Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today's essay is a bit longer than usual... It shares three incredibly important lessons every investor can learn from one of the most successful recommendations in our company's history...

What I Learned From Our Most Successful RecommendationBy

Friday, November 13, 2015

Four years ago, in the June 2011 issue of our Extreme Value newsletter, my colleague Dan Ferris and I recommended the best portfolio holding in our publication's 13-year history...

Readers who took our advice to buy wine producer and beer importer Constellation Brands (STZ) up to $25 per share back then have made more than five times their original investment. From our $21.24 reference price back in 2011, the total return including dividends is 555%.

There are three important lessons every investor can learn from this successful recommendation...

Lesson No. 1: Skate to Where the Puck Is Going, Not to Where It Is

Buried deep in that June 2011 issue is an analogy about successful investing I still consider one of the most insightful things Dan has ever penned. Here's what he wrote (emphasis added)...

Buying tomorrow's profits with a margin of safety today is the essence of successful investing. The key is looking into the future and imagining how the story will change. Constellation is the No. 1 premium wine producer in the U.S. and 100% owner of the No. 1 beer importer to the U.S. (Crown Imports). We correctly anticipated that Constellation Brands' distinctive wine and beer assets would continue to generate growing amounts of cash flow.

We also correctly viewed the shares as undervalued in relation to this upside. Fiscal 2011 operating cash flow was $620 million. For the last 12 months, this figure has almost doubled to $1.2 billion. That equates to operating cash flow growth of about 16% per year since 2011.

Lesson No. 2: Don't Get Complacent About an Undervalued Stock

When we issued our recommendation to buy Constellation Brands up to $25 in June 2011, shares were trading near $20. They continued to do so for the next 12 months. In other words, month after month, Constellation remained an "extreme value" and well within buying range.

As a subscriber, it was easy to get complacent and not take action.

Then out of the blue, on June 29, 2012, Extreme Value holding Anheuser-Busch InBev (BUD) announced it would divest the 50% interest in Crown Imports it was acquiring as part of the Grupo Modelo deal... and sell it to Constellation. This meant Constellation would now control 100% of Crown Imports, the largest beer importer to the U.S.

Shares rocketed higher 25% that day, closing near $27. Constellation Brands hasn't fallen back into buy range for even a single day in the three years since.

Keep this story in mind as you ponder current buys. Don't make the mistake of assuming that because they're a buy today, they will be tomorrow as well.

A quality business selling at a bargain price is an anomaly you can safely assume will eventually get corrected. Better to be a few months early than to be one day late.

Lesson No. 3: Let a Winner Run... But Regularly Ask Two Crucial Questions

When a stock becomes a big winner like Constellation has, fighting your emotions becomes a big challenge. If the stock suddenly starts declining, you wonder if you should lock in profits. If it starts surging, you wonder if you should sell amidst the sudden euphoria, particularly if the broader market has been on an extended, multiyear run.

Don't give in to these evil temptations. Avoid acting irrationally and prematurely closing a big winner by asking yourself these two questions...

For Constellation, the monitoring process has been more complicated than usual the past three years due to heavy (but temporary) capital spending. Back in 2012, when Constellation agreed to acquire the 50% of Crown Imports it didn't already own, it also agreed to expand the Nava, Mexico brewery from 10 million to 20 million hectoliters by the end of 2016. The first 5 million hectoliters of this expansion is expected to be online by the end of 2015.

Last year, in response to the beer business exceeding internal expectations, Constellation added another 5 million hectoliters to the buildout, raising total capacity to 25 million hectoliters.

Recently, the company said it's evaluating plans for even more capacity beyond 25 million hectoliters. The current brewery expansion (to 25 million hectoliters) won't be finished until fiscal 2017, and this will be the primary use of operating cash flow until then.

Continued expansion of the Nava brewery is precisely what we want to see. A larger plant is likely to manufacture more in-demand alcoholic beverages like Corona at lower unit prices and thus earn higher marginal profits.

