Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: It's Exchange-Traded Fund (ETF) Week here in DailyWealth. And we're sharing the top reasons why we love ETFs. Today, we highlight one of the biggest benefits of ETF investing... low fees. Read on to learn why...

This Essay Could Literally Save You Millions of DollarsBy

Tuesday, February 17, 2015

If you have an IRA, 401k, or any other kind of "traditional" investment account, you need to hear today's message.

These types of accounts often push you into mutual fund investments. And while mutual funds do offer some of the benefits of ETFs... they come with a dirty secret: outrageous fees.

Over a lifetime, these high mutual funds fees could literally cost you millions compared to low-cost ETF investing.

Here's why...

Investing in mutual funds comes with a few problems... First, mutual funds charge high fees (called "expense ratios"). Second, you can end up on the hook for taxes, even if you don't realize any gains.

My good friend Mebane Faber has been crusading against mutual funds for years. He's the chief investment officer and portfolio manager for Cambria Investment Management. And he built Cambria in hopes of upending the mutual-fund industry.

Over the past few years, he has done extensive homework on just how expensive mutual funds actually are. He found major differences between the fees mutual funds charge and the fees ETFs charge. Take a look...

Passive funds track an index, like the S&P 500. Active funds have managers that select investments (a value fund would only buys cheap stocks, for example).

As you can see, ETFs have much lower expenses than mutual funds. And according to Meb's research, the tax benefit of ETFs is even greater...

You see, in both mutual funds and ETFs, fund managers buy and sell stocks or bonds. Whenever a security sells for a profit in a mutual fund, the U.S. government wants its cut. So often, mutual funds pay capital gains at the end of the year. And you're on the hook for the tax bill.

Sometimes, even investors who lose money in a mutual fund are still on the hook for a capital gains tax bill... That's ridiculous!

ETFs use a different structure. It allows them to buy and sell whatever they want without worrying about capital gains taxes. You only pay taxes when you sell the ETF.

According to Meb, ETFs offer tax savings of 0.3%-2.0% a year over mutual funds.

When you combine the tax and fee savings, Meb estimates ETFs save up to 2% a year over mutual funds.

That might not seem like much. But over a lifetime of investing, it quickly adds up...

Take two investors, Jack and Jill. They both make the same investments. But Jack uses mutual funds while Jill invests in ETFs.

They both invest $10,000 a year in the stock market. Stocks have returned 10.8% a year since 1950. So for the sake of this example, we'll assume Jack and Jill earn the same return going forward.

Over time, Jill's low-cost ETF portfolio crushes Jack's. Take a look...

As you can see, those 2% annual costs really add up. After 40 years, Jack has lost nearly $2.5 million in potential gains. His account size is 43% smaller than Jill's... even though they made identical investments. Of course, some mutual funds are better than others... some offer lower fees. But the tax problem won't go away.

In short, ETFs give us all of the benefits of mutual funds... But without the enormous cost. And that's absolutely vital to any long-term investor.

Good investing,

Steve

Further Reading:

Taxes are another silent killer on your returns. Here are three proven ways to lower your tax burden:

This is one of the easiest, simplest ways to increase your ability to build wealth.

This idea will provide you with instant returns that will compound your wealth for many years to come.

You can still take advantage of one of the most powerful tax loopholes available...

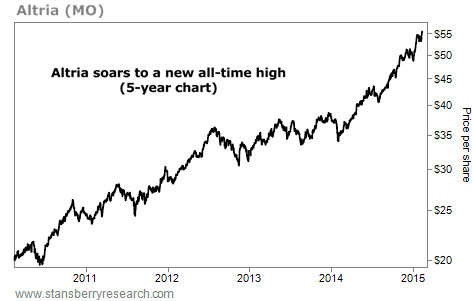

Market NotesSELLING THE BASICS: CIGARETTES EDITION Our "basics" approach isn't just working for brewing companies... it's working for cigarette companies as well.

As we reminded you on Friday, we're fans of owning "boring," basic businesses that sell things like soda, soap, toothpaste, food, beer, and cigarettes. These firms don't produce "next big thing" technologies, but demand for their products is constant. And it's unlikely a new technology will render having a beer after work obsolete.

On Friday, we pointed to the major uptrend in global brewing giant Anheuser-Busch InBev (BUD) as a way to take advantage of this idea. Today, we look at another great "basics" leader... U.S. cigarette powerhouse Altria (MO). Our friend and colleague Tom Dyson wrote an excellent piece on the company, which you can read here.

As you can see below, things are going well for Altria. Shares are up 175% over the past five years... and just struck a new all-time high last week. It's further proof that selling the basics isn't exciting... it just works.

|

Recent Articles

|