Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today, we're sharing one of the first essays from Dr. David Eifrig's brand-new project, Retirement Millionaire Daily. It's a free daily letter packed with intriguing health and wealth ideas... and tips on how to live a "millionaire lifestyle" on far, far less than you can imagine. (You can sign up right here.) Read on to learn...

What the 'Junk-Bond Crisis' Means for Muni BondsBy

Thursday, October 15, 2015

It could happen next week... or next month...

Wall Street is already sending warning signals about the next financial cataclysm. Analysts are using phrases like "liquidity crunch" and "crisis situation."

I'm talking about the impending crisis in high-yield ("junk") corporate bonds. When this crisis happens, some investors will get wiped out... while others will make a killing...

But some folks are, right now, making a costly mistake by lumping municipal bonds into that same crisis.

Today, I'd like to explain municipal bonds... why they shouldn't be confused with high-yield "junk" bonds... and why they can be a sleep-well-at-night asset during a crisis.

What are municipal bonds?

Municipal bonds – or "munis" – are loans that investors make to cities and states to build roads, schools, or other public buildings. For example... toll roads in California, water distribution in Texas, and maintenance of the New Jersey Turnpike.

In return, the government promises to send investors regular interest payments, plus return the initial investment, called the "principal," at the end of a set period of time.

How much do munis pay you?

Right now, muni bond funds are yielding about 5.5%. That seems pretty good at a time when savings accounts yield less than 1%. But the income is even better than it looks...

As an incentive to get folks to loan their money to cities and states, the income you earn from muni bonds is exempt from federal taxes. If you're in the 28% tax bracket, that makes a 5.5% yield the equivalent to a 7% taxable yield.

How often do you get paid?

Many municipal-bond funds are structured to pay out interest monthly... perfect for retirees who are looking for a safe, dependable income stream. Most muni funds have paid out like clockwork since they were established... every single month.

Are these bonds safe for your portfolio?

Muni bonds are incredibly safe... Most are backed by the full taxing power of the issuing municipality. If money runs short, the city or state can raise taxes and pay off its bills. That's what makes munis so safe.

From 1970 to 2013, an investment-grade municipal bond had a 0.08% chance of defaulting over 10 years. During that same period, junk bonds had about a 3% chance of defaulting over 10 years.

What's the worst-case scenario if everything falls apart?

We don't have to look far to find a prime example of nearly everything going wrong for muni-bond holders... In 2013, Detroit was a true nightmare scenario for muni bonds. The city had more than $20 million in debt that raising taxes wouldn't fix. After making deals with creditors, Detroit was able to exit bankruptcy in December 2014.

But even in this worst-case scenario, being a Detroit bondholder wasn't all that bad. If you held what were known as "unlimited-tax general-obligation" bonds – basically the all-purpose Detroit bonds – you collected $0.74 on the dollar in the final settlement.

So in the absolute worst-case scenario, most bondholders took just a 26% loss on face value... And remember, these bondholders also collected interest payments during the time leading up to the city's default.

What if the Fed hikes interest rates?

Investors think that the Federal Reserve will raise its benchmark interest rate sometime this fall or early next year. Whenever that rate goes up, it will make other investments look less attractive in comparison.

Rates and prices move in opposite directions. If a bond pays 3% and rates rise to 5%, the price of the bond declines because investors can easily find higher-yielding investments than the original 3% bond.

But as far as we can calculate, most of the potential for higher rates has already been "priced in" to muni-bond prices.

Are muni bonds a good choice for you?

If you own mostly stocks, then buying bonds will help balance out some of the ups and downs of your portfolio. The prices of muni bonds usually move independently from stocks. And their consistent history of paying steady dividends can help you sleep at night.

But like all assets, you want to buy muni bonds at a good price...

When should you buy muni bonds?

Right now, muni bonds are trading cheap... near the depths of where they traded during the global financial crisis. And if you watch the headlines... or, better yet, are a subscriber of my Income Intelligence advisory service... you can use "headline risk" to figure out an even better time to buy.

If you see a big drop and scary headlines, it probably means a lot of investors are overreacting to a single event... like Detroit, Puerto Rico (which defaulted on $58 million in debt in August), or a liquidity crisis.

Where should you put muni bonds when you buy them?

Because most muni bonds are tax-advantaged... that is, you don't have to pay taxes on some or all of the distributions that they pay out... it makes more sense to hold them in a regular, taxable brokerage account instead of your 401(k) or IRA.

Why won't a junk-bond crisis hurt muni bonds?

Muni bonds may have rocky ups and downs in the near future, but I don't expect the same liquidity problems in munis that are likely in corporate bonds.

I've been telling readers to buy municipal bonds for a long time. I even went on national TV to make my case. Municipal bonds have been – and will continue to be – a great deal for income-seeking investors.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

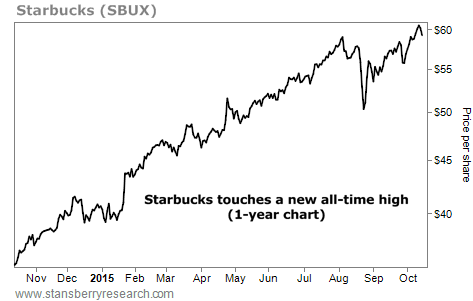

Market NotesTHE POWER OF INVESTING IN HABITS Today's chart showcases one of the all-time great investment secrets: investing in habits.

Longtime DailyWealth readers are familiar with this powerful strategy... As Editor in Chief Brian Hunt says, if people only knew this secret of investing, they could ignore just about everything else. By "investing in habits," we mean owning companies that sell habit-forming or addictive products, like soda, fast food, candy, cigarettes, and alcohol.

One of the best examples of this idea at work is coffee megachain Starbucks (SBUX). Starbucks is undoubtedly one of the most popular stocks in the market... and it's one of America's best businesses. The company has developed a product that millions of people love and rely on every day.

As you can see from the chart below, people still can't get enough of their Starbucks "fix." Shares just struck a new all-time high... and are up 65% over the past year, including dividends. It's clear to see that investing in habits is a proven way to generate wealth based on common sense.

|

Recent Articles

|