Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Are You Holding These Ticking Time Bombs In Your Portfolio?By

Wednesday, May 20, 2015

When are your safest investments a threat to your wealth?

When you hold them in a very common – but very wrong – way.

Most retirees don't realize it, but some of their safest investments are major threats to their wealth. Below, I'll show you why you need to sell these so-called "safe" investments right now... and I'll provide a much better option for your portfolio today.

Let's get started...

Longtime readers know that I love a balanced portfolio... One that's diversified and allocated across many assets.

Fixed-income securities – specifically bonds – are an important part of any balanced portfolio. You put your money into a bond and lock up a certain yield. Then, you get paid year after year for loaning the bond issuer your money.

That's why bonds are considered a safer way for retirees to earn a return on their savings... rather than being exposed to the ups and downs of the stock market.

The thing is, not all bond investments are the same. And as I'll show you in a moment, many investors are making a big mistake with the way they hold bonds today – simply because they don't know any better.

Let me explain...

Over the years, I've talked a lot about the differences between open-end funds and closed-end funds (you can read my educational interview on the subject here).

In short, most of the funds folks are familiar with are open-end funds, like the traditional mutual funds you might own in a 401(k)... or exchange-traded funds (ETFs) you might own in an IRA.

"Open-end" means the fund will issue as many shares as investors are willing to buy. When investors put more money into the fund, the fund issues more shares and buys more of the underlying asset – in this case, bonds.

Conversely, when investors pull money out of an open-end fund, the fund must liquidate shares and sell off the underlying asset to give shareholders their money back.

This is precisely what makes open-end bond funds so dangerous today...

You see, the beauty of fixed-income investments, like bonds, is that you can buy them (individually) and then hold to maturity, collecting the interest payments along the way and the principal repayment at the end. But that only works if you have a long-term view and personal control of the portfolio.

Bond prices fluctuate, so if you trade in and out of bonds, you can take losses at the wrong time.

That's what happens when a lot of investors in open-end bond funds want their money back at the same time... The fund managers have to sell some of the bonds they hold to raise cash and repay investors. With the selling, the prices of the bonds drop. Then, shareholders of other mutual funds see the prices dropping and demand their money back, too. And suddenly, it's a scramble for the exits.

Unlike an individual, open-end funds don't get to hold and collect their bond payments until maturity. If shareholders want money, they have to sell whatever they have to raise the funds.

So even if you are a long-term investor, your fund manager might not have that luxury. That's why we hate open-end funds.

Even worse is that these kinds of funds are so common...

According to the 2015 Investment Company Fact Book, $15.9 trillion of the $18.2 trillion of assets held at U.S. investment companies is in the form of open-end mutual funds. Another $2 trillion is held in open-end ETFs.

According to the same report, open-end bond mutual funds experienced net inflows of $44 billion, last year alone. Since 2005, bond mutual funds have received $1.9 trillion in net inflows and reinvested dividends. And that's not even factoring in the inflows to bond ETFs.

When all this money starts scrambling for the exits, it's not going to be pretty.

For this reason, we prefer closed-end bond funds that don't have to sell to redeem investor money. As I mentioned, when closed-end-fund shareholders want their money back, they simply sell those shares to another investor (like a traditional stock). That transaction has no bearing on the capital available for the fund to invest. You can find all kinds of closed-end funds at www.cefconnect.com.

In the meantime, we recommend reviewing your bond-fund holdings and selling all of the open-end funds immediately.

If you're holding closed-end bond funds, the ride could still get rough. Prices can still go down. But know that the fund won't have to sell its holdings because the price is dropping. And if rates do explode upward (which we think is unlikely), the closed-end-fund manager can use maturing bond funds to buy new higher-yielding bonds. This is a win-win for closed-end-fund bond holders.

Just make sure they aren't leveraged bond funds of any type – that will get ugly when rates go higher.

Bottom line, use closed-end bond funds instead of open-end bond funds for long-term retirement-saving purposes.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

One of Doc's favorite bond investments over the past few years has been closed-end municipal bond funds. "If you switch some of your capital into muni bonds, the income they generate will flow to you, tax-free," he writes. "And with municipal-bond funds, you can get a diversified collection of the top-rated bonds in just a few minutes." Get the full story here.

Doc also recently showed readers a way to earn double-digit yields outside of the stock market. "These yields are safe," he writes. "And they're a great way to diversify your income portfolio and reduce exposure to stocks." Learn more here.

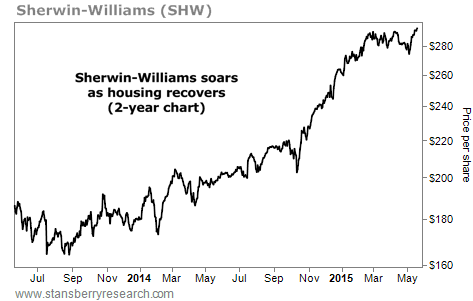

Market NotesANOTHER NEW HIGH FOR THIS 'PICKS AND SHOVELS' WINNER Today's chart provides an update on one of the biggest "picks and shovels" winners in the housing rebound...

Regular readers know we're proponents of investing in picks-and-shovels companies to profit from sector and commodity booms. Picks-and-shovels providers don't bet the company on one project... They sell vital goods and services to an industry (read our educational interview about it here).

Back in April, we showed you the big uptrend in Sherwin-Williams (SHW). As we explained, Sherwin-Williams is a "picks and shovels" provider to the housing industry. Sherwin-Williams doesn't build houses or manage a portfolio of properties. Rather, it's one of America's largest paint suppliers. As more houses are built or remodeled, people buy more paint.

As you can see below, folks are buying plenty of paint. Shares of SHW are up more than 150% in the past three years. Just yesterday, the U.S. Census Bureau reported that housing starts in April jumped to their highest level since 2007. Shares of Sherwin-Williams reached a new all-time high on the news. As the housing sector continues to recover, picks-and-shovels providers like SHW will continue to benefit.

|

Recent Articles

|