We've re-evaluated Constellation's story each quarter over the past four years. Thus far, it has remained in alignment with our original growth thesis.

Compared with last 12 months' (LTM) free cash flow, the current share price appears to be extremely overvalued (about 52 times free cash flow). That's because expanding the Nava brewery has been (and will continue to be) the primary use of operating cash flow... and is therefore depressing free cash flow (operating cash flow less capital expenditures).

By the time fiscal 2017 begins on or around March 1, 2016, management expects the major brewery expansion to be done, leading the way to much higher free-cash-flow growth.

If capital expenditure (CapEx) spending returns to a more normal 3% of revenue (it's currently more than 10%), Constellation could generate $1.15 billion of free cash flow during fiscal 2017. That would be about five times higher than this year's projection of $200 million to $300 million. If this cash-flow surge does materialize, management maintains it'll use it to continue paying down debt, grow the dividend, and buy back shares.

At a recent price of $135 per share, Constellation trades at about 23 times our fiscal 2017 stabilized free-cash-flow estimate. That's not cheap enough to recommend buying again, but it's also well below our intrinsic value estimate (about 30 times free cash flow).

When we first recommended Constellation in 2011, shares were trading about seven times LTM free cash flow. Today, they're trading at about 23 times our estimate of 2017 free cash flow. This growth accounts for a big part of our gains. And it perfectly illustrates why we are obsessed with buying a quality business at a bargain price.

This is the kind of analysis we've been doing quarter after quarter. Monitoring Constellation's performance in relation to our original investment idea – and keeping track of its rising valuation in relation to our estimate of intrinsic value – has helped us stay in the stock and avoid the temptation of selling too early.

As you search for future big winners like Constellation, imagine how a given company's story is likely to change. Skate to where it is going, not just to where it is currently.

Then, when you find a stock that's undervalued, don't get complacent. Remember that quality companies selling for bargain prices are market anomalies that usually get corrected.

Finally, once you have a big winner, don't put it on autopilot. Regularly ask yourself if the reason you bought it is still valid and if the shares are fully valued.

Asking these questions will take emotion out of the decision-making process as much as possible and help you avoid selling a big winner prematurely.

To sum up, the three important lessons to learn from our Constellation recommendation are:

I highly recommend applying these lessons to your own investing today. Good investing,

Mike Barrett

Further Reading:

Last month, Mike shared his method for finding successful investments. "I have read thousands of annual reports in my investing career," he says. "Over time, I've developed a system that helps me quickly assess if a company is worthy of further study." Learn more right here: Successful Investments Start With These Five Questions...

Earlier this year, Mike showed readers why just buying the world's best businesses isn't enough if you want to succeed in the stock market. "This is one of the most important lessons I can teach you about buying stocks," he says. Find out what it is right here.

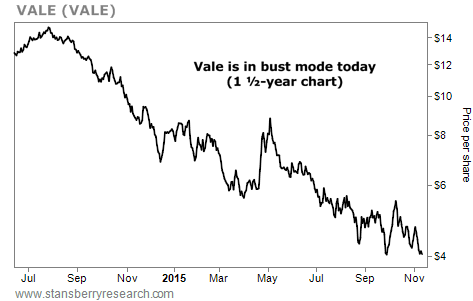

Market NotesANOTHER CAUTION ABOUT INVESTING WITH THE GOVERNMENT Shares of a multinational mining giant continue their downward spiral...

Regular readers know we often warn about the dangers of investing with the government – specifically, the corrupt Brazilian government. In short, the bureaucrats running government agencies are more interested in acquiring more power and bigger budgets than they are in improving the long-term value of a business.

We can see this downtrend at work by taking a look at Brazilian mining giant Vale (VALE). The $20 billion firm is the world's biggest producer of iron ore, a critical material for emerging economies building out their infrastructure.

As you can see from the following chart, Vale shares are in a clear downtrend. The company is down more than 70% in the last 18 months alone. It's another lesson on why "partnering with the government" is a bad idea...

|

Recent Articles

|