Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Steve's note: Regular readers know I believe the "Melt Up" stage of this bull market is now 100% here – and we need to stay invested for the biggest gains. But this kind of market environment can hide dangerous risks. Today, my colleague Dan Ferris explains one popular trade you should avoid right now...

Don't Make This Dangerous Gamble on ComplacencyBy

Wednesday, November 15, 2017

One type of trade is destined to ruin investors today.

It's a set of arcane assets that are poorly understood by those who claim to have mastered them.

In this essay, we'll take a close look at the bubble in Volatility Index ("VIX")-related investments – and why they're destined to blow up spectacularly.

Let's start with the tale of a young man who embodies all the classic foibles that destroy investors in the wake of a speculative mania (like what we're seeing today) and how his "mastery" of VIX investments will likely lead him and his ilk to ruin...

Seth Golden is a 40-year-old day trader in Ocala, Florida. A former logistics manager for retailer Target, Golden started selling short VIX-related exchange-traded products (ETPs) in 2012. Since then, he claims his net worth has risen from $500,000 to $12 million, according to an August 28 New York Times article.

The products Golden shorts are based on rolling 30-day long positions in futures contracts traded on the Chicago Board Options Exchange ("CBOE"). The basic idea of a rolling 30-day expiration is simple...

A VIX futures contract expires every month. At any given time, CBOE publishes nine serial monthly VIX futures contracts, currently from the November 2017 contract through the July 2018 contract.

This is highly simplified for illustrative purposes, but... imagine buying a November contract on November 1. Let's say it expires on November 30. On November 2, you'll have to sell enough of the November contract and buy enough of the December contract to keep the position at a 30-day average expiration. You do this every day until December 1, when you only own the December contract and the whole process starts over again.

ETPs do this so that whenever you buy shares, you'll always get the same thing: 30-day exposure to near-term VIX futures. You can also do this with more distant contracts to maintain a constant exposure to 60-day or 90-day rolling positions.

Golden says his standard position is to sell short VIX ETPs with 20% of his portfolio. He posts details of personal trades on Twitter, appears in YouTube videos, and publishes essays on websites like StockTwits.com and TalkMarkets.com.

Golden has two primary insights for shorting VIX products...

The first is that the products themselves are designed to destroy value over time. It's not absurd to bet against such a product.

In bull markets with low volatility – like the one we've been in for several years now – volatility futures tend to fall in value as they approach expiration. The contracts expire each month, locking in the losses and rolling over to the next month.

To add to the effect, the VIX futures and the ETPs based on them have historically tracked the VIX poorly.

For example, when the VIX tripled in August 2015, the most popular long VIX product – the iPath S&P 500 VIX Short-Term Futures ETN (VXX) – didn't even double. It rose 66%. Several weeks ago, the VIX rose 20.7%. VXX rose only 5.5%.

Golden is right. These are garbage securities.

The fact that Golden is shorting garbage is a big reason he's made so much money... But the main reason he's made so much money doing this is timing. We're in a bull market that has featured record lows in volatility. Confusing a bull market with financial acumen might be the most common investor foible of all.

Golden's second key insight about shorting VIX products is, as he told the New York Times recently, "The nature of volatility is that it desensitizes over time, which is why the index has been tracking down for so long."

Golden explained this further in a YouTube video titled "Shorting VIX Products for Max Profits"...

I asked Golden via Twitter, "Does [volatility] fall over time? Or is its nature to make new minima and maxima?" (In other words, doesn't volatility become more volatile over time, hitting both new highs and new lows?) His reply: "Nothing to debate here. The nature of volatility is to always seek out new low levels over time as evidenced by all defining metrics."

I asked him if the VIX would ever make a new high. He agreed it was highly probable, though it would take an "existential" shock, like 9/11. (The term is really "exogenous," meaning an event outside of and largely unrelated to day-to-day financial market activity.) But when I tried to press him further about his theories, he called me "thick" and said, "I think we're done here."

History suggests Golden doesn't understand that the VIX doesn't need exogenous shocks to hit new highs.

The top 10 new VIX all-time highs all occurred in October and November of 2008. If you look through the VIX data going back to 1990, when it first came into existence, all but a handful of the top 100 intraday highs were logged in late 2008 and early 2009 – the end of a massive financial bubble, a purely financial event.

No terrorist attack on New York and Washington, D.C. No hurricane. No North Korean nukes. No exogenous shock. Nothing "existential," as Golden put it. Just the inevitable, disastrous end to a massively overleveraged credit cycle.

Today, we're in the final innings of the single most overvalued stock market in history. The VIX could easily make multiple new highs when U.S. stocks finally come unglued. And anyone who is shorting VIX-related products could lose everything.

Volatility can remain elevated for years, and it has done so in recent history. The VIX never closed below 16 from November 1996 to December 2003 (according to data compiled by Bloomberg), spiking multiple times above 30 during that period.

How would a trader with high-minded theories about complacency and 20% of his portfolio short VIX-related products have performed during that period? It's impossible to say, since none of the VIX ETPs existed at that time.

Golden is too certain about his views on the nature of volatility, leading him to a lack of imagination. And as I've written before, an investor without imagination can't see risk until after the damage is done.

I wish Golden well, not ill. I hope he hangs on to his $12 million and makes even more. But the complacency he believes in so deeply is the sort of idea that gets you killed financially at times like this, especially when coupled with certainty and arrogance.

Be very, very careful out there. Give the short-VIX gurus a wide berth. And don't take their advice.

Good investing,

Dan Ferris

Further Reading:

"It all seemed so simple and powerful," Dan writes. Recently, he shared the story of an investor who got incredibly lucky – and walked straight into disaster. Learn how to avoid this dangerous kind of prediction right here: Is This Common Mistake Leading You to Financial Ruin?

"These are the exact same kind of instruments that led to the panic in 1987," Porter Stansberry warns. In this essay, he delves into the risks of betting against volatility – and why investors who do it could lose everything... Read more here: Where's the Biggest Bubble?

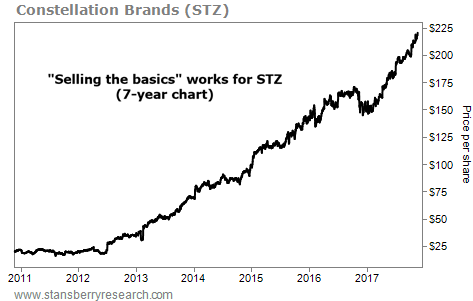

Market NotesAN EXPLOSIVE WINNER FROM THE BEVERAGE BUSINESS Today's chart shows our "selling the basics" strategy at work...

Regular readers know you don't have to take big risks to generate huge returns. For years, we've shown you the power of investing in companies that sell boring, everyday items like cigarettes, soda, toothpaste, and paper products. It's one of the most powerful ways to build steady, long-term wealth in the stock market.

One of the best examples is Constellation Brands (STZ). The $43 billion company is the No. 1 premium wine producer in the U.S. It's also the country's No. 1 beer importer. Constellation's portfolio includes more than 80 different brands, such as Robert Mondavi wine, SVEDKA vodka, and Corona beer. In June 2011, our colleague Dan Ferris told subscribers to buy shares in his excellent Extreme Value advisory.

As you can see in the chart below, his timing was spot on. Dan's readers locked in huge 631% gains last November. Shares are still climbing to new highs today. And Dan's recommendation earned the No. 3 position in the Stansberry Research Hall of Fame. Congratulations to Dan on another great call...

|

Recent Articles

|