Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: We're wrapping up the week with a special two-part series from Stansberry Research founder Porter Stansberry. Over the next two days, you'll learn all about one of the easiest ways to lose money in the market: investing in "value traps." As you'll see, it's a mistake even one of the world's greatest investors made...

Why Buying Cheap Stocks Can Be DeadlyBy

Thursday, March 17, 2016

It was the greatest investment mistake of all time... a cumulative loss of more than $200 billion.

It started out as a lie. Then it got worse. It got worse every year for 20 years. But even that lesson didn't really stick. The same investor repeated these same mistakes again and again. The first mistake happened in 1965. The last one didn't liquidate until 2001. That's 36 years of making the same mistake.

The person I'm describing is investing legend Warren Buffett. Yes, he's widely admired as the greatest investor of all time. But he's also made some of the biggest errors of all time, too.

As you'll see, the core error that Buffett made several different times was getting caught in "value traps." That same error, in at least three instances over 36 years, resulted in catastrophic losses. If you've ever lost money buying what you thought was a cheap (and therefore safe) stock, my bet is you have made the exact same error.

Today, I'll show you the details of this particular kind of investment mistake...

Most people don't know the most important and most basic fact of Buffett's investment career. He began his career in the 1950s and early 1960s as a deep-value investor – someone who looked for stocks trading well below their net asset value (book value). His original strategy was to buy the cheapest stocks and find a way to liquidate his holdings at a fair market value. In his 1989 letter to shareholders, Buffett used the metaphor of finding a cigar butt on the ground to describe his method...

However... all too often, this approach caused him lots of problems, especially as his operations grew in size and he began taking control of companies. After that point, his strategy proved to be far too cumbersome and risky. Selling the assets became difficult or even impossible. Again and again, he found himself "trapped" with low-quality assets that he couldn't sell for any price. Working with investors over the past 20 years, I've seen lots of people make huge mistakes buying expensive stocks, from the Internet darlings of the late 1990s to real estate stocks in 2007.

It's not difficult to learn why this happened and how to avoid expensive stocks... You just don't buy anything that is wildly popular, a newly minted initial public offering (IPO), or trading at 50 times earnings. But learning how to avoid big investment mistakes in cheap stocks is a lot more difficult, as Buffett's track record demonstrates. In many cases, these opportunities seem the safest... which is why they can be particularly deadly.

Let's start with the big one...

In 1962, Buffett began buying shares in a beaten-down former industrial powerhouse called Berkshire Hathaway. The company, which once was among the largest businesses in New England, had been in decline since the end of World War II. Cheaper, non-union labor in the South and a slew of new innovations made the company's mills obsolete.

By the time Buffett took control in 1964, the company's previous nine years of operations saw revenues of more than $500 million... but an aggregate loss of $10 million. The business was no longer competitive in the market. Management responded by closing down mills, selling assets, and generating cash for its balance sheet. The result was a company with far greater assets on its books ($22 million) than its share price... and a lot of cash.

Buffett figured he could buy the stock safely because sooner or later, Berkshire Hathaway's then-CEO (Seabury Stanton), whose family had owned and run the business for decades, would try to buy it back from him. That's exactly what happened. In 1964, Buffett negotiated with Stanton to tender (sell) his shares back to the company. They verbally agreed on a price: $11.50 per share. But when the formal tender offer was published, the asking price was reduced by one-eighth of a point – to only 11 and three-eighths. What happened next was a disaster. As Buffett told CNBC...

Buffett was now saddled with a failing textile maker. To escape the industry's grim economics, he began to invest the company's cash flows in businesses with better prospects. The first thing he bought was insurance company National Indemnity in 1967. As you likely know, Buffett would continue to use Berkshire Hathaway as his main investment vehicle. He bought stakes in other high-quality businesses like insurance firm Geico, credit-card company American Express, soft-drink empire Coca-Cola, and dozens more. It was these investment decisions that have made him and his fellow shareholders roughly 20% a year since 1965.

