's not likely to go much lower from here.

So when those interest payments rise, the income these loans generate should rise, too. That also means the value of the bond is more immune to a changing interest rate. These loans will hold their value better than a typical bond.

That explains the "floating" part of senior floating-rate loans, but what about "senior"?

Remember that bonds are typically considered a safer investment than stocks because of their claim on assets. If a company goes bankrupt, bondholders get paid out first. Shareholders only get what's left over after that.

But senior floating-rate loans rank even higher than bonds. If something bad happens to the company, no one gets a dollar until all the senior loans are paid out. Most often, they are collateralized by specific assets that will go straight to investors in the case of default.

Because of the senior status, these loans have high recovery rates in cases of default. Recovery rates measure how much money investors are able to collect from asset sales if the company goes bankrupt.

From 1996 to 2012, investors in senior floating-rate loans collected an average of $0.71 on the dollar when companies went under. That's 60% more money than the $0.43 on the dollar investors collected for typical company debt.

Of course, that's not to say that investing in senior floating-rate loans is entirely risk-free...

The companies that issue senior floating-rate loans usually have credit ratings of less than investment-grade. These companies are growing and profitable, but they don't have top-notch balance sheets.

Since 1996, the default rate on senior floating-rate loans has been 3.4%. That falls between the 0.1% default rate on investment-grade bonds and the 4.5% on speculative-grade bonds.

However, the real risk drops substantially because senior loans have such a high recovery rate in bankruptcy.

Now... there's one catch to these investments... These loans are extremely illiquid. You can't normally load up on individual bank loans with a few clicks of a computer mouse on your online trading platform. They don't have to be registered, and often the companies involved are private corporations. So they don't have to provide much financial information to anyone but the current holders of the bank loan.

That's why these loans have traditionally been the province of institutional investors and power-player financial insiders.

However, there is one way for individual investors to make the trade. In the most recent issue of Income Intelligence, I showed subscribers a safe, easy way to add senior floating-rate loans to their portfolios... And I described how they can easily diversify across many sectors and companies, making for a safe investment in this higher-yielding arena of finance.

It's important to note that these floating-rate loans allow us to reduce (or eliminate) our interest-rate risk in exchange for taking on some extra credit risk. But that's a trade we're willing to make right now. The economy is strong and default should remain low. In fact, defaults on junk-rated companies are at a six-year low of 1.5%.

This sort of trade-off will help to solidify most income investors' portfolios. Take a look at your fixed-income holdings. If you own high-quality bonds, you're exposed to interest-rate risk. By diversifying into floating-rate loans, you can reduce your exposure to interest rates and protect yourself from whatever happens in the future.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

"If your retirement plan is to sit and wait and hope to earn higher interest someday, you have no retirement plan," Steve Sjuggerud writes. "Because that day might not come." So what can you do? Learn Steve's two top places to put your money today right here.

DailyWealth classic: In 2012, everyone believed U.S. interest rates HAD to go up. But Steve predicted the opposite would happen. "History says rates could stay this low for a long time. And possibly fall even lower in the next few years. Let me explain…"

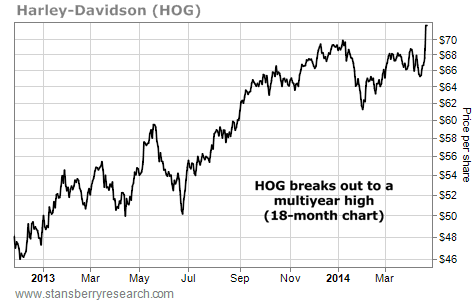

Market NotesWHAT HOG SAYS ABOUT THE ECONOMY One of our "real-world indicators" is flashing... It's telling us "things can't be all that bad" with the U.S. economy.

Longtime DailyWealth readers know we like to check in on "real-world indicators" to get a quick read of the economy... Yesterday, for example, we showed you why strength in manufacturing giants 3M and Honeywell is good news for America. Things can't be all that bad when our real-world indicators are enjoying booming profits and share prices.

Harley-Davidson (HOG) is America's largest and most popular motorcycle maker... And it's one of our favorite real-world indicators. Since many of the company's motorcycles carry a price tag of over $15,000, HOG's fortunes are tied to America's ability to spend extra money on "toys."

HOG reported quarterly earnings on Tuesday. It sold 57,415 new motorcycles in the first three months of 2014... up 5.8% from the first quarter last year. As you can see in today's chart, the stock broke out to a multiyear high on the news. It's up 64% over the last 18 months.

America is still buying toys... And HOG is climbing. That means "things can't be all that bad" with the economy.

|

Recent Articles

|