Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

What You Should Ask Your Money Manager Today – Right NowBy

Friday, July 26, 2013

The financial industry is adept at keeping its customers in the dark about what they are spending.

There are plenty of regulations in place that are supposed to make such costs transparent, but most of the disclosures are in small print and peppered with legal terms.

I'm not suggesting that all fees and charges are unfair. In fact, decades of consumer advocacy have reduced the number and types of tricks brokers, financial advisors, and money managers use to fleece their clients.

But there are still things to watch out for...

Some money managers and financial advisors provide a range of financial services, including asset allocation, stock and bond recommendations, reporting, and so on.

Most of them will charge you a fee for financial advice. Some will also collect commissions on any transactions.

One of the biggest problems with money managers and financial advisors is that they have a predisposition for mutual funds. They like mutual funds because they are easy. But as you know, mutual funds are very expensive.

And that's not all... With a money manager, you are likely paying other fees, too. My colleague Tim Mittelstaedt, the editor in chief at The Palm Beach Letter, has a good friend with a UBS-managed account. Tim studied the fine print and this is what he found:

The fine print showed other fees that were impossible to decipher:

So Tim's friend is paying 2.44% in disclosed fees – and he may be paying even more if you consider the hidden or hard-to-decipher fees. There is an argument to be made that fee-only financial advisors and/or money managers are better because you don't have to pay transactions costs. This is not necessarily true. Your account could be billed for certain transaction costs separately. The money manager doesn't receive this fee, but you pay it.

The only way to know what you are paying a financial advisor and/or money manager is to write them a letter asking them to disclose all costs clearly and fully.

If you use a money manager or financial advisor, you should expect him to be completely forthcoming and transparent about what you are paying. If you aren't sure, the first step is to ask him in writing, "Please send me a clear and comprehensive account of all charges, fees, commissions, and other costs I am paying for your service."

And ask him to copy his manager on that message.

If you are ever told, "There is no commission on a purchase," you are speaking to a liar. It may be true that no actual commissions (as defined by the industry) are being charged, but you can be sure that there are other charges, either embedded in the transaction or put through to you as "management fees."

As with stockbrokers, there are some situations in which you may be happy to pay the fees they are charging. And there are certainly financial advisors and money managers who are smart and caring and do a good job.

But you need to know exactly what the costs are – immediately and over time.

Then, and only then, can you decide if these sorts of services are good for you.

Regards,

Mark Ford

Further Reading:

When it comes to business and financial relationships, Mark says, "I've learned that getting the cheapest deal doesn't necessarily mean you're getting the best deal. I want expert advice and great service. And I don't want to overpay for it... But I don't want to underpay, either." That's why Mark says there are three qualities he looks for before going into business with anyone. Find out what they are here.

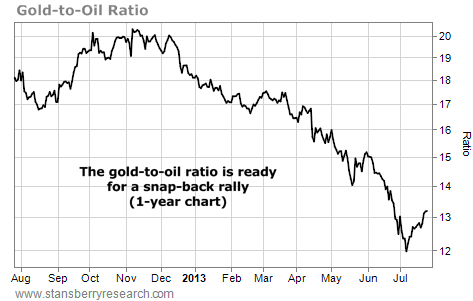

Market NotesAN UNUSUAL GOLD RALLY IS IN THE CARDS Get ready for a rally in the most important ratio you're not following... the "gold-to-oil" ratio.

Most folks don't know about it, but there is an interesting world of trading ideas that can be termed "ratio trades." These aren't the conventional "buy a stock and hope it goes up" trades. They involve trading one asset against another asset. For example, one of the most important ratios in this group is the "gold-to-oil" ratio.

Since they are both commodities that have intrinsic value, gold and oil can be affected by the same buying and selling pressure in the market. But their values can get "out of whack." When this happens, traders can step in to sell gold and buy oil... or buy gold and sell oil. The profit on these trades depends on how the two assets move against each other... rather than moving in U.S. dollar terms. We used this analysis to time – almost to the day – the epic 2008 bottom in crude oil.

Over the past 10 months, the gold-to-oil ratio has fallen from 20 to 12. This means gold has collapsed in value relative to oil. Now, the whole world hates gold... and hedge funds hold massive short bets against it. Conversely, hedge funds hold massive long bets on crude oil. Look for "hated" gold to rally against "loved" crude oil.

|

In The Daily Crux

Recent Articles

|