But the situation raises an interesting question: Why didn't Buffett simply borrow (or raise from investors) the capital he needed to buy the insurance companies and the other blue-chip stocks? Why did he fool around with Berkshire at all? Putting all of these great assets into Berkshire was a horrible mistake, because Berkshire continued to require a lot of capital. Says Buffett...

Buffett got "trapped" by owning a lousy business. He even doubled down on his bet by buying Waumbec Mills (another New England textile company) and merging it with Berkshire. In investment circles, this situation is known as a "value trap." Plenty of great investors have seen their careers ruined because they took an oversized position in a stock that looked really cheap, but actually was worth a lot less than its balance sheet suggested. Here's the key concept to grasp: It didn't matter how much money Buffett could afford to put into Berkshire. It didn't matter what Berkshire management decided to try next. Low-cost competition was decimating the economics of its entire industry. More than 250 different textile firms went bankrupt between 1980 and 1985.

As a result, every dollar Buffett put into Berkshire's textile business was going to be a dollar lost – as Buffett found out when he tried to liquidate Berkshire's assets at an auction held in early 1986, which he described in a shareholder letter soon after...

This isn't the only time Buffett made an error of this same kind... In 1966, shortly after buying Berkshire, he partnered with Charlie Munger to buy the failing Baltimore department store Hochschild Kohn. They managed to sell it in 1969 and get back what they paid for it. They got lucky.

In 1993, much later in Buffett's career, he bought Maine shoemaker Dexter Shoe, paying $433 million worth of Berkshire Hathaway shares. Buffett already owned HH Brown (another shoemaker) and knew Dexter was in trouble because of foreign competition... just like his original textile investments. Buffett says the Dexter deal ended up costing Berkshire $3.5 billion by the time he finally liquidated in 2001. As Buffett told Reuters news service in 2008, "Dexter is the worst deal that I've made."

Writing in his 1989 shareholder letter, Buffett commented specifically on why these "value traps" usually don't work out...

How can you use these lessons in your own investing? Buffett says just to stick with the stuff that's easy: "In both business and investments, it is usually far more profitable to simply stick with the easy and obvious than it is to resolve the difficult." And in tomorrow's essay, I will show you exactly how to identify these "value traps"... and I'll share the companies to avoid today.

Regards,

Porter Stansberry

Further Reading:

Earlier this year, Porter showed readers a way to guarantee that you will beat the market. "I don't think a better strategy exists for individual investors," he says. "These results are clearly better than any newsletter that has ever been published... and better than just about any investment fund in existence." Learn more right here.

Dr. David Eifrig recently showed another way to profit in a down market. He says right now is the ideal time to be selling options on high-quality businesses. Learn why this strategy is so successful in this essay from last week.

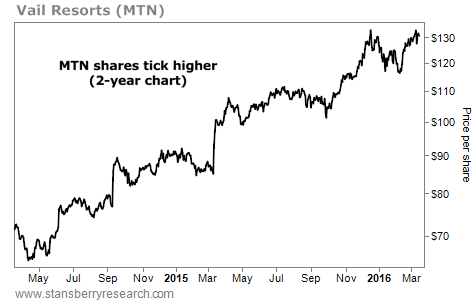

Market NotesWHAT OUR 'SKI GAUGE' IS SAYING TODAY One of the classic spending stocks we monitor is rallying, and that's a positive sign for the U.S. economy...

As longtime readers know, when we say "spending stocks," we're referring to "I want this" – not "I need this" – purchases. Put simply, when the economy is doing well, people are more willing to spend extra on things like cruises... art... movies... and more.

They're also able to spend more on ski trips. The stock we're highlighting today is Vail Resorts (MTN). The popular ski-resort operator is a top spot for people who want to hit the slopes. Vail Resorts also owns resort hotels throughout the world.

As you can see below, MTN shares are starting to climb higher today. Shares are up more than 10% since mid-February and are now a chip-shot away from a new high. It's a sign that things can't be all that bad with the U.S. economy right now...

|

Recent Articles

|