Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

How to Collect Thousands of Dollars in 'Hidden Income'By

Wednesday, December 3, 2014

When you look at a water fountain, what do you see?

A chance to get a drink of water? A place where other people's germs hang out?

I see a way to earn thousands of dollars a year in extra income.

A water fountain is like many things in your everyday life. It can be used to generate lots of extra income for you and your family. This income is reliable... and available to anyone. You simply have to know how to look for it.

Now back to the water fountain...

Each time someone uses a water fountain or a toilet... a water bill must be paid. Water and sewer systems are often built by local municipalities.

The tax revenues that your city and state collect from these things can be turned into your very own "hidden" income.

And you'll also get to earn that income tax-free. You do it by buying municipal bonds, also known as "munis."

Muni bonds are loans to local governments. By buying a muni bond, an investor loans a municipality cash to build roads, schools, or other public buildings. In exchange, the government promises to send investors regular interest payments. At the end of the bond's life, they also return the initial "principal" investment.

Municipal bonds are a remarkably safe investment.

Investment-grade municipal bonds (those ranging in grade from A to triple-A) have had a default rate of only 0.017% over the past 40 years, according to Forbes magazine. In other words, less than two out of every 10,000 investment-grade municipal bonds default.

Put another way, if you invest $100 into muni bonds, you can expect to lose only 1.7 cents from cities or states that end up unable to pay you back over 40 years.

Municipal bonds can pay anywhere from 3% to 7%, depending on what cities or states issued them and what tax revenues they can tap to pay off the interest.

You also can earn income from these bonds tax-free.

That's because income from munis is exempt from federal income tax. And if you own bonds that were issued from your own state, you won't have to pay state taxes, either. (This is the case in most states, but you should check your local laws.)

So for instance, if you earn 6% on a municipal bond and you're in the 25% tax bracket, you end up with the same income as if you earned 8% in a taxable investment.

It's true that buying municipal bonds directly can be difficult and confusing.

The brokerage fees are expensive, the transactions are complex, and the minimum investments are high. Plus, sorting through the 1.5 million different bonds further complicates things.

I've found a way around all that. After all, I doubt you want to take the time to become a muni-bond expert and manage a complex portfolio.

That's why I like to buy bonds through investment funds dedicated to owning municipal bonds. For an example, let's look at the Invesco Value Municipal Income Trust (IIM)...

IIM holds more than 300 different municipal bonds, worth a total of around $1.1 billion. The average bond in its portfolio yields around 4%. But because the fund borrows a bit of capital to increase its leverage to buy some bonds on margin, IIM yields more than 5%.

If you look at IIM's portfolio, it sticks to very safe munis from safe issuers.

About 75% of its funds are invested bonds that have received an investment rating of Baa level or higher. Of that group, the riskiest ones have just a 0.1349% chance of defaulting in 10 years (or 13 out of 10,000).

There are different types of munis for different services. Some are "revenue bonds" that are tied to specific projects. For example, a revenue bond can be used to build a stadium and the income investors receive comes from the rent that sports teams or concerts pay to use it.

The safest types of bonds are "general obligation" bonds. These bonds are backed by the entire power of the state or municipality. This means that the state can and will use funds from anywhere to keep paying bondholders.

So rather than paying out of your pocket for your local government services – and the services of all your neighbors – you can turn those services into positive income inflows. It's a "hidden" income opportunity many overlook.

And with municipal-bond funds, you can get a diversified collection of the top-rated bonds in just a few minutes.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Last week, Doc showed readers how to collect more safe income from lower oil prices. "Nothing is more powerful to the global economy than the price of oil," he writes. "And the massive move down has created equally extreme opportunities for investment." Get all the details here: Are You Taking Advantage of This Free-Market 'Stimulus Package'?

Doc also recently shared what he calls the "perfect income investment." It's a way to earn a 7.3% income stream... and you've likely never considered it. "This investment has the safety of a bond. It pays regular income. But it's better than a bond... because it has the upside of stocks. And right now, it's on sale..." Find out what it is right here.

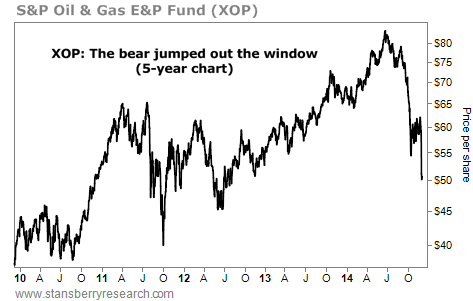

Market NotesTHE BEAR JUMPS OUT THE WINDOW "The bull climbs the stairs, the bear jumps out the window."

This Wall Street saying describes a bull market's tendency to advance in a stair-step fashion over a period of years... while a bear market tends to be shorter and feature much sharper price moves (jump out the window).

This saying describes the recent action in oil stocks. The price of crude oil has fallen from $100 to $65 in five months, which has made hash out of an oil-stock uptrend that took years to build. The recent action in the S&P Oil & Gas Exploration & Production Fund (XOP) tells the story.

In 2012, XOP started a bull market that took it from $44 per share to $83 per share in two years. As you can see, XOP has plunged... and erased almost all the gains in just five months.

There's a simple reason behind the market's ability to destroy value faster than it creates value. To move prices higher, a market requires large and consistent amounts of buying. To move prices lower, a market needs only the absence of buying. It's like a choo-choo train. It takes extraordinary horsepower to move a train uphill. To move a train downhill, you only need gravity. This has been a painful lesson for oil-stock investors this year.

|

Recent Articles

|