|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

It Is a Sure Bet – a Guaranteed Lock – Junk Bonds Will CrashBy

Wednesday, June 19, 2013

We didn't mean to call the top. But it sure looks like we did...

On May 10, I issued this warning to my readers:

The U.S. bond market – particularly junk bonds – is going to crash. When this crash occurs, it will be the largest destruction of wealth in history... As I explained then, I believe we'll see a real panic in the corporate bond market at some point in the next year. I expect the average price of non-investment-grade debt (aka junk bonds) to fall 50%. Investment-grade bonds will fall substantially, too. (I'd estimate somewhere around 25%.) This is going to wipe out a huge amount of capital... and believe me... it's 100% guaranteed to happen. It's already starting...

On May 7, the yield on the Barclays U.S. Corporate High Yield Index fell to a record low of 4.97%. It was the first day in the history of the U.S. junk bond market (where less creditworthy companies borrow) that the index yield fell to less than 5%.

The next day, yields fell again to 4.96%.

Watching the action that week, we simply couldn't believe our eyes... General Motors issued new debt paying a yield of only 3.75%. General Motors is sitting on roughly $100 billion in pension obligations. It went bankrupt less than five years ago. And it operates in a sector that's still suffering from massive overcapacity. To say GM's five-year note isn't investment-grade could be the punch line of a joke.

At yet... there it was. You should imagine us sitting at our desk, rubbing our eyes in disbelief.

It is impossible to justify the high price of junk bonds (and their correspondingly low yields). You must remember that the default rate on these bonds will soar, sooner or later.

In March 2009, the default rate on this category of debt hit 14.9%. And of course, default rates rise when more bonds are issued. Issuance hit an all-time record in 2012. Through the beginning of May, the high-yield sector was on pace to beat that record this year.

In other words, never before in modern American finance have so many investors placed so much capital in riskier assets with less compensation. It is a sure bet – a 100%, guaranteed lock – these investments will end badly.

Believe it or not, that's not even the worst sign that the debt market is headed for an enormous crash.

Not only are investors no longer being compensated adequately for the risk of default, issuers of these debts have also succeeded in placing clauses in the contracts that allow them to repay investors with additional debt securities rather than cash.

So-called pay-in-kind (PIK) toggle notes allow corporate borrowers the option of issuing still more debt rather than paying bondholders interest in cash. These kinds of terms were invented during the last credit bubble, at the height of the market in 2006 and 2007.

Needless to say, a borrower who requires the option to repay you with still more debt isn't likely to repay you. These investments are sure to end badly, too.

The default rate on high-yield paper hit what appears to be a low in April at 3%. The default rate has now begun to tick up, inching to 3.1% in May. This will surely increase. The cycle will turn (as it always does). Higher rates will come. Refinancing terms will be tougher and tougher. Defaults will soar. This is certain.

And so, in the May 10 edition of our e-letter, the S&A Digest, we issued our warning:

The coming collapse in the bond market will be far worse than it was last time, too. This time, the Federal Reserve's actions have driven forward the huge bull market in bonds. The Fed is printing up almost $100 billion per month and buying bonds. That has forced the other buyers of bonds to buy riskier debt that, historically, offered much higher yields. As bond yields rise, the price of bonds will fall sharply. We were right. Since early May, the iShares High-Yield Bond Fund (HYG) has given up all the capital gains it made in the previous seven months. And on June 6, market research firm Lipper released data showing a record volume of investor redemption from mutual funds and exchange-traded funds holding high-yield bonds. Investors pulled $4.6 billion out of the high-yield market.

It's time to get out of bonds... especially high-yield corporate bonds.

Regards,

Porter Stansberry

Further Reading:

Over the past few months, Porter has detailed the insanity of the world's bond market. He thinks it's "without a doubt the single greatest threat to your wealth you will ever face." And for those who don't own gold, "it could soon be too late." Read Porter's full argument here.

It's important to remember that a crisis can create great bargains. When this happens, you should be ready to step in and make profitable, "bad to less bad" trades. "Bad to less bad" trading is one of the most powerful financial concepts in the world. Read a brief educational interview on this idea right here.

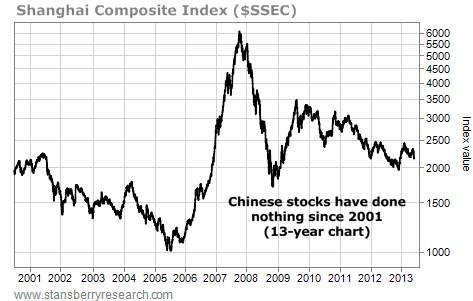

Market NotesCHINA: HIGH GROWTH, LOW RETURNS Earlier this year, we exposed a big investment myth: You make the best returns buying into "high growth" economies.

Many so-called "experts" promote this myth. But our research shows what knowledgeable investors have known for years: You make the most money buying stocks when economic growth is stagnant or declining.

This is because great conditions get "priced in" to the stock market. By the time things are great, stocks are usually too expensive... and due for a big fall. When things are terrible, stocks become very cheap... and due for a rise. (A country's corporate climate can also kill investor returns.)

To see this idea at work, consider China. For the past decade, it's been the world's fastest-growing large economy. But many of its publicly traded companies have absurd levels of corruption and waste. As you can see from the chart below, this has caused the Shanghai Composite Index – its benchmark stock index – to register zero returns since 2001. Anyone who bought Chinese stocks with the idea that "growth means returns" has learned that lesson...

|

In The Daily Crux

Recent Articles

|