Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: This week we're sharing our best ideas on how to legally lower your tax bill. On Monday, we shared a simple way to save thousands on taxes each year. Yesterday, we covered how to earn an instant 33% return using a tax-sheltered account. Today, Dr. David Eifrig shares a simple "one click" way to collect substantial tax-free income on your savings. Read on to learn...

How to Legally "Opt Out" of Federal Income TaxesBy

Wednesday, February 11, 2015

If you're a retiree... or if you're simply looking to earn safe interest on your money... you have two enemies:

1. Federal income tax rates that can take a 20%-30% bite out of your earnings. In some cases, that number is as high as 40%.

2. Interest rates that are near record lows. Right now, you're lucky if you can make even 1% on your bank savings... And that's before taxes.

Fortunately, you can fix this situation quickly.

You just need to know how to legally "opt out" of federal income taxes on your savings... and where to find much higher (but still safe) rates of income...

Let me show you what I mean...

Right now, the highest-yielding one-year Certificate of Deposits (CDs) pay about 1%. Most banks offer a little less... But for this example, we'll use the banks offering the highest yields.

The federal government will tax the income you collect from CDs just like ordinary income. For most folks, this means they must pay Uncle Sam 25%-28% of any interest earned. For high earners, the tax rate is 39.6%. Keep these figures in mind... We'll come back to them in a moment.

But first, you need to know you have the option of placing your money into another safe investment. This investment pays more than 5%... and the interest is free from federal taxes. If you live in a state with zero income tax (like Florida or Texas), you pay no tax at all.

So... a saver has the option of parking his money in the bank... We'll call that "option A" – or in this investment... "option B." Here's how the numbers stack up after you factor in taxes:

As you can see, it's no contest. By owning this safe, alternative investment, you can earn nearly seven times more interest on your savings. For a $10,000 investment, that's an extra $428 after just one year. If you're in a higher income bracket and put in a larger chunk of savings, the numbers get ridiculous. For example, on a $100,000 chunk of savings, you'll earn over $4,000 more a year with this tax-free strategy versus a high-yield CD.

And you can start earning this income RIGHT NOW. It will take you just five minutes. All you need is a regular brokerage account. And all you need to do is buy one of my recommended "muni bond" funds.

As regular readers know, municipal bonds are loans made to state and municipal governments. To encourage folks to invest in the government, interest received from "munis" is exempt from federal income tax. And again, if you live in a zero-income-tax state, you'll pay $0 in taxes on your income.

Right now, one of my favorite muni-bond funds, the Invesco Insured Municipal Income Trust (IIM), is offering you a little more than 5% in annual interest. By buying this fund, you park your money in loans to various state and local entities. It's a diversified fund that owns over 300 different bond issues. And as of yesterday, it's even trading at a small discount to the value of its bonds.

Of course, unlike a traditional CD, there's no guarantee that the price of the fund won't fall. So this isn't something you want to put ALL your savings into. But these bonds are backed by the taxing power of state and local governments. And they're insured against default. A fund like IIM is a safe choice for a good portion of your portfolio (up to 5%).

If you've earned and saved your whole life and would like to earn income on those savings, stop shortchanging yourself. Consider "opting out" of federal taxes and moving some of your savings into a muni-bond fund.

It's safe... and you can start earning nearly seven times more income than you do in the bank.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Learn how muni bonds can also help you build a diverse, disaster-proof portfolio right here:

How to Build a Portfolio That Will Handle Any Crisis

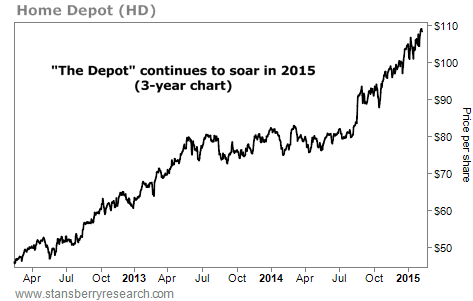

"This will have 1,000 times greater impact on your wealth than any single trade..." Market Notes"THE DEPOT" IS STILL SOARING Another month goes by... and "The Depot" tells us things are a heck of a lot stronger than the pessimists would have you believe.

Over the past few years, we've highlighted many charts that reveal an important idea: While the U.S. economy isn't booming, it can't be doing all that bad. For example, we've noted the tremendous share-price strength in super-bank Wells Fargo and American entertainment giant Disney.

But let's not forget about Home Depot (HD). Owning and maintaining a home is the American dream. "The Depot" is America's largest home-improvement chain. It sells the things we need to install new kitchens, remodel bathrooms, and build home additions. This makes Home Depot's share price an excellent gauge of what's happening in America.

As you can see from today's chart, things are "happening." Three years ago, Home Depot shares traded for less than $45. Since then, business has been good enough to send the stock more than 150% higher. Yesterday, shares struck a new all-time high. If "The Depot" is doing this well, things can't be all that bad.

|

Recent Articles

|