Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Steve's note: I expect the "Melt Up" in stocks to continue higher – potentially for as long as two years. But even though my friend and colleague Porter Stansberry takes a more bearish stance, we both agree one key indicator will start the clock ticking. This week, we're sharing his two-part series on how to prepare for the "Melt Down."

And if you're looking to take the "guesswork" out of your investing, we've put our heads together to launch the perfect service for you. Read on to learn more...

A Huge Rally and an Even Bigger CollapseBy

Tuesday, January 23, 2018

I believe that 2018 will be a truly historic year in the markets.

I think it's likely that we'll see a huge "blow off" top in equity prices... and then a big reversal.

I'll explain why in detail today. Whether you agree with me or not isn't that important. What is important is that you understand some powerful underlying forces are moving the market right now. They will play a huge role this year.

I'm sharing these ideas with you because I think they're important – especially this year. But quite honestly, these "macro" thoughts aren't especially relevant to the decisions I make as an investor.

What?

In my experience, most investors dramatically "overweigh" the importance of macro forces and dramatically undervalue the skills, knowledge, and strategies that can actually deliver reliable (and safe) returns.

So... in addition to telling you what I think will happen in the markets as a whole this year (and why)... I'm also going to beg you to do three things that you've probably never done before...

These three strategies will make a much more powerful and lasting impact on your ability to increase your wealth than any of the macro ideas I could give you. And I'll show you exactly why.

But no matter what I do... I'm almost certain two things will happen:

So... why do I bother? Well, it's simple. By supporting Stansberry Research, you've given me and the almost 200 other people who work here the greatest job in the world. As Warren Buffett says, "I skip to work every day."

In return, I and the other equity partners and longtime employees at Stansberry Research have dedicated our lives to helping our subscribers make better investment decisions and achieve better investment results.

My primary job is to make sure that we continue to publish the information I'd want if our roles were reversed.

So that's how I'm starting out the year...

I'm going to do my very best to help you succeed in the financial markets, just like I have every day for the past 19 years. Thank you for giving me this opportunity.

Let's start here... with what I believe will be the major factor driving the financial markets this year...

How quickly we forget...

It was less than 10 years ago, in the closing months of 2008, when our monetary masters – led by stuttering Federal Reserve Chair Ben Bernanke – began an enormous monetary experiment. The Fed started printing new money, out of thin air. These new dollars were used to buy financial assets – mostly newly issued federal bonds, but also mortgages of dubious quality.

The result was a multiyear "one way" bet on interest rates that powered the earnings of banks, hedge funds, and traders. It also led to the largest increase in corporate and private debt ever and larger total debts than our economy had ever seen before.

The government, its private bank, and its pocket economists proved they could stop a debt crisis... by creating stupendous amounts of new debt. It was as though they'd worked a miracle.

Meanwhile, the balance sheet of the central bank in the U.S. grew from $800 billion to more than $4 trillion...

Again, this didn't just happen in America. The central bank of Japan printed more than anyone else and ended up becoming the largest shareholder in virtually every Japanese business. The Swiss central bank ended up earning more in dividends, coupon payments, and currency appreciations than any other private business in the world, about $55 billion.

And like squirrels watching a bank robbery, none of the economists and precious few investors noticed anything important happening...

Nobody noticed any inflation (because they ignored the huge rise in financial asset prices). Nobody noticed the collapse in certain commodity prices (like oil) and the resulting bankruptcies, where far too much capital had been borrowed and lent.

But eventually... like the pressure rising in a kettle, turning to steam, and blowing out with a whistle... things started going a little haywire in the global economy. By late 2016, negative interest rates threatened to destroy the global banking system. Shares of Deutsche Bank (DB), one of the world's largest banks, dove down past $10 – a critical threshold.

At the time, even junk bonds in Europe were trading with negative interest rates. European banks were paying mortgage holders to live in their houses, instead of the other way around. Commodity prices fell so far that it was cheaper for many American energy producers to burn off natural gas instead of pushing it down a pipeline. It was as though the financial world had been turned inside out and upside down. Stranger Things wasn't just a TV show: It was our financial reality.

