Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

The Fed Don't Mean a ThingBy

Friday, October 21, 2016

This letter is the only thing you need to read about the Federal Reserve...

Ignore the sky-is-falling headlines. The Fed's decision during its December 13 and 14 meeting will have virtually no effect on your life or your investments.

Here are the basics...

The Fed is tasked with maintaining full employment and price stability by setting very short-term interest rates. It has to walk a fine line between those two goals. Low interest rates encourage economic growth, which in turn creates employment, but also risk-causing inflation.

Here's how the economy looks today... Employment is good, but it's not quite yet at "great." Meanwhile, inflation has not appeared yet.

The Fed meets in early November. According to futures markets, where traders can place bets on the outcome, the likelihood of a rate hike is only 17%. But those odds jump to 65% after the Fed's December meeting.

There's a lot of financial-media hoopla about what the Fed will do and what it will mean. Some pundits claim that rising rates will cause a disaster in the market... and your portfolio.

But they don't mean a thing (to paraphrase Duke Ellington).

Here are four reasons why you should completely ignore what the Fed does at its next meeting...

There are lots of different interest rates... from interest rates on U.S. bonds to the interest rate you earn on your savings account. The most chatter is about bonds... Bond prices and yields move in opposite directions. So some people are worried that the Fed raising interest rates means bond prices will fall.

Here's the current interest rate you'd earn on different maturities of U.S. government Treasury securities, depending on time to maturity...

Here's the point: None of these rates are controlled by the Fed... None. They're all controlled by supply and demand. If a lot of investors want to lend for five years, they'll buy up the bonds and the interest rate on five-year bonds will decline.

The only interest rate the Fed controls is the "federal funds rate"... the rate at which banks and credit unions lend to each other on an overnight basis.

Now, in theory, if the Fed raises that rate, it would hurt bonds with longer maturities (what we'd call "further out on the curve"). But in practice, this effect is miniscule.

In fact, the Federal Reserve did raise the federal funds rate from 0% to 0.25% in December of 2015. Since then, most interest rates have gone down.

Supply and demand will determine what happens with the interest rates that affect everyday life most, not the Fed's rate.

If the Federal Reserve raises rates, it will be a very small increase – say, one quarter of one percent. The Fed will then, in the future, continue to raise rates very slowly. These moves are largely symbolic. Prior to the financial crisis of 2008, the federal funds rate was regularly as high as 3% or 4%. So we could have as many as 12 or 16 raises before we're at "normal" levels again.

Make no mistake about it, this is still an "easy money" policy.

Financial markets are forward-looking... If everyone knew that a stock would be worth $10 tomorrow, they'd buy and sell until it was $10 today. Markets aren't always perfectly priced, but a rise in interest rates has been anticipated for years.

Again, in theory, higher interest rates drive down the price of bonds. This leads some to claim that the day the Fed hikes rates, bonds will plummet. But do you really think there's an investment manager sitting on a pile of bonds who hasn't considered that rates are set to go up?

As Steve says about Fed decisions, "Let me ask you... How many crises have you been able to mark in advance on your calendar?"

Many investors fear that rising rates will choke the life out of the stock market. The theory goes that higher interest rates reduce profits for companies because they pay more to borrow... Plus, other interest-paying assets will look more attractive relative to stocks.

In reality, the Fed typically raises interest rates when the economy looks healthy enough to withstand it. Right now, GDP is growing, employment is strong, and even wages are increasing a little.

In my experience, it's the real economic factors pushing stocks up that outweigh the theoretical ones that could push stocks down.

Looking at historical data, when interest rates rise from low levels, like from 0%-4%, stocks tend to rise with interest rates. (It's not as safe if rates start at higher levels... When rates rise from 5% and higher, that does tend to put pressure on stocks.)

Talking heads in the media place more importance on interest rates than they should.

Over the long term – spanning a business cycle that includes a recession and recovery – the Fed can certainly affect the path of the economy.

But in the short term – if and when the Fed announces a change before the end of the year – it won't mean much at all. Please ignore it.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Over the past year, Steve has detailed why stocks, real estate, and emerging markets actually outperform after the Fed raises interest rates. It might not be what you'd expect, but based on history, it's true. Get the details here and here.

Doc recently gave some additional advice on how to control your fears and make smart investments. Following his three simple steps can help you be a successful trader and stop worrying, no matter what the market is doing. Read more here: How to Trade Like You Have a Sixth Sense.

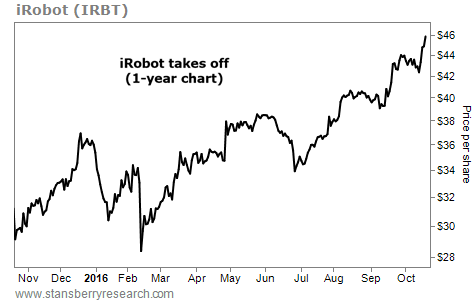

Market NotesTHE BULL MARKET IN ROBOTS America's urge to speculate in high-growth "story stocks" is alive and well. For proof, all we need to do is look at shares of iRobot (IRBT)...

There aren't many "slam dunk" guarantees you can make when it comes to investing in technology. One year's big success story is another year's big bankruptcy. But one trend we can count on is the increasing use of robots to manufacture cars, work in labs, and perform heavy military duties. As machines get lighter, faster, stronger, and smarter, the robotics market will mushroom in size.

iRobot is an industry leader. One of the world's largest robot makers, some have gone so far as to call iRobot "the GM of robots." It has a huge potential market to grow into over the coming decade.

As you can see in today's chart, investors are piling into this great "story stock." Shares of iRobot have climbed from $29 in late 2015 to $46 today, recently hitting a fresh 52-week high. With a rich price-to-earnings ratio of 33, iRobot isn't cheap... But the market is willing to "pay up" for good growth stocks right now...

|

Recent Articles

|