Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

One of the Most Important Lessons When Buying StocksBy

Friday, July 10, 2015

You're not going to succeed in the stock market by just buying the world's best businesses...

For the past several years, my colleague Dan Ferris and I have urged Extreme Value readers to buy great businesses... Businesses that gush free cash flow, reward shareholders, have great balance sheets, earn consistent profit margins, and have high returns on equity.

But if you pay too much, even a fantastic company can turn into a mediocre and possibly terrible investment...

That's why we also tell readers to never buy a great business until it's trading at a cheap price. This is a discipline I impose upon myself and encourage you to embrace.

To see just how a great business can turn into a mediocre – and even terrible – investment if you pay too much, let's look at American candy icon Tootsie Roll Industries (TR)...

We've never recommended Tootsie Roll, but Dan and I have followed the high-quality business for years. Tootsie Roll's results don't change much from year to year or decade to decade. Since 2005, revenue and free cash flow (FCF) have compounded at low levels of about 1.5% per year. Since revenue doesn't change much year-to-year, neither do dividends or shareholder equity.

Return on equity, or "ROE" (using free cash flow instead of the usual net income because the business is capital-intensive), is routinely a strong 15%-20%. Occasionally, when manufacturing equipment is updated and capital expenditures exceed 2% of revenue, the ROE drops to 5%-10%.

Since things don't change much operationally, it's crucial you buy shares at a cheap price. Otherwise, you lock yourself in for years of meager returns, despite the regular cash and stock dividends.

Let me illustrate...

Right now, shares trade around 24.5 times trailing 12-month free cash flow. That's expensive for outside passive minority investors like us.

If you'd bought Tootsie Roll in 2005, you'd have paid a similarly expensive multiple. Shares ended that year at $28.93, valued near 23 times FCF.

Since then, approximately $10 in cash dividends and stock splits would have reduced your cost basis from $28.93 to $18.66. (Capital returned to you lowers your cost basis dollar for dollar.)

At the end of 2014, shares closed at $30.65. That produced a compound return of just 6% per year over the full nine-year holding period. At Extreme Value, we want our investment capital to earn double-digit compound returns of 10% or better.

It was the same story if you bought in 2010. Shares were trading near $29 and at an expensive 23 times 12-month FCF. By the end of 2014, your cost basis would have been reduced to $24 by cash dividends and stock splits. Again, that's a compound return of only around 6% per year over the four-year holding period.

If you had bought when shares were cheap, though, it would have been a different story entirely...

Shares temporarily dropped to $20 in 2009 and the valuation multiple was a much-lower 15 times FCF. Since then, cash dividends and stock splits would have reduced the cost basis to about $13.68... and the compounded return on investment would've been closer to 18%, not 6%, per year.

This is one of most important lessons I can teach you about buying stocks: A great business is a great long-term investment only if you buy it when it's unusually cheap. Pay too much and you're doomed to underperform, or possibly even lose money.

This is why you should be choosy about making new trades. Stock prices have soared the past six years so most individual stocks are still too expensive to buy today.

In short, if a great business you want to buy is expensive right now, be patient. Prices tend to fluctuate. Eventually, you'll get a chance to buy it at a price that will also make it a great investment.

Good investing,

Mike Barrett

Further Reading:

Investors need to view their stock, bond, real estate, and commodities purchases just like they would view buying a house, car, phone, or groceries – don't overpay. It sounds simple... but most people can't bring themselves to do it. Learn more about this critical concept in this classic interview with Editor in Chief Brian Hunt.

"If you study what I'm about to teach you," Dan Ferris writes, "you will be able to identify companies that 'jump off the page' as wonderful investments you'd like to own one day." The best part is you won't have to pick stocks anymore. "They'll pick you!" Get all the details right here.

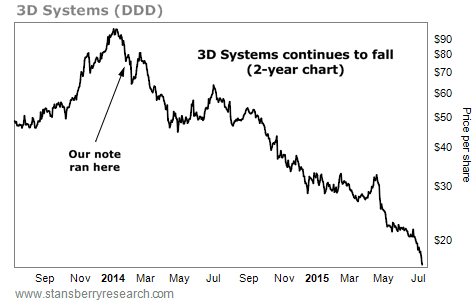

Market NotesTHINGS JUST KEEP GETTING WORSE FOR THIS POPULAR "STORY" STOCK Our warning to avoid "3D printing" stocks is still proving to be a heck of an idea...

In January 2014, we ran a warning on the market's top 3D-printing stock, 3D Systems (DDD). 3D printing is the printing of solid objects... rather than conventional "on paper" printing. The industry uses computers and special materials to "print" things like tools, guns, and toys.

Over the past few years, 3D printing has become one of the world's biggest tech stories. And with good stories come good stock rallies. Printer maker 3D Systems shot from $10 a share in late 2011 to $97 in early 2014. It's one of the biggest stock market winners in recent memory.

In our original note, we mentioned that high-growth "story" stocks like 3D Systems often get far too popular with the investment public... and far too expensive. When growth rates slow, these stocks get slammed. Our note was well-timed. Since then, 3D Systems has lost nearly 80% of its value... and just reached a new multiyear low. It continues to be a great case study in avoiding popular investments.

|

Recent Articles

|