Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today's edition of DailyWealth is a little unusual. In place of our usual essay format, we're bringing you an interview with income investor and editor of The 12% Letter, Dan Ferris. Dan focuses on the potential risks of an investment above almost any other consideration. But as he explains, risk isn't that hard to avoid if you use just a few simple strategies...

The Three Big Risks You're Taking Every Time You Invest Your MoneyBy

Friday, January 18, 2013

The Daily Crux: In a recent issue of your 12% Letter, you wrote that there are three serious risks every investor needs to be aware of. What are they, and why are they so important?

Dan Ferris: Well, I know just mentioning the word "risk" can cause many folks to run for the hills. But I hope your readers will give me just a minute to explain.

This topic isn't nearly as complicated as most people think... and managing risk is literally one of the most important things you can do to ensure investing success.

In fact, many of the world's most successful investors consider risk management to be the most important factor in their success.

As you mentioned, there are three major types of risk that all investors need to be aware of... and avoid at all costs if they want to be successful.

The first is called valuation risk. This is simply the risk that you'll pay too much for your investments, causing you to earn less money – or even lose money – on them.

This risk is probably the most important, because it's the only one of the three that an investor can totally control... after all, no one can force you to buy a particular stock at a particular price.

Crux: What can an investor do to control or avoid this risk?

Ferris: Well, it's less about what you can do, and more about what you can avoid doing. An investor can control valuation risk by refusing to pay too much when he makes a new investment.

Of course, buying low and selling high runs contrary to human nature, and is one of the most difficult things for the average investor to do. Rising stock prices feel good, but they're a major problem for investors who want to avoid valuation risk.

Many investors are lured to believe there's less risk as stock prices rise. They feel more comfortable... which makes them think they're taking on less risk. But of course that's not true at all... The exact opposite is true.

Stocks become riskier as valuations rise. When a stock's valuation rises too high – like the vast majority did in early 2000 and late 2007 – and risk hits an unsustainably high level, prices are certain to fall sooner or later. And when they finally do fall, it's usually a collapse.

To think about it another way, suppose a particular company earns $1 per share. Would the stock be riskier when it sells for $13 or $23 a share? When asked that way, almost anyone could answer it correctly. The stock is riskier at the higher price and less risky at the lower price.

In general, if the company is growing earnings at all, 13 times earnings – $13 a share in this example – is a cheap valuation, and unless it's one of my World Dominating Dividend Growers or another super-high-quality business, $23 a share is too expensive to buy safely.

Determining how much to pay is not an exact science, however, and there are a number of different methods professional investors use. When I set the maximum buy prices for my 12% Letter recommendations, I try to balance the price-to-earnings ratio, the dividend yield, and the dividend-growth rates, and come up with a conservative number.

It's not complicated... But if you can consistently avoid paying too much for stocks and only buy them when they're cheap enough, you'll realize returns the vast majority of investors never see. One the other hand, if you consistently pay too much for stocks, nothing can save you.

Crux: What's the second major risk investors face?

Ferris: The second risk is business risk. This is the risk that something will go wrong with the business and hurt its ability to earn and grow profits. This risk could come from bad management decisions, increased competition, changes in the industry, or any number of other areas.

Regardless of the cause, companies with high business risk are likely to earn less in the future. Because a stock is simply a claim to a company's future earnings, it's clear your returns are likely to be lower as well.

Crux: How can investors avoid business risk?

Ferris: The easy way to avoid this risk is to buy only high-quality businesses... companies that have excellent management teams and grow earnings like clockwork year after year.

One of the key traits of the highest-quality businesses is they're much more likely to grow and much less likely to shrink than most businesses.

An easy way to find these companies is to look at their dividends. Companies that earn more year after year also tend to pay higher dividends year after year. So companies with a long history of consistent dividend growth tend to have very low business risk.

Two other clues to identify high-quality businesses include consistent profit margins and plenty of free cash flow.

Companies that have all three traits in spades – like my World Dominating Dividend Growers – are likely to be among the highest-quality, lowest-business-risk companies in the world.

Crux: And finally, what's the third investment risk?

Ferris: The third investment risk is known as balance sheet risk. This is the risk that a business will fail or get in trouble because it can't pay its debts.

This is probably the simplest type of risk to understand and avoid... All it really requires is finding companies with much more cash than they'll ever need to pay their debts.

For example, if a company has $63 billion in cash and less than $12 billion in debt – which one of our World Dominating Dividend Growers does – the whole company could shut down tomorrow, and it could easily pay off all its debt and still have tens of billions of dollars left to distribute to shareholders. There's practically no balance sheet risk in a business like this.

But a company doesn't have to have that kind of cash hoard to have low balance sheet risk. I also like to look at the amount of interest the company pays compared to how much it earns. If a company can earn many times more each year than it pays out in interest payments, balance sheet risk is often low.

The best part is, it takes just a few minutes to take a look at a company's balance sheet to see if it has more cash than debt and/or earns many times its interest expense. This makes it very easy to find companies with low balance sheet risk.

Crux: Sounds great... Any parting thoughts?

Ferris: As I mentioned to my readers, learning how to access these three types of risk will take a little time. But it's guaranteed to be time well spent.

Avoiding these risks will do more to guarantee your investment success than almost anything else out there... and it's accessible to the professional and amateur investor alike.

Of course, if any readers don't have the time or inclination to master these techniques themselves, I encourage them to try The 12% Letter. I never make a recommendation without checking off each of these three risks.

Crux: Thanks for talking with us, Dan.

Ferris: My pleasure.

Further Reading:

The Daily Crux has put together an incredible collection of useful, insightful interviews over the years. You can find them all here.

For timeless advice on the markets, look for ones labeled "the world's greatest investment ideas." Here is a handful of our favorites:

Market NotesGET READY FOR MORE VOLATILITY It's about time for the DailyWealth "law of volatility" to take effect...

At DailyWealth, we know there are few sure bets in the financial markets. There are few "this is the case, and it always will be" statements we're comfortable making. The market is too messy and too dynamic for those types of claims.

But one "this is the case, and always will be" statement we'll stick by is this: "Calm periods of rosy headlines and softly rising prices will always be interrupted by periods of wrenching volatility... and vice versa." That's just the way the world works. Statisticians call this idea "reversion to the mean."

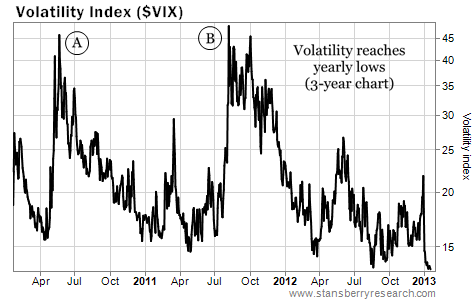

For a picture of this "always the case, always will be" phenomenon, we present the past three years of the Volatility Index (the "VIX") – the most popular gauge of market volatility. When the VIX is low (around 15), it indicates investors have few worries and see blue skies ahead. When the VIX is high (above 30), it indicates panic and confusion.

In early 2010, investors were enjoying the "good times" of the market recovery. The calmness was shattered by the flash crash (spike "A"). In mid-2011, investors were enjoying another calm period... which was shattered by the European debt crisis (spike "B"). As you can see in the lower right-hand corner of our chart, the VIX just plummeted to a yearly low. But it's just a matter of time before a new problem catapults it higher.

– Brian Hunt

|

In The Daily Crux

Recent Articles

|