Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: This week we're sharing some of our best ideas on how to minimize your tax bill. Yesterday, we shared how one simple move could save you thousands of dollars each year. Today, Dr. David Eifrig shares another easy way to keep the government away from your hard-earned money. Read on to learn how you can...

Use This Simple Tax Move for an Instant 33% ReturnBy

Tuesday, February 10, 2015

Most people view taxes as unavoidable... They're inevitable, like death, right?

That thinking leads many people to ignore the huge benefits gained from investing through tax-sheltered accounts. But in an effort to protect us from its own taxes, the government graciously allows individuals to invest through several tax-deferred accounts.

The main examples are an individual retirement account ("IRA") and a 401(k). In the next two essays, I'll explain how these accounts work... and how they can provide you with instant returns that will compound your wealth for many years to come.

Today, I'll cover the huge benefits offered by opening an IRA...

An IRA lets you park your cash and compound your wealth tax-free.

You don't have to pay taxes on capital gains, dividends, or interest income for any stocks, bonds, or funds you hold within an IRA. (If nothing else, this makes for simple accounting come tax time.) Even better, you make contributions to a traditional IRA with pre-tax dollars (up to a certain level of income).

For instance, say you make $100,000. With a marginal tax rate of 25%, you would owe roughly $16,857 a year in taxes (depending on a lot of other assumptions). So you'll take home $83,143. If both you and your spouse make the maximum annual IRA contributions of $5,500, you'll adjust your taxable income to $89,000. Your tax bill will drop to $14,107. You end up taking home $74,892... but you also set aside $11,000.

Another way to look at it:

You get $11,000, but it only cost you $8,251. That's an immediate 33% return on your investment, which you then compound for decades.

The only downside is that you can't withdraw your money until you reach 59 and a half years of age. If you do withdraw before then, you have to pay the taxes due on it plus a 10% penalty.

After 59 and a half, your withdrawals are taxed as ordinary income. If you withdraw $50,000 a year, that will count toward your annual income. You'll be taxed accordingly. And when you reach 70 and a half, you must start making the minimum required withdrawals.

In short, if you don't have an IRA now... open one immediately!

Opening an IRA is as easy as opening any other brokerage account. You can do it with any brokerage. When registering, you simply select an IRA as the account type.

When you file your taxes at the end of the year, the forms include a line to enter any IRA contributions. It's as simple as that. By skipping taxes, you've already made a huge investment gain.

And that 33% boost on your initial capital will save you tens of thousands of dollars over just a decade or two of retirement savings.

Don't leave that free money on the table...

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Get more of Doc's "armchair wisdom" and investment advice right here:

My No. 1 Way to Reduce Interest-Rate Risk

This little-known investment will reduce (or eliminate) your interest-rate risk while generating a steady stream of income... What You NEED to Know About Rising Interest Rates

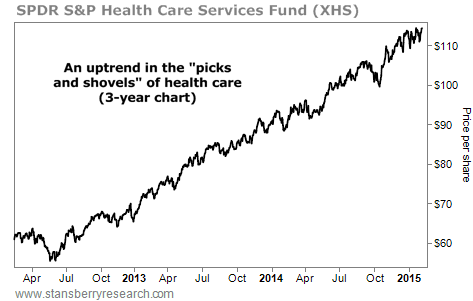

I know interest rates aren't the most exciting topic to most readers. But understanding what they mean for the market can put you ahead of 99% of the crowd... Market NotesA BIG PICKS AND SHOVELS WINNER Of all the trends in the market right now, few are as strong as the one in health care's "picks and shovels."

Regular readers know we're proponents of investing in picks and shovels companies to profit from sector and commodity booms. Picks and shovels providers don't bet the company on one project... They sell vital goods and services to an industry (read our educational interview about it here).

As we've covered many times, the health care industry is booming right now. The Baby Boomer generation is increasing its health care consumption. Plus, Obamacare is boosting demand.

This is great for investment funds like the S&P Health Care Services fund (XHS). It holds a diversified basket of picks and shovels providers to the health care industry. As you can see from the chart below, business is booming. XHS is up nearly 100% in the past three years.

|

Recent Articles

|