Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

How to Break the Shackles of the Financial IndustryBy

Friday, September 16, 2016

The investment-advisory industry is a huge, multibillion-dollar business based on hard work, clever thinking, and sophisticated algorithms. But it's also based on one teensy-weensy lie.

The lie is that you can grow wealthy investing in stocks and bonds.

It's not a big, black lie. But the unfortunate truth is that the financial establishment rarely looks beyond stocks and bonds. And if you think about it, why would it want to? It makes its money by ushering you from one "hot" stock or "amazing" fund to the next.

Because they know that you have heard that "diversification of assets" is good, financial advisers give you the illusion of diversification by filling your stock portfolio with businesses that are "diversified" into manufacturing, retail, global trade, natural resources, etc.

But at the end of the day, it's all invested in stocks or stock derivatives. The result? More risk and less potential wealth gain for you...

If you can't reasonably expect to get rich with just stocks and bonds, what can you do?

You can model your investing behavior on the behaviors that have been proven, time and time again, to actually work.

I'm talking about asset allocation.

Asset allocation is the process by which you spread your wealth across different sorts of investments.

You might think that something so dull as asset allocation could not possibly be that important in acquiring wealth, but numerous studies have shown that it may be the most important factor.

Because of an early financial disaster, I became an emotionally compulsive diversifier of practically every dollar I could save, putting some of it in bonds, some in stocks, some in cash, some in real estate, and so on.

Over the years, I have made hundreds of individual financial decisions – buy this, sell that. Some of them were good, a few of them were bad, and most of them were in between. And yet, overall, my net worth has increased considerably and consistently, without any down years, for more than 30 years.

I could see very clearly that it was not particular buy/sell decisions that accounted for this good fortune. It was the general decisions about asset allocation that paid off.

Let me give you a bird's-eye view of what I do:

I don't think my own portfolio is the best possible example of diversification. But it does reflect my belief that one needs to go well beyond some combination of stocks, bonds, and cash to win at the wealth-building game. Regards,

Mark Ford

Further Reading:

If you're middle-aged with a meager net worth and you're struggling just to keep your head above water, you might think all hope is lost. But as Mark points out, that's simply not true. "You do not have to give up on your dream of being wealthy. You always have the ability to change your financial life," he writes. "It will just take a bit of time and patience." Get the full story here: How to Become Financially Independent in Seven Years or Less.

Years ago, Mark fired his broker. "Never, ever allow a broker to be in charge of the conversation," he writes. "You're the boss. He should listen to you." See why he argues you shouldn't be "loyal" to your broker right here.

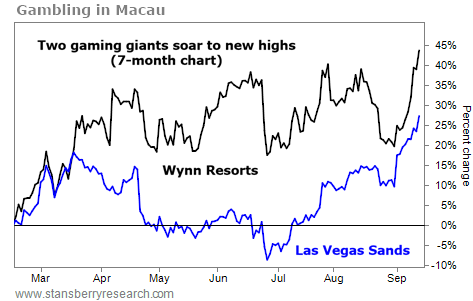

Market NotesCHINA'S GAMBLING CAPITAL PUSHES THESE STOCKS HIGHER Today, we're taking a look at the world's biggest gambling destination...

Regular readers know Steve has been talking about the potential in Macau for nearly a decade. The tiny, autonomous region is the only place where gambling is legal in China. But after years of soaring profits, gambling revenue fell into a downtrend as the Chinese economy stumbled.

That trend reversed last month as recreational gamblers headed to new resorts in Macau. Two global leaders in gambling – Wynn Resorts (WYNN) and Las Vegas Sands (LVS) – have led the way. Boosted by the changes, gaming revenue was once again on the rise in August, beating analyst estimates.

As you can see below, shares of WYNN and LVS have thrived on the recent news. Both stocks just hit fresh 52-week highs. Wynn Resorts has jumped about 20% since the beginning of this month, while Las Vegas Sands is up roughly 15%. Things appear to be back on track in China's gambling capital...

|

Recent Articles

|