Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Successful Investments Start With These Five Questions...By

Friday, October 9, 2015

Finding successful investments is hard work.

My colleague Dan Ferris and I routinely evaluate dozens of companies before finding a few that are worthy of additional research. Unfortunately, that means we probably spend more time reading about businesses that we don't recommend than reading about those we do.

Often, our research begins with a company's annual report. To achieve transparency with investors, public companies are required to file these reports with the U.S. Securities and Exchange Commission (SEC), which refers to them as "10-Ks."

Annual reports provide a wealth of valuable data. Better yet, the data are accessible 24/7 on the SEC website.

These reports are often 100-150 pages long and contain a mind-boggling array of numbers. Our challenge is to quickly separate what's important from what's not. Or as Arthur Conan Doyle's famous fictional sleuth Sherlock Holmes says...

How do you separate "incidental" from "vital" in a document loaded with thousands of seemingly important facts? You must have a plan. I have read thousands of annual reports in my investing career. Over time, I've developed a system that helps me quickly assess if a company is worthy of further study.

My system starts with these five questions...

Let's look at each individually... Question No. 1: Are there risks related to the company's revenue stream that aren't readily apparent?

Typically, an overview of the business and how it generates revenue can be found within the first few pages of an annual report. Spend some time there. I specifically look for two risks...

Customer Concentration Ideally, we're looking for companies that sell to many, many customers. This limits the risk that revenue might suddenly decline from the loss of any one customer. It also limits the leverage any one company can have on the business. Raising prices on a customer that's responsible for 60% of your business will always be a challenge.

Be aware that some industries routinely experience high customer concentration. Food manufacturers like Hain Celestial Group often report Wal-Mart as a major customer (10% or more of sales).

Suppliers of original equipment manufacturer (OEM) auto parts typically have high exposure to one or more of the major car manufacturers. BorgWarner, for instance, reports that 17% of its 2014 sales were made to beleaguered Volkswagen.

Companies in the semiconductor industry also routinely experience high exposure to just a few customers. Cirrus Logic is an extreme example. In 2014, 72% of its sales were made to a single customer, Apple.

Exposure to Commodity Prices

In addition to assessing customer concentration, you also want to determine if there is hidden exposure to cyclical commodities, like oil and gas.

Remember, a company doesn't have to be in the oil and gas business to have significant exposure to its boom and bust cycle. Last November, I addressed this problem in the Stansberry Digest.

Oil prices were starting to fall hard. I warned investors they might be unwittingly exposed if they owned companies that did a significant amount of business with oil and gas producers. Here's what I said at the time...

After I wrote that, the drop in oil prices did resume. And Emerson's stock price has dropped about 29% since then. Question No. 2: Are there other unusual risk factors?

Toward the middle of a typical annual report, you'll find the Risk Factors section. Here, a company identifies and lists the primary risks for its business. Many of these risks are generally the same from company to company. For instance, if a recession appears, sales are likely to decline. If another company is acquired, the integration may underperform the expectations management has set.

What I'm looking for are unique risks. Here's an example from the 2014 10-K of Molina Healthcare, which provides health care plans to more than two million members across the U.S. (emphasis added)...

This is something you don't see every day – a change of one percentage point in expenses potentially reduces income 91%! No matter how attractive Molina might otherwise be, this vital fact about its business model was a deal-breaker for me. Near the Risk Factors section, you'll usually find a financial review covering the past five years. This lets you quickly see whether the company has been successful at growing sales and profits. Growth in these two metrics is vital because it typically means the products and services the company sells are enjoying greater demand over time. Companies that get bigger and better are exactly what we're looking for.

Acxiom is an example of a company that has not been growing revenue or earnings. The provider of enterprise software has been around for more than 40 years, but sales the past two years were actually lower than they were five years ago. Earnings also trended down during this period.

By glancing at Acxiom's five-year financial history just a few minutes into my research, I was able to quickly eliminate it from consideration.

