Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Chris Mayer is one of the best stock pickers in the game, and he's developed a "cult" following among devoted newsletter readers. Over the last decade, his stock selections have beaten almost everyone and everything... including Warren Buffett, David Einhorn, and Carl Icahn.

Chris recently became the newest expert at Bonner & Partners, chaired by Agora founder Bill Bonner. Chris and Bill have known each other for many years. And one of things Chris likes to do is send notes to Bill about great investors – how they did it, and what he's learned from them. Below, Chris shares one of these notes with you.

Follow This Legendary Investor's Strategy for Big, Safe GainsBy

Friday, April 8, 2016

I recently sent Bill my notes on a book I read about legendary investor John Templeton. It's called Templeton's Way with Money: Strategies and Philosophy of a Legendary Investor by Jonathan Davis and Alasdair Nairn.

As I'll show you today, the lessons from this book are in many ways foundational to how Bill and I approach his portfolio...

First, some background on Templeton...

He started his flagship Templeton Growth Fund in 1954. He ran it until 1992. The average return was about 16% per year for 38 years.

This was almost four points better than the market over that time... an astonishing achievement. He did it without using debt and often had excess cash.

If you had put $10,000 with Templeton in 1954 and left it there, you would have had $1.7 million when he stepped down in 1992. That's a 170-fold return.

So, how'd he do it?

Authors Davis and Nairn sum it up this way:

In his latest issue of The Bill Bonner Letter, Bill wrote:

On this, we are in complete agreement. Templeton's philosophy is one we want to emulate. Buying cheap is a key part of that. But there are other important lessons from Templeton's career. And they may surprise you...

He was happy to hold high levels of cash and bonds when cheap stocks were hard to come by. In 1969, he had one-third of his fund in cash/bonds because the high-flying market did not offer many cheap stocks. He was not a market timer, but he stuck to his positions, even if this meant trailing the market when it went nuts.

His field was the world. Templeton went where there was opportunity. For example, he invested heavily in Japan in the early 1970s when it was out of style to do so. There he found rapidly growing companies trading at cheap prices. In 1974, he had 62% of his fund in Japanese stocks. Meanwhile, the World Equity Index, a benchmark for global markets, had just a 12% weighting in Japan.

He was not afraid to change his mind. By 1978, he had less than 10% of his fund in Japanese stocks. As the stocks grew pricey, he sold them. By 1989, when the World Equity Index had a 40% weight in Japan, Templeton's weight was 0%. The Japanese market would never recover the heights it climbed in 1989. What's important here: Templeton did not wed himself to any of his ideas. Everything was for sale at the right price.

He was not afraid to concentrate his holdings. He often made big bets on things in which he had high conviction. In 1969, for example, his largest holding was 15% of his fund. And as I discussed above, he once had more than 60% of his fund in Japanese stocks. This was a pattern throughout his career.

He traveled – a lot. Templeton wrote that it was important to travel abroad, not only to find ideas but also to learn about the world. "[Travel] teaches us to question the economic theories and fads popular here," he wrote. "It gives us deeper respect for the fact that the most unexpected things can happen and often do." (Bill and I certainly do more than our share of traveling.)

His performance improved when he moved away from Wall Street. Templeton moved to the Bahamas in 1968. There he worked alone, more than a thousand miles from Wall Street. Sometimes he would do his research for only a couple of hours a day. He was patient and thoughtful. Many great investors today work off Wall Street.

He wasn't good all the time. This is critical to understand. The best investors often have periods where they look bad. Templeton was no different. His fund lost money in 10 of those 38 years – almost 25% of the time!

From 1971 to 1975, he trailed the market in three years out of five. Every time he did, the media would write stories about how he lost his touch. Incredibly, for the first 10 years of the fund's life, Templeton trailed the MSCI World Index. Today's impatient investors would likely fire such a manager.

He held his stocks for four to five years on average. He also urged his investors to judge him on five-year returns. Few investors hold their stocks for even a year or two. They are like gardeners pulling up their tomato plants before they get their tomatoes.

His best years as an investor were his last 20 years. And he quit running his fund when he was almost 80 years old. I told Bill he has a lot of years yet!

As I mentioned above, Templeton's approach is one Bill and I strive to emulate... and it's one you may want to consider as well...

Sincerely,

Chris Mayer

Further Reading:

"Dividends... REAL CASH PAYMENTS from companies... this is what you want – right?" Steve asks. Learn why dividend investing alone is not a good strategy right here.

Market NotesANOTHER WAY TO SEE THAT 'THINGS CAN'T BE ALL THAT BAD' Our 'POOL' indicator isn't the only thing pointing to a healthier economy... Today, we check out shares of another reliable economic gauge...

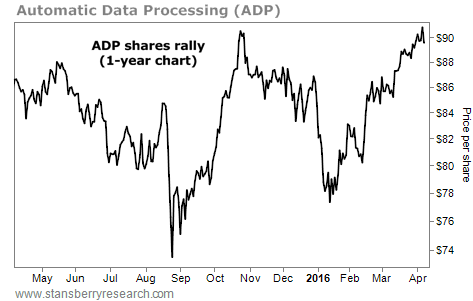

Automatic Data Processing (ADP) is the country's leading payroll-processing and benefits company. If you have a job, chances are good that ADP withholds your taxes, hands them to various government agencies, processes your check, and pays you the rest.

That's why ADP is one of our favorite real-world indicators. Checking in on how shares are performing can tell us a lot about employment in the U.S. If companies aren't hiring, ADP's business won't grow.

As you can see from the chart below, ADP's business is growing. The U.S. economy added 200,000 new jobs in March alone. Shares are up more than 15% since mid-January and just touched a new all-time high. We aren't saying everything is rosy out there, but when ADP is marching higher, it's hard to be pessimistic...

|

Recent Articles

|