Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

Our Strategy Beats the Market With Less RiskBy

Wednesday, June 10, 2015

Buy great businesses at good prices.

I've been telling my readers (and anyone else who will listen) this for the past several years.

Owning great businesses at good prices allows you to do something you're not supposed to be able to do. It allows you to beat the market with less risk...

My research partner, Mike Barrett, recently read an excellent Barron's interview with hedge-fund manager Andrew Wellington.

Wellington runs the $3 billion Lyrical Asset Management, which Barron's ranks among the "Best 100 Hedge Funds." Hedge funds are similar to mutual funds, but typically invest in a wider range of securities and are most suitable for institutional investors and individuals with substantial wealth.

For the last three years, Lyrical's U.S. Value Equity Fund strongly outperformed the S&P 500. And it did it with a similar approach to the one we use in my Extreme Value newsletter.

Here's what Mike wrote in a recent Extreme Value update:

This is exactly what we do in Extreme Value. We look for high-quality businesses selling at discounts to intrinsic value (measured by net assets and/or earnings power). A great business is a leader in its industry. It gushes free cash flow... rewards shareholders... has a great balance sheet... earns consistent profit margins... and has high return on equity.

But even a great business can be a bad investment if it's too expensive. That's why we never buy a great business until it's trading at a cheap price. And we sell a business when it's trading at an expensive price (or has already performed as well as we could have expected).

You might be wondering if having a limited number of stocks in a portfolio or fund is sufficiently large enough to spread risk. Here's what Wellington told Barron's (emphasis added)...

Mike and I wholeheartedly agree with Wellington. That's why we always recommend taking a position that's big enough to make you money but small enough to allow you to be dispassionate should it turn into a mistake. For example, we always recommend putting no more than 5% of your investment dollars into our great businesses in buy range.

We also recommend you build positions slowly to take advantage of share-price volatility. So, for example, you might consider building a long-term position one quarter at a time. If you plan to invest $4,000 in a particular stock, you could divide this into four $1,000 purchases made at different times.

Finance professors, advisors, and most brokers will tell you that to get market-beating returns, you have to take more risk. That's not true at all... When you buy the world's best businesses at good prices, you get big returns... without taking big risks.

Good investing,

Dan Ferris

Further Reading:

Learn how Dan picks great buy-and-hold businesses in these must-read essays:

"If you study what I'm about to teach you, you will be able to identify companies that 'jump off the page' as wonderful investments you'd like to own one day."

"What should a customer do with IBM? IBM is dropping... so should he still buy?"

"Owning these businesses allows you to do something you're not supposed to be able to do... "

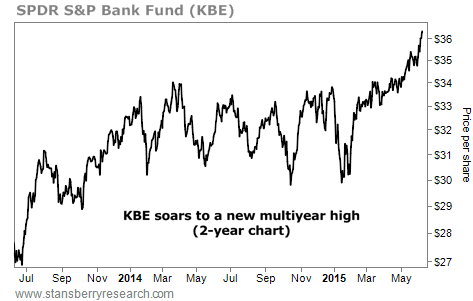

Market NotesSMALL BANK STOCKS ARE SOARING A month ago, we showed you how regional banks had "broken the box" and were headed higher... Today's chart provides an update.

Like most assets, regional banks were crushed in the 2008-2009 bear market. But since bottoming in 2009, it has been all recovery in the U.S. banking sector. Regional banks have "digested" the bad debts of years past, and these businesses are now growing.

Our chart shows the price action in the SPDR S&P Bank Fund (KBE). This fund tracks the KBW Regional Banking Index, a widely followed gauge of regional banking firms. These firms aren't the giant "too big to fail" banks like Bank of America and Citigroup. They tend to practice a more boring kind of banking, rather than trading trillions of dollars' worth of financial derivatives. They benefit when their local regions enjoy better economic times and rising asset values.

As you can see below, shares of KBE have tacked on another 4% since our last note – despite weakness in the overall market. Just yesterday, they reached a new multiyear high. The bull market in regional banks is still on.

|

Recent Articles

|