Not a subscriber? Click here to learn

more.

|

| Home | About Us | Resources | Archive | Free Reports | Market Window |

|

Editor's note: Today's DailyWealth essay comes from our colleague Dr. David "Doc" Eifrig's excellent Retirement Millionaire Daily e-letter. (You can sign up right here.) In it, he shares three mistakes you might not realize you're making that could be costing you a lot of money...

Three Investment Mistakes That Are Draining Your PortfolioBy

Wednesday, July 13, 2016

Most folks just want a hot stock tip...

These folks will likely never truly grow their wealth. And when a crisis comes, they'll be the first to panic.

If you've followed my investment newsletters – my health-and-wealth letter Retirement Millionaire, my income-focused letter Income Intelligence, and my high-end, options-trading service Retirement Trader – you know that in each issue, I not only recommend great businesses at good prices... I also give you a hefty dose of education and empowerment.

Finding investments that increase the size of your portfolio is just one part of being a successful investor. Preserving your wealth is an essential part as well.

Today, I'm sharing three common mistakes people make that drain their money.

If you avoid them, I can almost guarantee you'll be on track to save yourself thousands of dollars in the next decade...

No. 1: Avoid Whole-Life Insurance as an Investment There's an idea floating around out there that whole-life insurance is a great way to build wealth and income for your future...

The idea is that whole-life insurance policies allow you to save up your own money and get insurance for your family in case of death. Late in life, you can draw down on the cash value of the policy to support your idealized lifestyle... Or if you die early, your family will get paid the agreed insurance amount.

But that sort of protection can be had with much cheaper term-life insurance. And the big trouble with whole life is the fees. Whole life typically takes a big, upfront commission when you start saving. If you understand the phenomenon of compounding, you know that a small change in your savings early on can lead to a big change in your wealth.

Added to that, the most generous whole-life policies pay about 4.5% a year. The stock market returns about 8% a year on average. So you're not only starting behind, you're running at a slower pace.

Also, whole life only works if the insurance company is still able to pay you in 30 years. In this day of low interest rates and low returns for insurance companies, that's a real risk over the next decades. Avoid whole-life insurance products.

No. 2: Don't Pay Front-Loaded Mutual-Fund Fees

Much like whole-life insurance products, some mutual funds have fee structures that take a big chunk out of what you invest on the first day... up to 5.75%.

That means if you buy $50,000 worth of a front-loaded mutual fund, you start off $2,875 in the hole. Over 20 years, this is easily worth the value of a car in retirement.

The argument for front-loaded mutual funds is that they have lower annual fees, so you make out better over the long term. This is sometimes true, but you'd need to hold these funds for at least eight years to come out ahead. And the average investor holds a mutual fund for 3.3 years.

Do what I do and go for the no-load mutual funds and closed-end funds.

And never invest in a mutual fund without reviewing its fees. You can do this quickly by going to the financial-information website Morningstar, entering a fund's ticker symbol, and clicking "expense."

No. 3: Never Use Market Orders

When you buy a stock or any security on your online trading platform, you can use two types of orders: a market order or a limit order.

A market order will fill your order essentially immediately at any price. Using one is like telling your broker, "Buy me this stock for whatever price you can get."

A limit order sets the maximum price you are willing to pay, and it will sit unfilled until your broker can get that price or less (or until you cancel the order). It's like telling your broker, "Buy me this stock, but only if you can get it for less than $10" (or whatever price you specify).

If a stock price is moving higher, you can easily pay too much for a stock using a market order because you've given up control of the price you pay.

Don't use market orders – use limit orders instead. Set your price at the same price you see in the market, and then wait. You never want to be the sucker that pays the worst price of the day.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

Read more of Doc's insights here...

"These are the lessons I wish I had heard at 20 or 25. And even if you're a seasoned investor, they will still probably resonate with you... "

"When people find out I've been producing my own wine... they often ask for a bottle," Doc says. "And when they learn about my experience in finance... they always ask the same question."

"When most folks think of investing, they think of either stocks, which provide the potential for capital gains, or bonds, which provide safe and steady fixed income," Doc writes. "It turns out that you don't necessarily have to choose between the two."

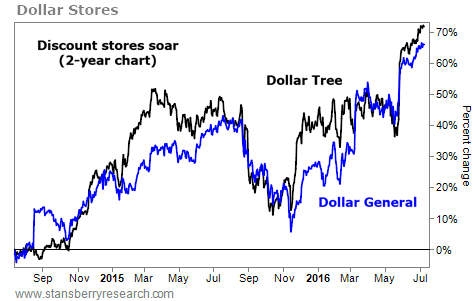

Market NotesTHE BULL MARKET IN DOLLAR STORES Today's chart shows the powerful uptrend in America's discount stores...

It doesn't take much to realize that the cost of living in the U.S. has increased. Across the country, average rents and grocery prices are on the rise. Meanwhile, the paychecks of lower-income wage earners aren't growing as quickly.

While that's bad news for a huge number of Americans, it's great news for discount retailers like Dollar General (DG) and Dollar Tree (DLTR). These chain stores don't sell brand-name goods. They simply sell everyday household items for super-cheap prices.

As you can see from the following chart, business is booming for these dollar stores. Shares of both companies are up 60%-plus over the last two years, hitting a new high earlier this week. As long as America's middle class continues to feel squeezed, this trend shows no sign of slowing down...

|

Recent Articles

|