Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Reduce Next Year's Tax Bill – Starting TodayBy

Friday, April 10, 2015

If you're like me, April 14 can be a painful day.

It's the day before "Tax Day" here in the U.S., when individual income tax returns are due to the IRS.

No matter your politics... or your thoughts on what the tax rate should be... it hurts to see that final number of just how much you've paid in taxes this year. It's difficult not to imagine what you could buy with those thousands of dollars. Or how much you could boost your savings.

But there's a simple way that you can reduce how much you pay in taxes each year. And it doesn't take a tax attorney or complicated accounting.

All you need to do is buy into one of the most stable and tax-efficient investments in the market. And in return, you can earn thousands of dollars a year in extra income... all without paying a single cent to the IRS.

I'm talking about municipal bonds, also known as "munis."

Regular readers know that muni bonds are loans to local governments. By buying a muni bond, an investor loans a municipality cash to build roads, schools, or other public buildings. In exchange, the government promises to send investors regular interest payments. At the end of the bond's life, the government also returns the initial "principal" investment.

Municipal bonds are a remarkably safe investment.

Investment-grade municipal bonds (those ranging in grade from A to triple-A) have had a default rate of only 0.017% over the past 40 years, according to Forbes magazine. In other words, less than two out of every 10,000 investment-grade municipal bonds default.

Put another way, if you invest $100 into muni bonds, you can expect to lose only 1.7 cents from cities or states that end up unable to pay you back over 40 years.

Municipal bonds can pay anywhere from 3% to 7%, depending on which cities or states issued them and which tax revenues they can tap to pay off the interest.

You also can earn income from these bonds, tax-free.

That's because income from munis is exempt from federal income tax. And if you own bonds that were issued from your own state, you won't have to pay state taxes either. (This is the case in most states, but you should check your local laws.)

For instance, if you earn 6% on a municipal bond and you're in the 25% tax bracket, you end up with the same income as if you earned 8% in a taxable investment.

But for many individual investors, buying municipal bonds directly can be difficult and confusing.

The brokerage fees are expensive, the transactions are complex, and the minimum investments are high. Plus, sorting through the 1.5 million different bonds further complicates things.

I've found a way around all that. After all, I doubt you want to take the time to become a muni-bond expert and manage a complex portfolio.

That's why I like to buy bonds through investment funds dedicated to owning municipal bonds. For an example, let's look at the Invesco Value Municipal Income Trust (IIM)...

IIM holds more than 300 different municipal bonds, worth a total of around $1.1 billion. The average bond in its portfolio yields around 4%. But because the fund borrows a bit of capital to increase its leverage to buy some bonds on margin, IIM yields about 5.3%.

If you look at IIM's portfolio, it sticks to very safe munis from safe issuers.

About 75% of its funds are invested bonds that have received an investment rating of Baa level or higher. Of that group, the riskiest ones have just a 0.1349% chance of defaulting in 10 years (or 13 out of 10,000).

This resilience has been proven in the toughest of times. During the 2007-2008 financial crisis and the intervening years, some analysts called for a wave of defaults in municipal bonds. They felt that state and local governments were too indebted and couldn't pay bills.

I, on the other hand, have been a big proponent of muni bonds for five years now.

You may have heard big news of financial trouble in Detroit and Puerto Rico, but even those "big" defaults are miniscule to a diversified portfolio. And now, the local economies are improving, tax revenues are up, and municipalities are very healthy. At the same time, muni bonds have provided great returns.

It's something that every income investor needs in their portfolio.

So if you have investments in corporate bonds or stocks, you're paying taxes on the income they generate. As you prepare your 2014 return, take a look and see just how much that adds up to.

If you switch some of your capital into muni bonds, the income they generate will flow to you, tax-free. (You still pay capital gains taxes if you sell the fund for a gain, though.)

And with municipal-bond funds, you can get a diversified collection of the top-rated bonds in just a few minutes.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Earlier this month, Doc shared a simple trick to finding the world's best tech stocks. "For every wild tech company burning through cash, a select few create massive profitable cash flows by providing essential services," he writes. Find out how Doc uncovers these cash-gushing businesses here.

Doc also told readers why he sees plenty of upside left in U.S. stocks. "While the economy has improved a great deal from its crisis six years ago, it still has a good deal of room to improve," he writes. Get the full story here.

Market NotesANOTHER BIG 'PICKS AND SHOVELS' WINNER We've told you about the recent uptrend in homebuilders... Today, we look at one of the biggest "picks and shovels" winners in the housing rebound.

Regular readers know we're proponents of investing in picks-and-shovels companies to profit from sector and commodity booms. Picks-and-shovels providers don't bet the company on one project... They sell vital goods and services to an industry (read our educational interview about it here).

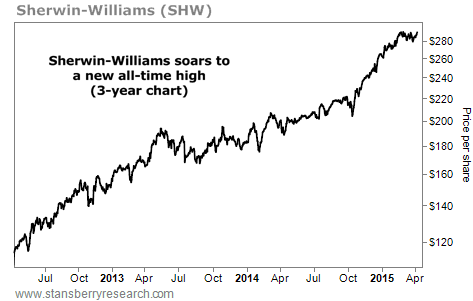

A great example is Sherwin-Williams (SHW). Sherwin-Williams doesn't build houses or manage a portfolio of properties. It's a housing picks-and-shovels investment because it's one of America's largest paint suppliers. As more houses are built or remodeled, people buy more paint.

As you can see below, folks are buying plenty of paint. Shares of SHW are up more than 150% in the past three years... and just yesterday, reached a new all-time high. Things are going so well that the company announced a 22% increase to its dividend last month. As the housing sector recovers, housing picks-and-shovels companies like SHW will continue to benefit.

|

Recent Articles

|