Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Don't Buy Another Tech Stock Until You Read ThisBy

Wednesday, April 8, 2015

I love tech stocks...

Not the market-darling social networks or the absurd valuations in the venture capital market. I love tech stocks that provide sometimes dull, but always necessary, products: the hardware and software essential for business and communication.

The services are so vital, I call them "Digital Utilities." In the same way you expect running water and electricity to get your daily business done, you expect a reliable Internet connection, some basic software, and an accurate search engine.

If you've been reading my research for any amount of time, you've heard this story before.

But how do you find Digital Utilities and dodge wild tech companies? I'll let you in on a secret... It's easy.

You see, for every wild tech company burning through cash, a select few create massive profitable cash flows by providing essential services.

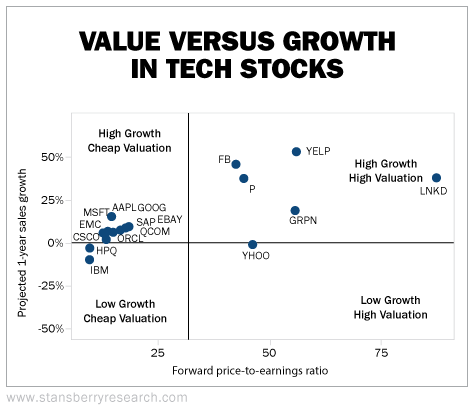

Take a look at the following chart. It shows the expected sales growth for selected tech companies over the next year, along with their current valuation, as measured by price-to-earnings ratio.

We didn't include stocks like Twitter, software maker Splunk (SPLK), and online-game developer Zynga (ZYNG). Their valuations were so high, they'd literally be off the chart. What you're looking for in a Digital Utility is positive growth and a low valuation. It's really no different than what you look for in any stock investment.

That means the cluster of stocks collected in the upper-left quadrant offer the best values.

You've seen these names in my writing before. Businesses like Oracle, Qualcomm, and Cisco all post consistent profitable growth and all trade at valuations near or below the rest of the market.

Many of them – like Cisco and Microsoft – even have respectable and consistent dividend yields.

Take Microsoft, for instance...

Microsoft operates around the globe in many segments of the computing, business, and gaming world. Almost everyone knows Microsoft's products. In the last 12 months, the company sold $91 billion in goods and services, up an unbelievable 13% over the previous year.

MSFT has a real business. While many think of the Xbox gaming system or its new tablets, MSFT makes its money by selling other things that are absolutely critical to business. Things like Microsoft Office software or the operating systems that run business servers.

I'm using Microsoft Word to write this now. And my company paid for the software.

And that real business generates huge cash flows. Over the last four years, MSFT has generated more than $100 billion in free cash flow. MSFT has amassed more than $80 billion in cash on its balance sheet.

The company is paying that extra cash back to shareholders with a 3.1% dividend yield and $26 billion in planned share buybacks.

Microsoft currently trades for about 17 times earnings, while the rest of the market trades for about 18.5 times earnings.

Sure, you're not likely to get a short-term 300% gain on Digital Utilities like Microsoft.

But these companies are safe, steady, cash-gushing machines. The need for routers and switches, word processors, and efficient search engines isn't likely to decline any time soon. Better yet, these healthy businesses should continue to treat shareholders well and provide excellent vehicles for compounding your wealth over the long term.

If you want to find the best tech stocks in the world to own, I suggest you pass on the market darlings and focus on Digital Utilities. And as I showed you above, finding them is simple.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

You can find more "common sense" wisdom from Doc right here:

Is the Government Lying About Unemployment?

Let's cut through the political spin and look at the facts on unemployment... Is the CPI Telling Us the Full Story on Inflation?

A variety of inflation stats show that things are not heating up... Is the U.S. Headed for a Recession?

It's clear the economy is doing well. But it's not as overheated as many bears would have you believe... Market NotesAN UPDATE ON ONE OF OUR FAVORITE GOLD STOCKS Today's chart shows the gold-royalty model is alive and well... and doing a lot better than gold.

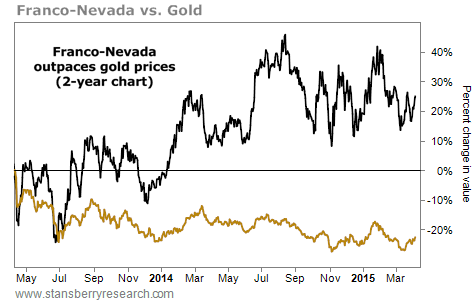

For years now, DailyWealth has urged readers interested in gold stocks to buy "royalty" firms. Royalty firms don't operate mines or explore for mineral deposits. They finance early stage mining projects and collect royalties when those projects work out. This makes a royalty firm safer and more diversified than a company that "bets it all" on just one project.

One of the top royalty firms is Franco-Nevada (FNV). It owns interests in dozens of valuable mining properties around the world. When professional investors want exposure to royalty firms, they often buy Franco-Nevada.

You can see how well the gold-royalty model is working in the chart below. It plots the performance of Franco-Nevada (black line) over the past two years versus the performance of gold prices (gold line) over the same time frame. Franco-Nevada has returned about 20%. Gold is down nearly 25%. As you can see, gold-royalty firms can do well even if the price of gold doesn't.

|

Recent Articles

|