Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Feel That? It's the Chill of DeflationBy

Friday, February 6, 2015

That chill in the air? This is what deflation feels like...

Right now, the 10-year U.S. Treasury pays just 1.8%... oil is $50 a barrel... commodity prices drift near to chilling lows... and the dollar is near multiyear highs. These are all deflationary trends.

What deflation means for you as an investor is what I want to explore today. As an investor in stocks, there is a safe path through a deflationary Ice age.

I'll get to that in a moment. But first... what exactly is deflation?

The economic word deflation, says the Oxford English Dictionary, first appeared in print in 1920. The idea, I'm sure, is much older. But it is the economist Ralph G. Hawtrey who gets credit for putting the thing into words when he wrote, "Deflation... is a reversal of the process of inflation." For the record, Hawtrey was against it.

Hawtrey may be the first to define it, but definitions are dry, dead things, especially in this case. Deflation is so much more than falling prices. It is also distinctly chilly.

Barton Biggs used to write about Fire and Ice, always capitalized, borrowing from Robert Frost. Ice was deflation. In a memo dated Aug. 18, 1997, the former Morgan Stanley strategist defined Ice in more certain terms than Hawtrey:

That's a more colorful definition. It also fits our spot in history rather well. We've got all of the above. The only one we haven't seen much of is erosion of profits. But that's coming. The year 2014 will go down in the books as a record year for profit margins. The S&P 500 will likely finish with a profit margin of more than 10%. It has never been that high, as the Wall Street Journal recently reported.

My bet is that will be a peak that will stand for a long time. As Horizon Kinetics wrote in their fourth-quarter commentary:

Two of those exhausted changes are falling interest rates and taxes. Look at what has happened since 1980, again from Horizon Kinetics:

Rates are low and will probably head lower, but the lion's share of the gains have already been eaten. It also seems impossible to imagine, in the current climate, that corporate tax rates will fall. So we're back to Ice.

Ice means slow growth in sales and earnings. "Companies that can grow earnings and dividends in an Ice age should be prized," Biggs wrote. Historically, they have been. "In the 1950s and early 1960s," Biggs goes on, "slow, steady growth sold at 40 times earnings. The problem is that making the transition from one environment to the other can be very disruptive and painful for the companies that are structured for the previous one."

(By the way, Biggs' essays on Fire and Ice are in the compilation Biggs on Finance, Economics and the Stock Market. It's an interesting book to flip through – you learn, among other things, that not much has changed in markets over the years. The same debates just recur in different dressings.)

So at least one page of the playbook is obvious. You want growth. The ability to grow is a prize in any Ice age. The higher the growth rate, the more prized that growth is.

Where to find growth?

That's the key question. Following Charlie Munger's quoting of 19th-century mathematician Carl Jacobi ("Invert, always invert"), we can try to answer the question first by saying where the growth isn't.

Well, one place you're not likely going to find it is in the commodity space. Those stocks face massive headwinds as the prices of what they sell fall. But Ice is tough on more than commodity prices.

As Biggs says, Ice is also tough for companies fitted for the prior environment. All kinds of companies used to having steady growth and small price increases will find it not so easy anymore. Many of the great brands – Coca-Cola is a good example – struggle to generate any growth at all.

There are plenty of industries with excess capacity. Go to Google News and type in "excess capacity." All kinds of stuff comes up. There's too much steel. There's too much excess factory capacity of seemingly everything in China. And on and on.

Ice is not necessarily all bad either. Japan has been in an Ice age for a couple of decades. Yet life is not bad in Japan. Biggs, too, appreciated this. In Diary of a Hedgehog in 2010, he wrote about Japan:

And even in an Ice age, there are also pockets of growth... For instance, if we are in an Ice age, you want to go small. Smaller companies can grow faster in little niches than the giants. There are exceptions, though (like Apple). In my Capital & Crisis newsletter, we've been focusing on many of these "exceptions."

I'm not sure if this deflationary chill will continue... But if it does, my readers will be prepared. I urge you to do the same.

Good investing,

Chris Mayer

Further Reading:

One of Chris' most popular DailyWealth essays is "A Triumph of Lethargy and Sloth"... an inspiring tale about the "coffee can" portfolio. "If you take its wisdom to heart," he writes, "you'll be ahead of 99.9% of your fellow investors."

"Nobody believes that DEFLATION – the opposite of inflation – is possible," Steve Sjuggerud writes. "But it is." Learn more about deflation – and why "it's the Fed's worst nightmare" – right here: The Financial Storm Nobody Is Expecting.

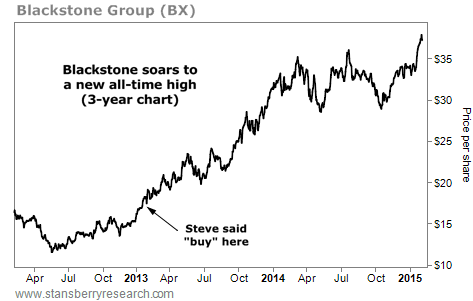

Market NotesSTEVE WROTE IT, DID YOU BUY IT? Blackstone Group (BX) just soared to a new all-time high... and DailyWealth readers shouldn't be surprised.

Back in January 2013, Steve Sjuggerud began writing about the opportunity in Blackstone Group. In short, Blackstone is Steve's favorite "back-door" way to invest in the U.S. real estate rebound.

Blackstone started out in the 1980s as a private-equity group. But it has evolved into one of the planet's biggest "alternative" asset managers. ("Alternative assets" means it's not investing in your typical stocks, bonds, and mutual funds.) Basically, people pay Blackstone to manage their money for them.

As Steve wrote a few years ago, Blackstone started buying up residential real estate properties at dirt-cheap prices, fixing them up, and then selling them for a profit. According to Steve, investors stood to double their money with Blackstone within two years based on this simple "Buy It. Fix it. Sell it." strategy.

As you can see below, Steve's bold claim turned out to be conservative. Investors who bought on Steve's recommendation doubled their money in just one year. Over the past two years, shares are up 127% (not including dividends)... and just soared to a new all-time high.

|

Recent Articles

|

|||||||||||||||||||||||||