Operating leverage is simply the ability to grow profits faster than revenue. Superior business models often grow profits faster than revenue, so I consider this a vital fact that helps me quickly determine whether a particular company is worth further evaluation.

Fleetmatics provides fleet management software services to 25,000 enterprise customers with large truck fleets. It's a textbook example of operating leverage. Over the past five years, revenue grew about 37% per year on average. Income grew a much faster 85% per year on average.

Adding lots of new fleet customers didn't require the company to build a new plant. It just needed room for a few new employees and their computers. Capital-light businesses such as Fleetmatics routinely demonstrate operating leverage.

Investors love rapidly growing companies that can grow earnings quickly. They regularly pay dear prices to own them. That's why these kinds of companies are rarely found in the Extreme Value model portfolio. Ideally, we look to buy these kinds of businesses during major market downturns when everything goes on sale.

Question No. 5: Is the company generating free cash flow?

The last thing I look for when starting the evaluation of a new company is its ability to generate free cash flow. This can be easily determined by going to the Statement of Cash Flows, which normally follows the Balance Sheet and Income Statement about two-thirds of the way into a typical annual report.

Free cash flow is not a line item on the cash-flow statement. Instead, it has to be calculated by deducting expenditures for property and equipment (i.e. capital expenditures, or "CapEx") from net cash from operations (or operating cash flow).

As Dan likes to say, free cash flow is what gives equity its value. This is the surplus capital management has at its disposal to grow the business, reduce debt, and give back to shareholders via dividends and share repurchases. The cash-flow statement in an annual report normally covers the last three years. Ideally, what I'm looking for is growing free-cash-flow generation over that period. If a company was unable to generate even a moderate amount of free cash flow over the last three years, I usually lose interest in it as a potential investment idea.

There are almost 7,000 companies listed on the three major U.S. stock exchanges: NYSE, Nasdaq, and Amex. Finding the handful of businesses that will translate into successful investments is hard work.

Having a plan like the one outlined above helps us eliminate many subpar businesses from consideration quickly... and focuses our attention on those that are worthy of your investment capital.

As you conduct your own research, I highly recommend you follow this guide.

Good investing,

Mike Barrett

Further Reading:

Read more of Mike's insights in DailyWealth right here:

"In today's essay, I'll share what I've learned about how companies get bigger and better... and show you two examples of companies doing it the right way..."

"You're not going to succeed in the stock market by just buying the world's best businesses..."

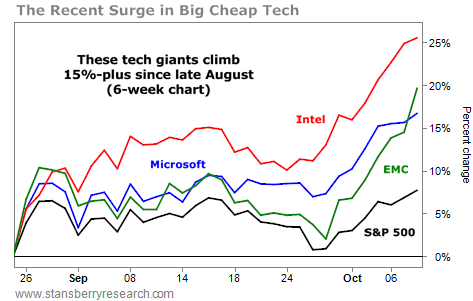

Market NotesGREAT NEWS FOR BIG CHEAP TECH Today's chart highlights an elite group of stocks leading the recent bounce in the stock market...

Longtime readers know that the tech sector has been a favorite of ours in recent years. Our "Big Cheap Tech" theme includes the biggest and best companies in the sector. These companies may not be "exciting," but they sport thick profit margins, generate huge amounts of cash, and pay ever-growing dividend streams to shareholders.

Right now, shares of three Big Cheap Tech companies are surging. And each stock dominates a separate, important part of the sector. We're talking about Microsoft (software), Intel (semiconductors), and EMC (Big Data). As you can see from the chart below, these three World Dominators are telling us the tech sector is alive and well.

Over the last six weeks, Intel shares (red line) are up 26%... EMC shares (green line) are up 20%... and Microsoft shares (blue line) are up 17%. The S&P 500 (black line) is up 8% in the same time frame. The market is recovering from its August pullback, and Big Cheap Tech is leading the way.

|

Recent Articles

|