And then, what I believe was the final and ultimate warning sign of this big inflationary bubble – cryptocurrencies...

Last year, the bubble reached a whole new kind of level, something we hadn't seen since the days of the South Sea Bubble. Digital "tokens" – backed by nothing, yielding nothing, and conveying nothing – began to soar in value, merely because they, unlike paper currency, couldn't be manipulated by central bankers. By North Korean hackers? Maybe. But not central bankers.

The greatest monetary experiment in modern history is drawing toward a close...

The crytpo bubble must have finally been too much to ignore. Even squirrels could tell something was wrong with our money. And so... the tide has begun to head out.

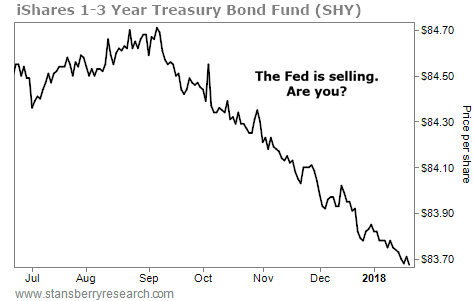

Most investors don't know anything about this... But the Fed is quietly reversing course. It's draining the system of reserves. On October 1, the Fed began to allow its balance sheet to "run off" by $10 billion a month. That is, as the bonds it holds mature, it won't "roll" the assets into new securities. And so, for the last three months, the Fed has seen its balance sheet shrink by $6 billion a month in U.S. Treasury securities and $4 billion a month in mortgage securities.

You can see for yourself what this is doing to the prices of short-term U.S. bonds. They've gone down in basically a straight line since the policy change was announced in September 2017.

It took the speculative bubble a long time to reach negative interest rates on junk bonds and $20,000 cryptocurrencies. It will likewise take a while (but not as long) for this fundamental change in the financial markets to hurt sentiment and securities prices. But make no mistake, the tide is going out... And the tide is going to get more powerful as it moves.

I don't mean that rhetorically or as some kind of metaphysical prediction. I mean the size of the Fed's reserve decreases will accelerate for all of 2018. Specifically, the amount of securities the Fed will no longer roll forward will increase at $10 billion per month for all of 2018. Doing the math, that's a $420 billion decrease in the size of the Fed's balance sheet in one year. That's a sizeable reduction in demand for both mortgages and U.S. Treasury securities.

And just as speculators enjoyed a one-way bet on the way up, they now have a one-way bet on the way down.

The link between the Fed's purchases (and sales) of securities and the other markets isn't direct...

The Fed's actions will primarily impact interest rates (and bond prices) at the short end of the curve – that's bonds and mortgages with durations of five years or less.

Far more important to equity prices and the sentiment of the bond market are the prices and yields on longer-duration mortgages and the 10-year U.S. Treasury bond. You can think of the yield of the 10-year Treasury bond as a kind of gas pedal for the price of global financial assets. The lower it goes, the more gas is being sent into financial markets. But as the pedal rises, those carburetors are getting less and less fuel... and the motor is going to slow.

As you can see in the chart below, the price of longer-term bonds is also moving in the wrong direction in a pretty linear fashion.

Again, the resulting impact on financial markets won't be immediate. It isn't direct. But it is, like gravity, irresistible. The Fed's actions and the resulting higher interest rates are going to eventually put a "pin" in the global financial bubble. The clock is ticking. Let me give you one example of how this macro force impacts the real economy...

Most banks and all mortgage-finance companies borrow money at a short-term rate, like two years. They then lend out this capital at the higher, long-term rate, like 10 years. As long as short-term capital costs less to borrow than long-term capital (and it should), then the banks and mortgage companies have a great, capital-efficient business. They're using other people's money to make a fortune.

The trouble is... sometimes unusual things happen... unusual things like a central bank selling off hundreds and hundreds of billions in short-term mortgages and Treasury debt into a market that knows that billions and billions more are coming.

In these unusual periods, short-term rates can rise to match, or even exceed, long-term rates. When that happens, the banks and mortgage companies can't earn more (or anything) from lending. They can quickly get into big financial trouble because they can't finance their outstanding loan packages at a profitable rate.

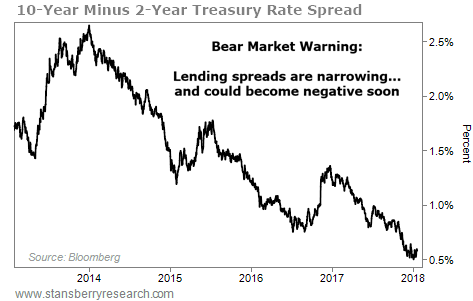

Because of the Fed's actions, it's highly likely that 2018 will see one of these rare "inversions" between short- and long-term rates. This so-called "inverted yield curve" would be the final "get out of the pool" warning before the storm.

As you can see in the chart below, the spread between two- and 10-year interest rates has been narrowing since 2014. It's now approaching a critical level – half a percentage point. As the spread gets closer and closer to zero, it will become progressively more difficult for banks and mortgage companies to access capital, which will reduce the market's liquidity substantially.

Let's make a safe prediction: 2018 will see some big financial fireworks... Amid the backdrop of tightening financial conditions and the Fed's decision to remove hundreds of billions in liquidity from the financial markets, you have one of the longest-running bull markets in history, a record-high level of bullish sentiment, and a fading crypto mania that was the single-greatest speculative event in our lifetimes.

My bet is that we'll see a number of additional record highs in the equity markets, as this amount of investor euphoria will not die easily. Watch for something: At some point, you'll see a new "lower low." That is, at some point over the next six months or so, you'll see a real dip in the markets. You'll see the indexes fall below previous lows.

You'll see some kind of important financial weakness. It might be a rise in bad loans (like subprime autos). Or it might be in bank earnings, thanks to a much tighter or even inverted yield curve. Something in the character of the market, something fundamental will change. Most investors won't notice. But you will.

And you'll know what's coming.

Great bear markets don't start when people are worried and the markets are quiet. They began in periods of incredible excitement and financial euphoria. They begin with markets at all-time highs, when speculation is rampant.

In summary... let me paraphrase Warren Buffett...

Your success as an investor can be predicted in a few simple ways, but I don't believe any indicator is more important than your ability to be cautious when others are greedy and to be greedy when others are afraid.

Many of you weren't subscribers back in 2009 and 2012, when we were "pounding" the table for investors to buy stocks. Both Steve and myself made the largest equity investments in our lives back in late 2008 and early 2009.

Today, I'm telling you the opposite. Yes, stocks may still run higher. But this market is running on fumes. We will see it all fall apart this year.

Still, as I said earlier, none of this should matter very much to your investing approach...

So tomorrow, I'll review three of the most important and fundamental investment strategies that we know will work, no matter what kind of market we see develop in 2018.

Regards,

Porter Stansberry

Further Reading:

The last three times the Fed pushed short-term interest rates above long-term rates, the stock market peaked – but not right away. Steve discusses what history tells us about this key indicator in his recent essay: All Right, Mr. 'Melt Up'... So When Does It End?

"Right now, we're seeing signs that the market needs to catch its breath," Justin Brill writes. In the Weekend Edition, he shares three potential warning signs for stocks. But as he explains, selling your stocks now could be a terrible mistake... Read more here.

Market NotesTHIS WELL-KNOWN COMPANY CONTINUES TO DOMINATE Today, we check in on an established company that churns out reliable gains...

Regular readers know investing in "World Dominators" is one of the safest strategies on the planet. These companies sit at the top of their industries, thanks to their wide brand recognition and outstanding customer loyalty. They're well-positioned to survive just about anything. And right now, another one of these elite businesses is thriving...

For decades, Johnson & Johnson (JNJ) has been a leader in consumer health care products, medical devices, and pharmaceuticals. Its brands include household names like Band-Aid bandages, Listerine mouthwash, Tylenol pain reliever, and skin-care brands Neutrogena and Aveeno. You probably have Johnson & Johnson products in your medicine cabinet at home. This competitive edge has given the company huge profit margins over the years. And that means dependable returns for investors...

As you can see in the chart below, shares have rallied nearly 33% over the past year, and they're now hitting new all-time highs. It's one more example of why you should invest in the best businesses in the world...

|

Recent Articles

|